Deribit now has a full suite of HYPE derivatives, including a perpetual future, dated futures, and options. All of these derivatives use USDC as the settlement currency, and benefit from margin requirement reductions with Deribit’s portfolio margin system. Eligible users holding USDC on Deribit also benefit from monthly USDC rewards (more info on rewards here).

HYPE spot will also be coming in the next few months, which will come with the ability to use HYPE as collateral in Deribit’s cross collateral system. Among other things, this will make positions like covered calls (selling call options against spot holdings) more capital efficient.

The new derivatives are of course useful for speculators, however they are also useful for hedgers and yield seeking traders. Let’s take a look at how these instruments work, as well as some use cases.

Futures and perpetuals

There are two types of future available for trading on Deribit, dated futures, and perpetuals. As the name implies, dated futures have a specific date on which they will expire. Perpetuals on the other hand do not have an expiry date, and therefore continue perpetually.

Both of these types of contract are well suited to:

- Leveraged directional trading – e.g. speculating on whether the price of HYPE will increase or decrease by longing or shorting the perp.

- Hedging spot holdings or option positions – e.g. protecting spot holdings against a decrease in price by shorting a future.

- Basis trading – e.g. buying HYPE spot, and then shorting either a dated future or the perp to earn the basis. For more on basis trading (a.k.a cash & carry), check out this playlist on the Deribit youtube here.

Futures and perpetuals are extremely useful delta one products, but as with all futures they are limited to the two events of either price going up, or price going down. For traders who want to be a bit more specific with their views, or who want to speculate on things other than just the price (e.g. volatility), that’s where options come in.

Options

Options grant the buyer of the option the right to trade an asset on a certain date, for an agreed upon price. The option buyer is not obligated to exercise their right, but they have the option to, hence the name ‘option contract’.

Options have the following parameters:

- The underlying asset – The asset that the option contract derives its value from. For the options we’ll be discussing in this article, HYPE is the underlying asset.

- The option type – Either a call option, or a put option.

- The expiry date – This is the date the option will expire and be automatically exercised if it has any value.

- The strike price – The price at which the buyer of the option has the right to trade the asset on the expiry date.

- The option price (aka the option premium) – This is the price the option buyer pays to the option seller to purchase the option.

On the Deribit platform you will see option instruments written in the following format:

Underlying Asset – Expiry Date – Strike Price – Option Type

For example if you see an option written as:

HYPE_USDC-25DEC26-100-C

This means the underlying asset is HYPE, the expiry date is 25th December 2026, the strike price is $100, and the option type is a call. The buyer of this call option then, is purchasing the right to buy HYPE at a price of $100 on 25th December 2026.

Let’s look at a payoff chart example of each or the two types of options, calls, and puts. To keep things simple in this article, we will only consider the value of the option at expiry.

HYPE put options

The buyer of a put option holds the right to sell the underlying asset (for example HYPE), at a fixed price until the option expires. If the underlying price is below the strike price of the put option at expiry, the option will have some value.

One common use for put options is to hedge against downside risk while continuing to hold a spot position. For example, imagine you are holding HYPE and are bullish long term and so do not wish to sell it, however, you are concerned about a bearish catalyst that is coming up in the short term. You want to protect against that short term downside risk without giving up the potential upside if price continues moving higher.

In this case, a put option could express your view well.

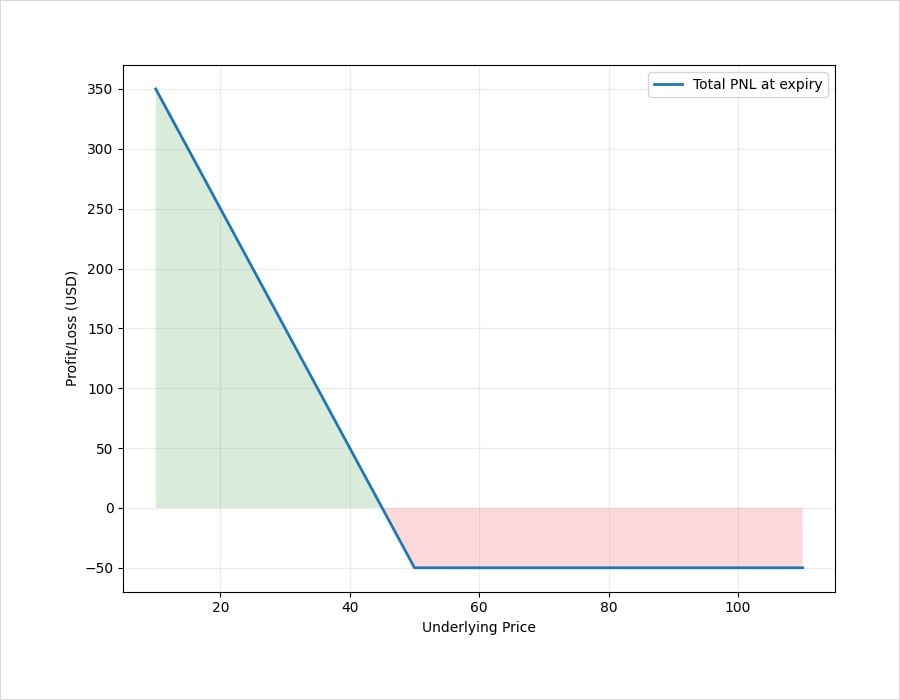

Let’s say we’re holding 10 HYPE that we purchased at $60 each, and we want to buy put options with a notional size of 10 HYPE to protect our spot holdings from price decreases below $50. The contract multiplier for HYPE options on Deribit is 10, so each option contract represents a notional size of 10 HYPE, therefore we will only need to purchase a single HYPE put option contract to protect our 10 HYPE. If we assume a strike price of $50 and an option price of $5 (so $50 total for the 10 HYPE notional) the payoff of buying the put option looks like this:

As you can see, the put option makes a profit at expiry if the underlying price decreases, but the losses are limited to the premium paid if the underlying price increases. Consequently, puts by themselves can be a good way to speculate on price decreases.

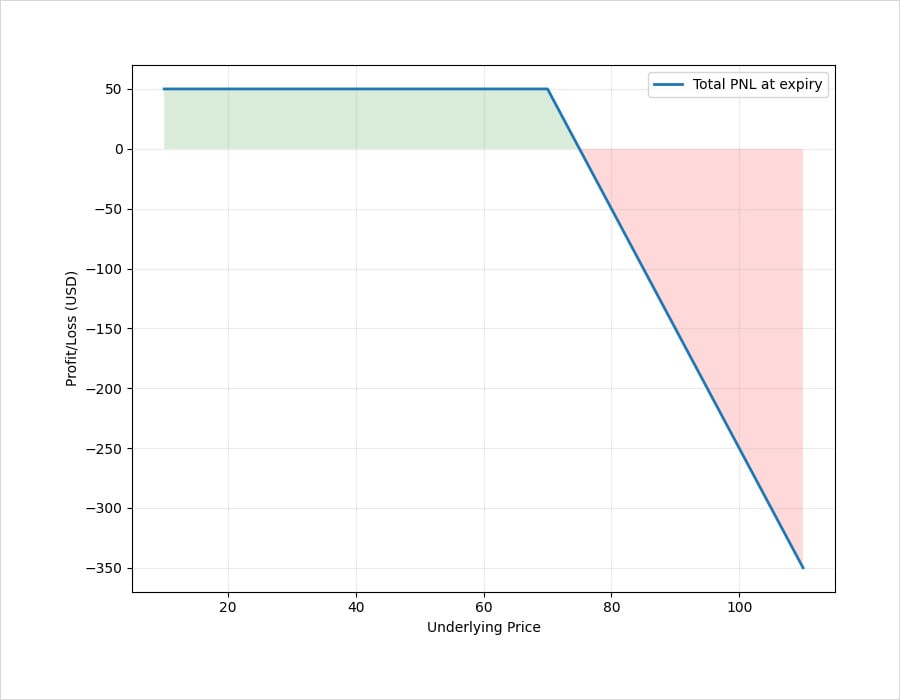

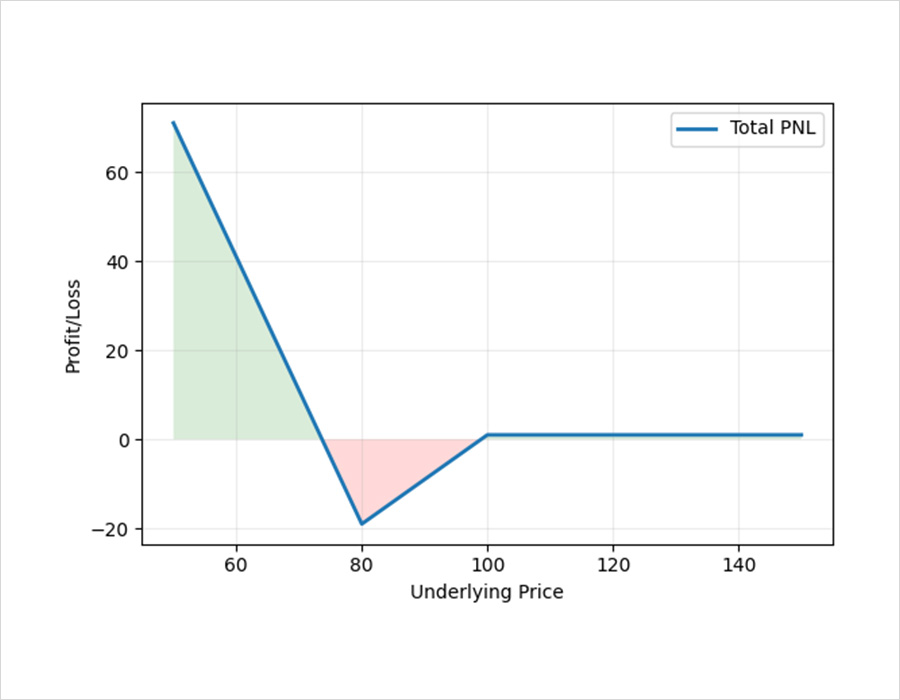

However, if we combine this put option PNL with the PNL of our spot position, we get the following combined payoff:

Let’s look at how this position performs at two extremes, the price decreasing to $20, and the price increasing to $100.

HYPE decreases to $20

Remember we purchased the 10 HYPE at $60 each, for a total of $600. With the underlying price now at $20, these same 10 HYPE are now only worth $200. The loss on the spot holdings alone is therefore $400.

However, we also purchased a $50 strike put option for a total of $50. At expiry, with the price of HYPE now at $20, the $50 put is worth $30 per HYPE, for a total of $300. The profit on the put option alone is therefore $250.

The total PNL is 250 – 400 = -$150

So we still made a loss, however the loss of $150 is significantly less than the $400 we would have lost if we had simply held the HYPE with no protection (the put) in place.

HYPE increases to $100

With the underlying price now at $100, our spot position of 10 HYPE that we initially bought for $600 is now worth $1,000. The profit on the spot holdings alone is therefore $400.

However, we also purchased a $50 strike put option for a total of $50. At expiry, with the price of HYPE now at $100, the $50 put is worthless. The loss on the put option alone is therefore $50.

The total PNL is 400 – 50 = $350

The profit is $50 less than if we had simply held the HYPE with no put protection, however we still made the vast majority of the profit that we would have done without purchasing the put.

HYPE call options

The buyer of a call option holds the right to buy the underlying asset (for example HYPE), at a fixed price until the option expires. If the underlying price is above the strike price of the call option at expiry, the option will have some value.

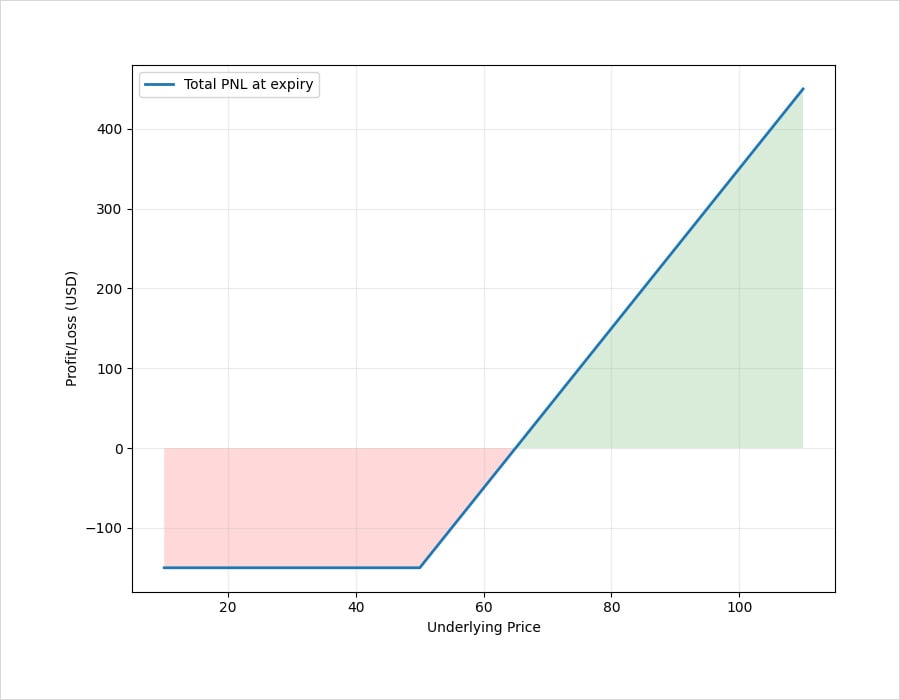

Let’s say we purchase a $70 call option with a notional size of 10 HYPE. The option price is $5 (so $50 total for the 10 HYPE notional). The payoff at expiry will be the following:

As you can see, the call option makes a profit if the underlying price increases, but the losses are limited to the premium paid if the underlying price decreases.

It’s clear to see why buying call options can be an attractive way to take a leveraged bet on the underlying price increasing, because the trader benefits from most of the upside (minus the premium paid), while having limited downside, and no chance of liquidation (assuming the option is fully paid for up front).

You may also notice that the shape of the long call payoff is the same as that of being long spot and long a put at the same time. By utilising options, it is often possible to create what are known as synthetic positions, where the payoff of a particular instrument is created by combining two or more different instruments. For more on that subject, see this lecture in the Deribit option course here.

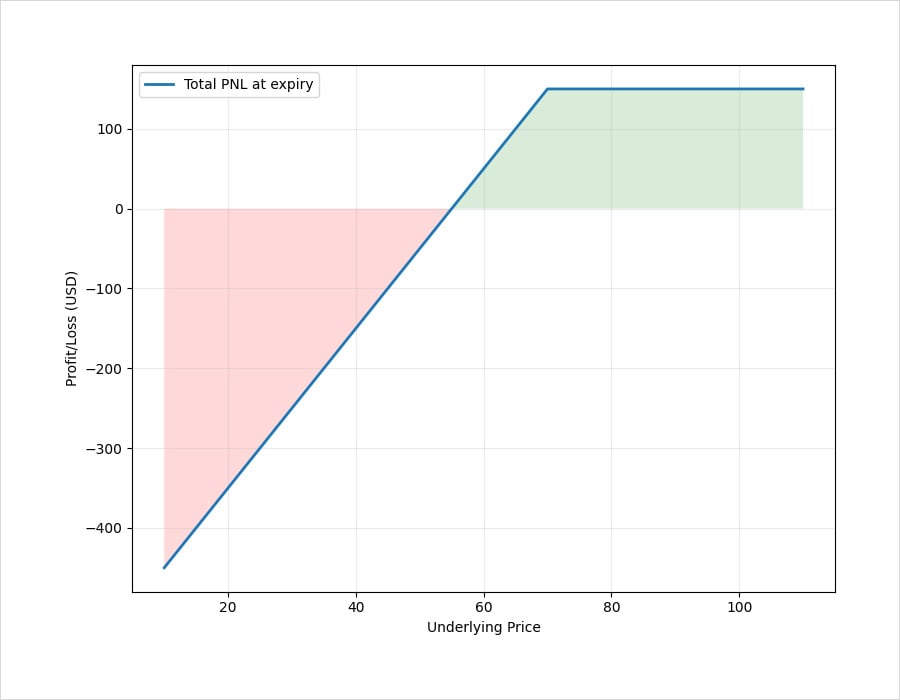

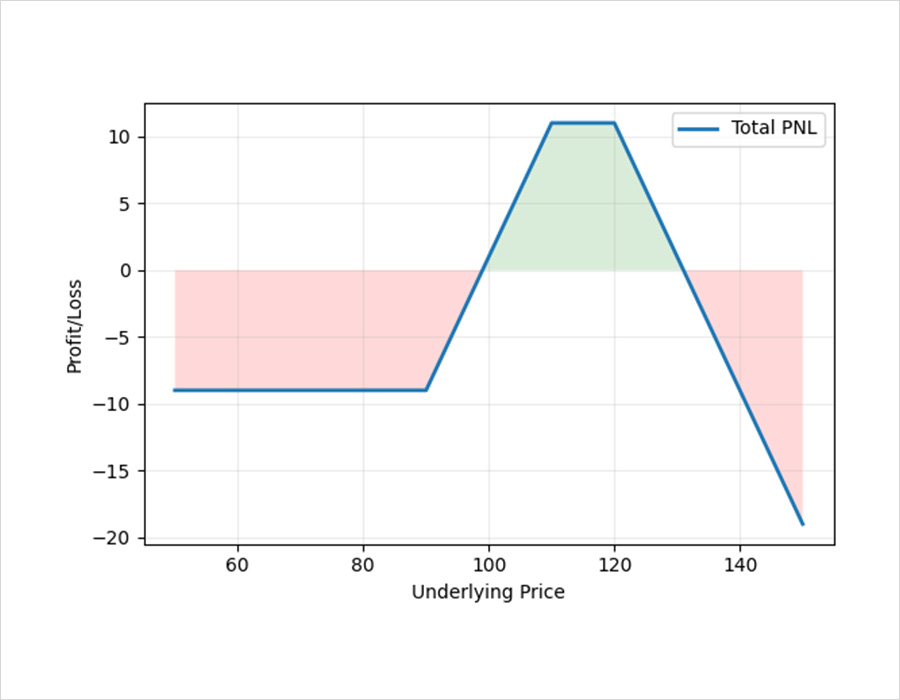

Covered calls

A covered call is a strategy that involves buying the underlying asset, and then selling a call option against that position. The sale of the call option, which by itself would have unlimited risk, is instead ‘covered’ by holding the underlying asset, hence the name.

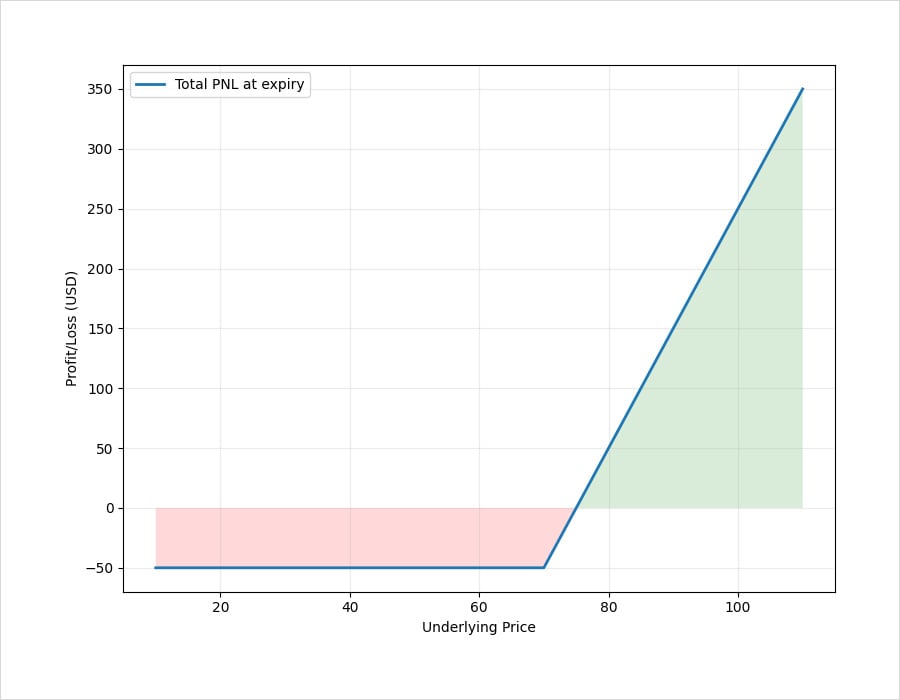

If we were to sell the $70 call option, with a notional size of 10 HYPE, this would be the payoff at expiry:

If we were to combine this short call with a spot position of 10 HYPE though, we get the following payoff:

The $50 of premium is received for selling the call, however, unlike the situation where we only hold the spot position, the upside is capped if the $70 strike price is breached. If the underlying price remains under $70 when the option expires though, the $50 premium is kept as profit, and the trader is free to repeat this process if they wish.

Note: It is common to see covered calls mentioned in the context of generating yield on your holdings. With a covered call, you are collecting a premium for selling the call, but this is in exchange for the risk of not benefitting from further spot price increases if the strike is breached. For this reason it’s wise to be cautious when comparing the yield from the short call to other forms of yield that are available. Always bear in mind where the yield is actually coming from, and what risk you are being compensated for.

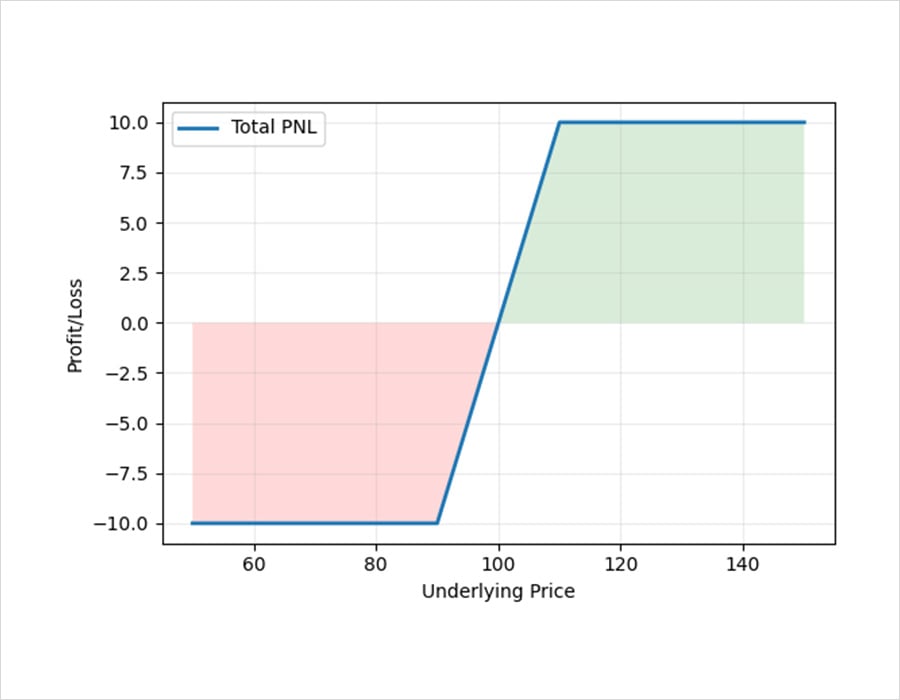

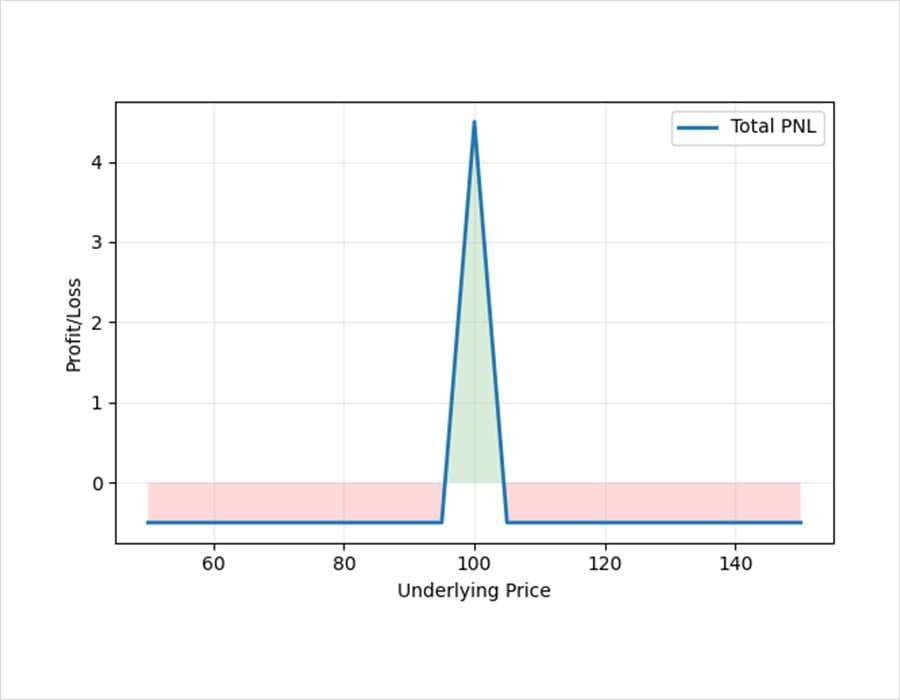

Multi-leg option positions

As well as single option positions, or combining them with spot positions, it is also possible to combine multiple different options together to create almost any payoff shape you can think of. The following images show some examples.

Vertical Spread:

Butterfly:

Put Ratio:

Call Ladder:

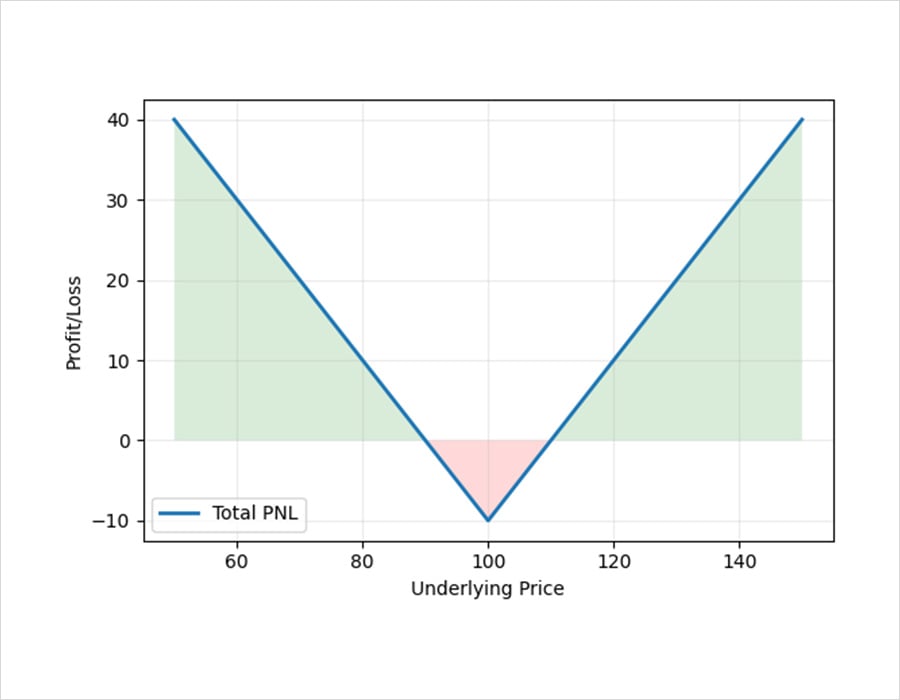

Long Straddle:

Discussing the details of each of these structures is beyond the scope of this introductory article, however if you wish to learn more, check out the Deribit option course. Section 12 in particular covers multi-leg strategies. The option course is also available on the Deribit YouTube.

For more details on each instrument type discussed in this article, see the relevant pages in the Deribit knowledge base: Options, Futures, Perpetual.