Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

Funding rates and future-implied yields are near their lowest levels in more than a month after the weekend’s spot selloff took prices back to the bottom end of the sideways trending range. Volatility at short tenor options rallied, causing an inversion in both BTC and ETH’s term structures at the front end, without lifting volatility levels at longer-dated expiries. The rise in volatility was matched by a strong skew towards OTM puts of volatility smiles at all tenors less than 3-months, indicating a strong switch in sentiment towards a demand for downside protection.

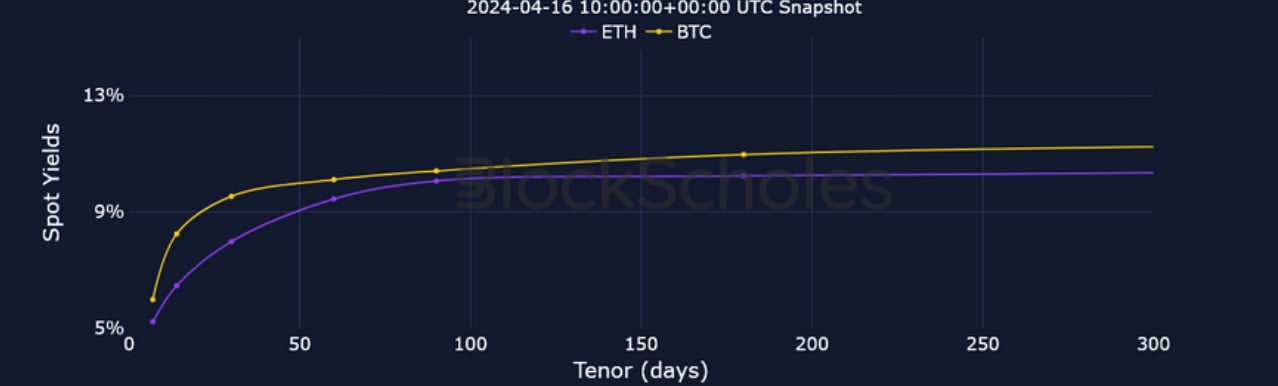

Futures Implied Yield, 1-Month Tenor

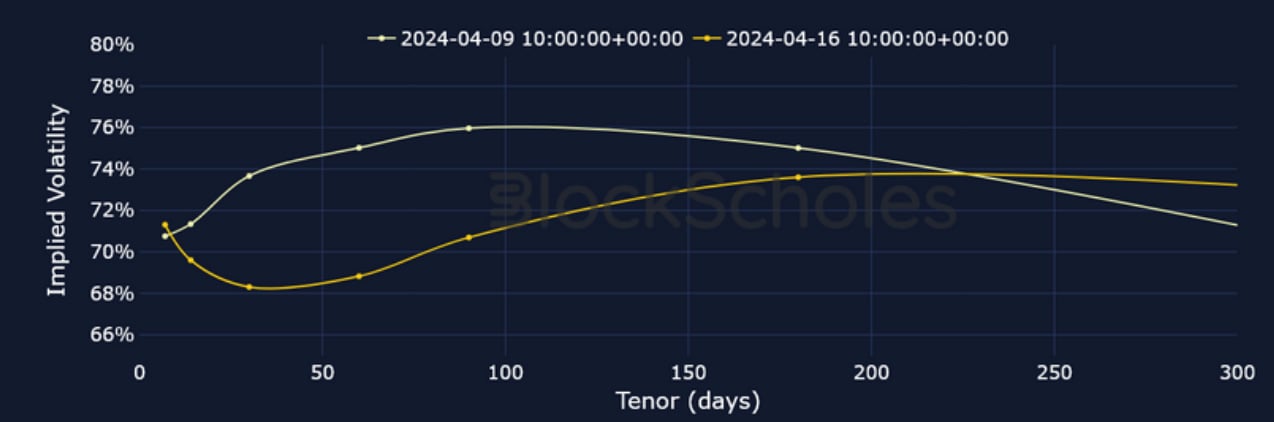

ATM Implied Volatility, 1-Month Tenor

Futures

BTC ANNUALISED YIELDS – yields trade near their lowest levels in over a month as spot has failed to continue it’s rally.

ETH ANNUALISED YIELDS – the term structure of ETH yields is slightly lower and more compressed across its term structure than BTC’s.

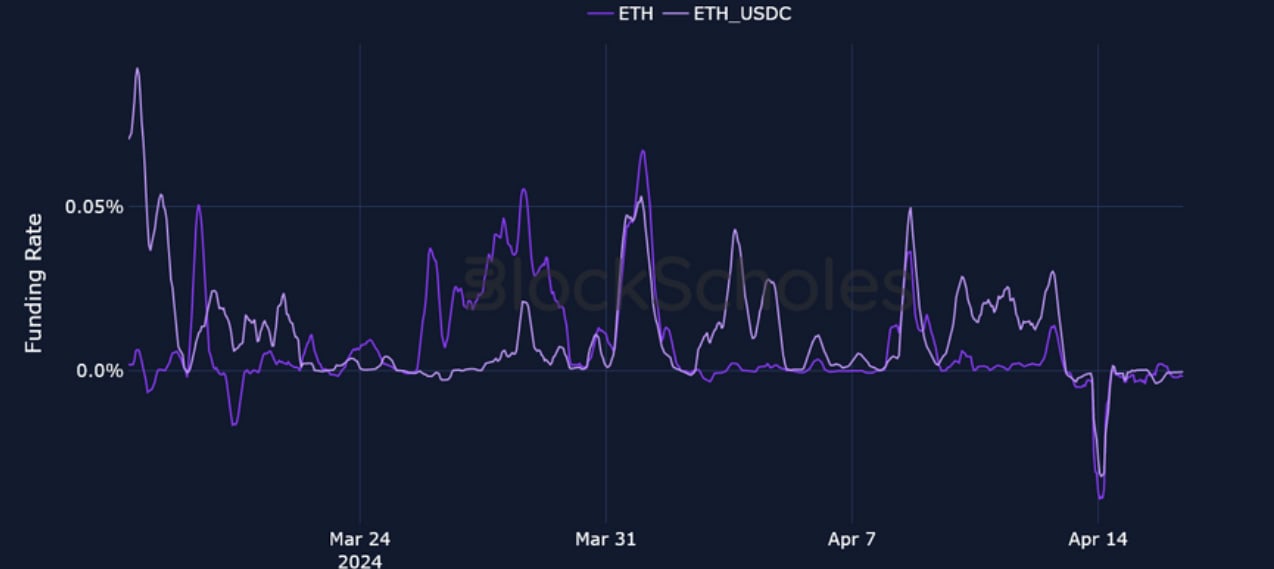

Perpetual Swap Funding Rate

BTC FUNDING RATE – has continued to trade intermittently negative over the last week as spot price trades at the bottom of its monthly range.

ETH FUNDING RATE – dipped strongly negative during the selloff on the evening of the 13th, but has remained close to zero in the days since.

BTC Options

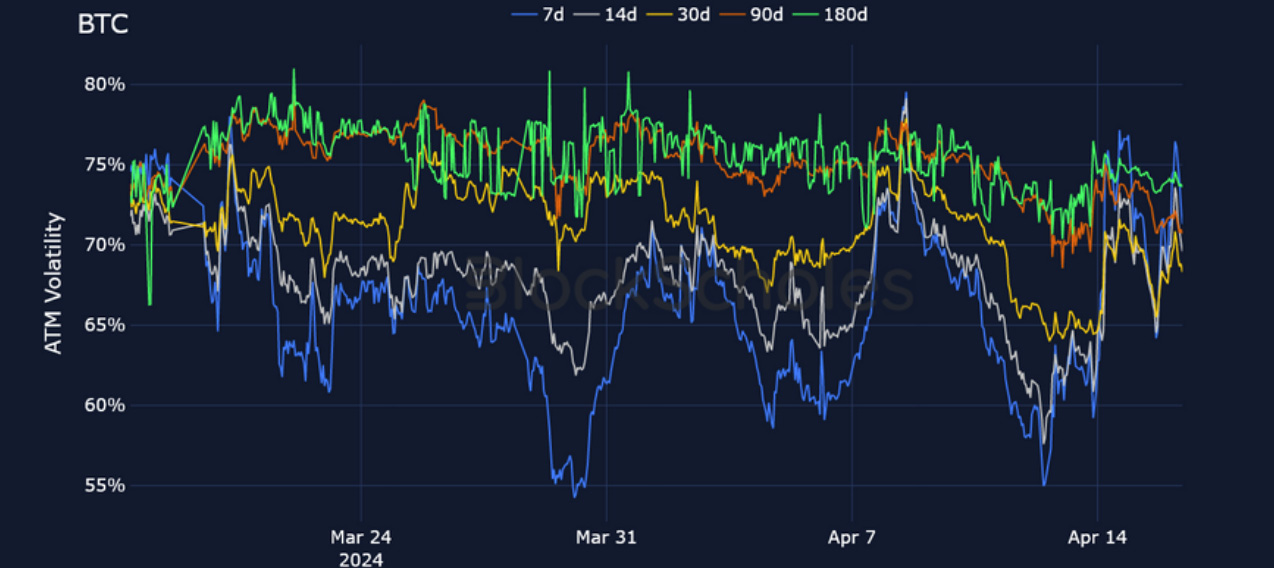

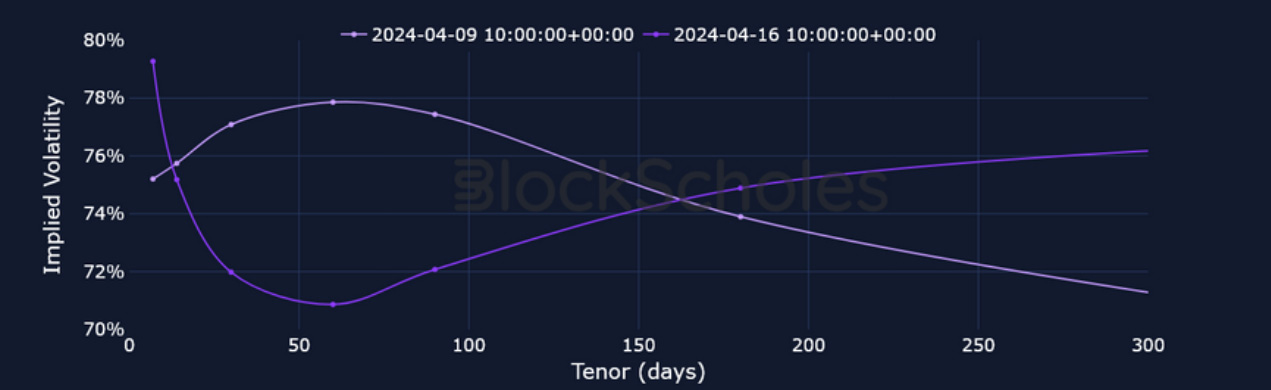

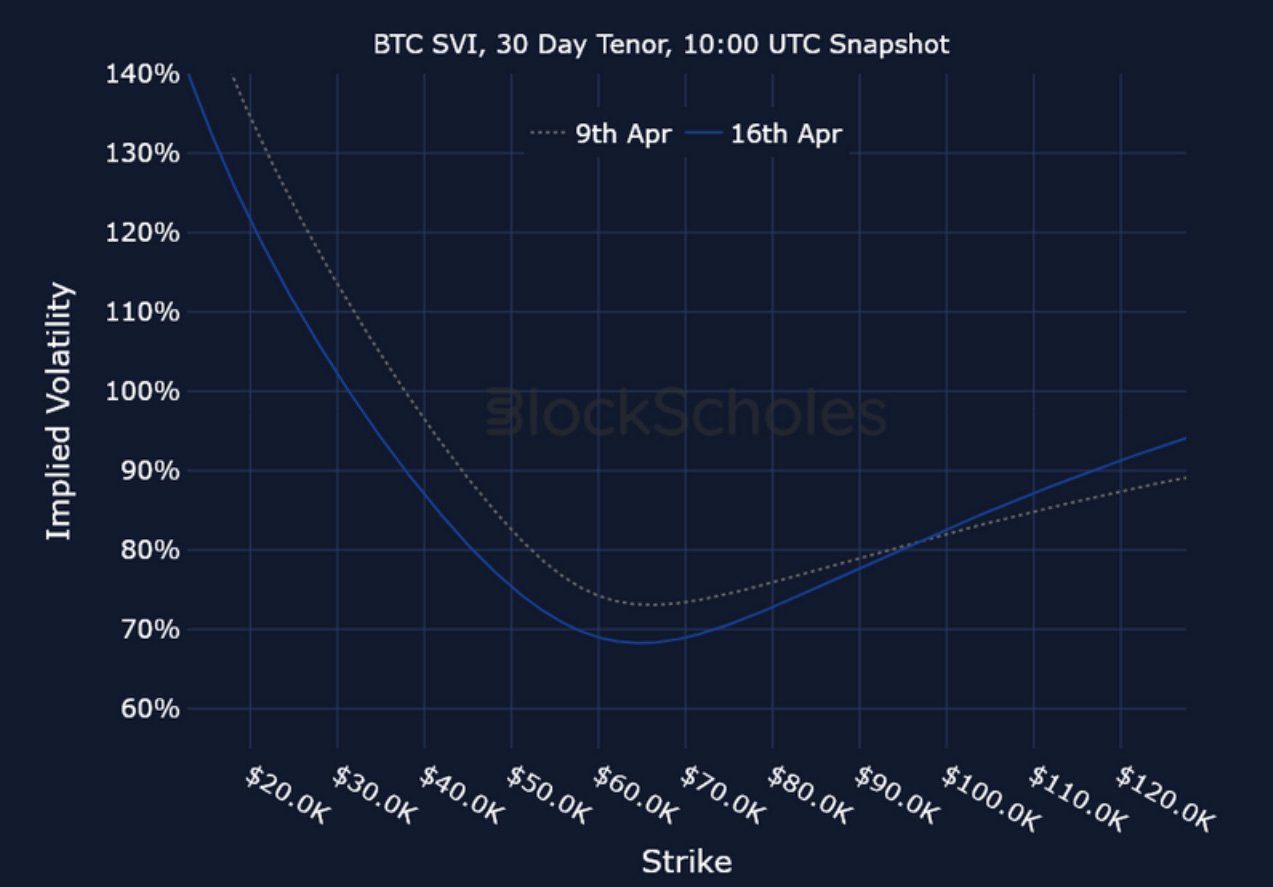

BTC SVI ATM IMPLIED VOLATILITY– short-tenor volatility has risen to invert the term structure once again at the front end.

BTC 25-Delta Risk Reversal – the rise of short-tenor volatility corresponds with their sharp skew towards OTM puts over the same period.

ETH Options

ETH SVI ATM IMPLIED VOLATILITY – shows an inverted term structure at tenors shorter than 2 months, having rallied during the weekend’s selloff.

ETH 25-Delta Risk Reversal – shows a similar skew towards OTM puts at tenors shorter than 3M, without skewing as strongly as in mid-March.

Volatility by Exchange

BTC, 1-MONTH TENOR, SVI CALIBRATION

ETH, 1-MONTH TENOR, SVI CALIBRATION

Put-Call Skew by Exchange

BTC, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

ETH, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

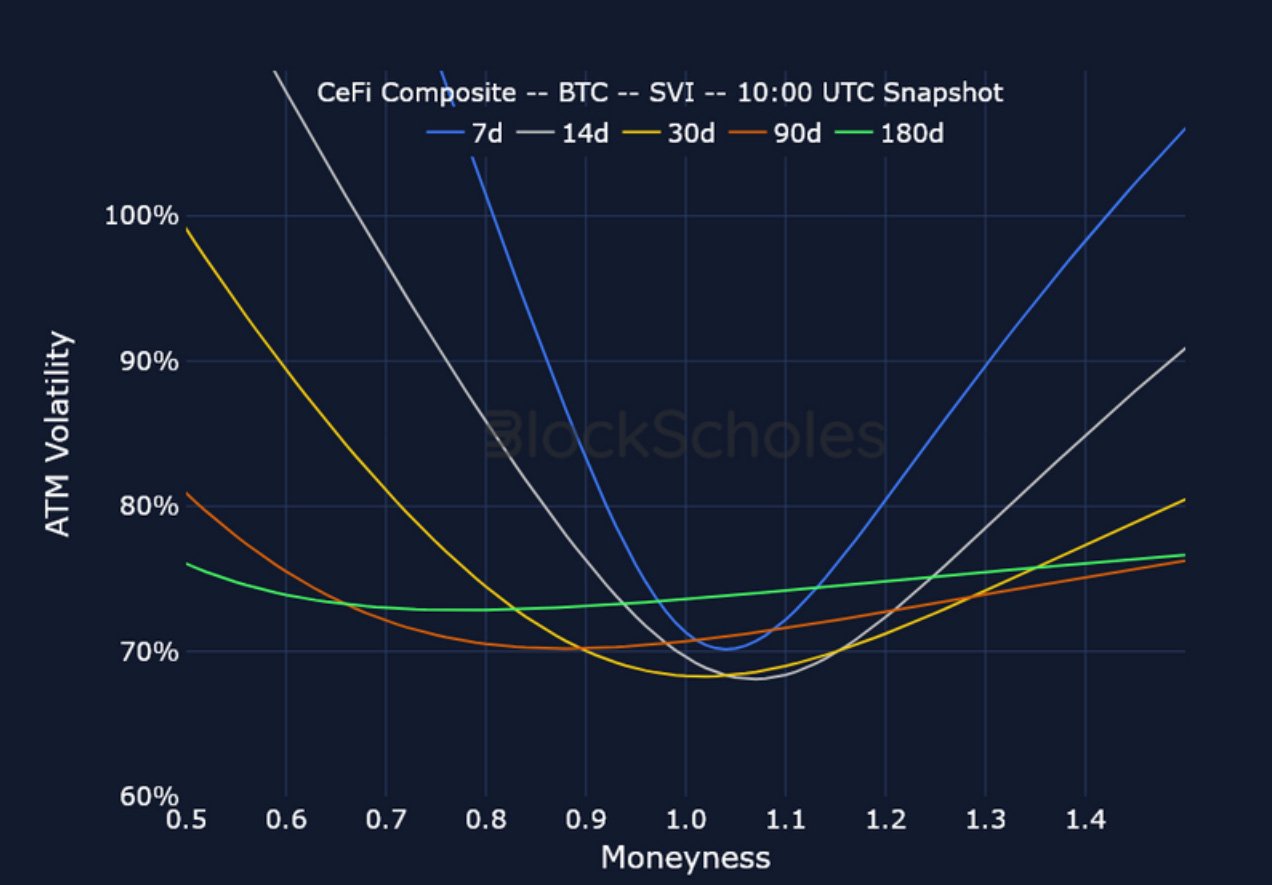

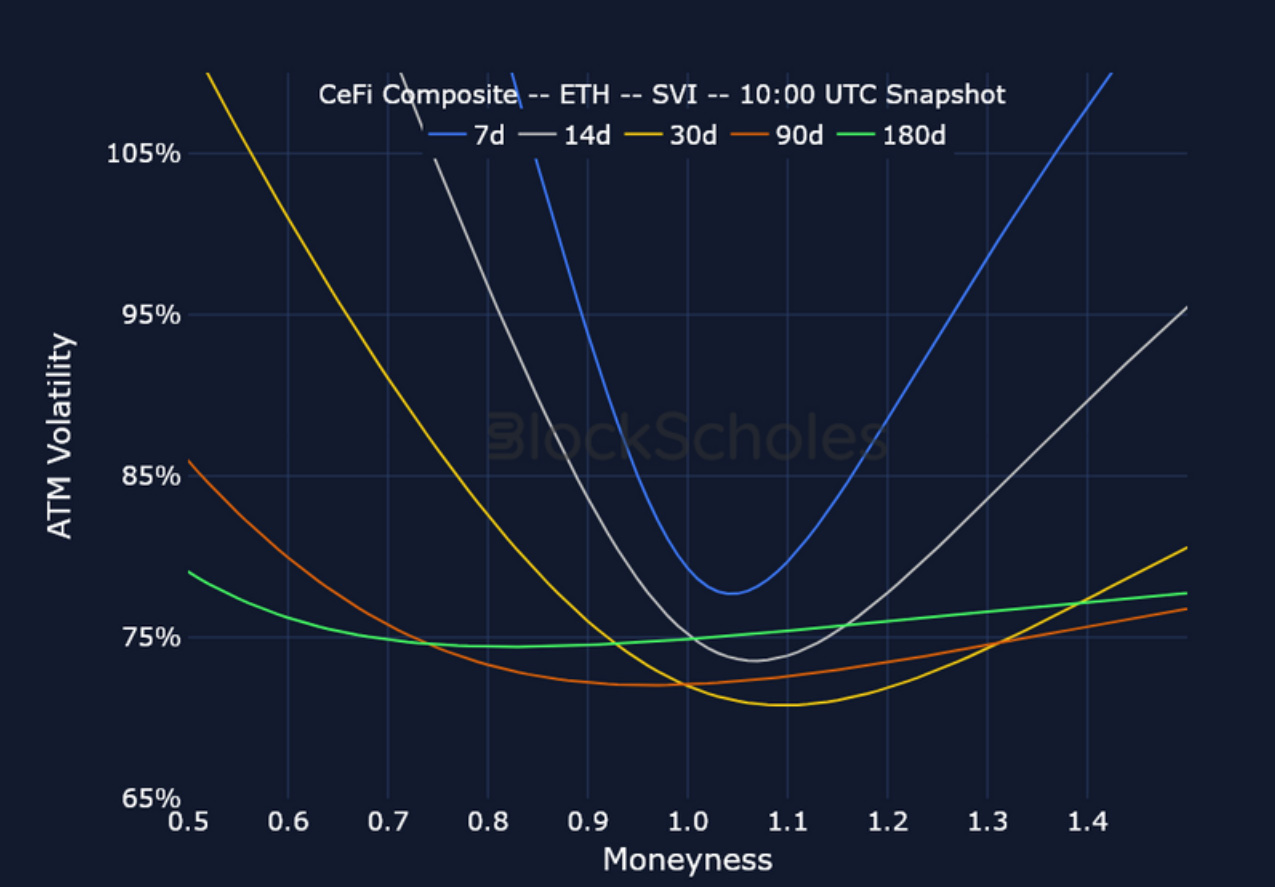

Market Composite Volatility Surface

CeFi COMPOSITE – BTC SVI – 10:00 UTC Snapshot.

CeFi COMPOSITE – ETH SVI – 10:00 UTC Snapshot.

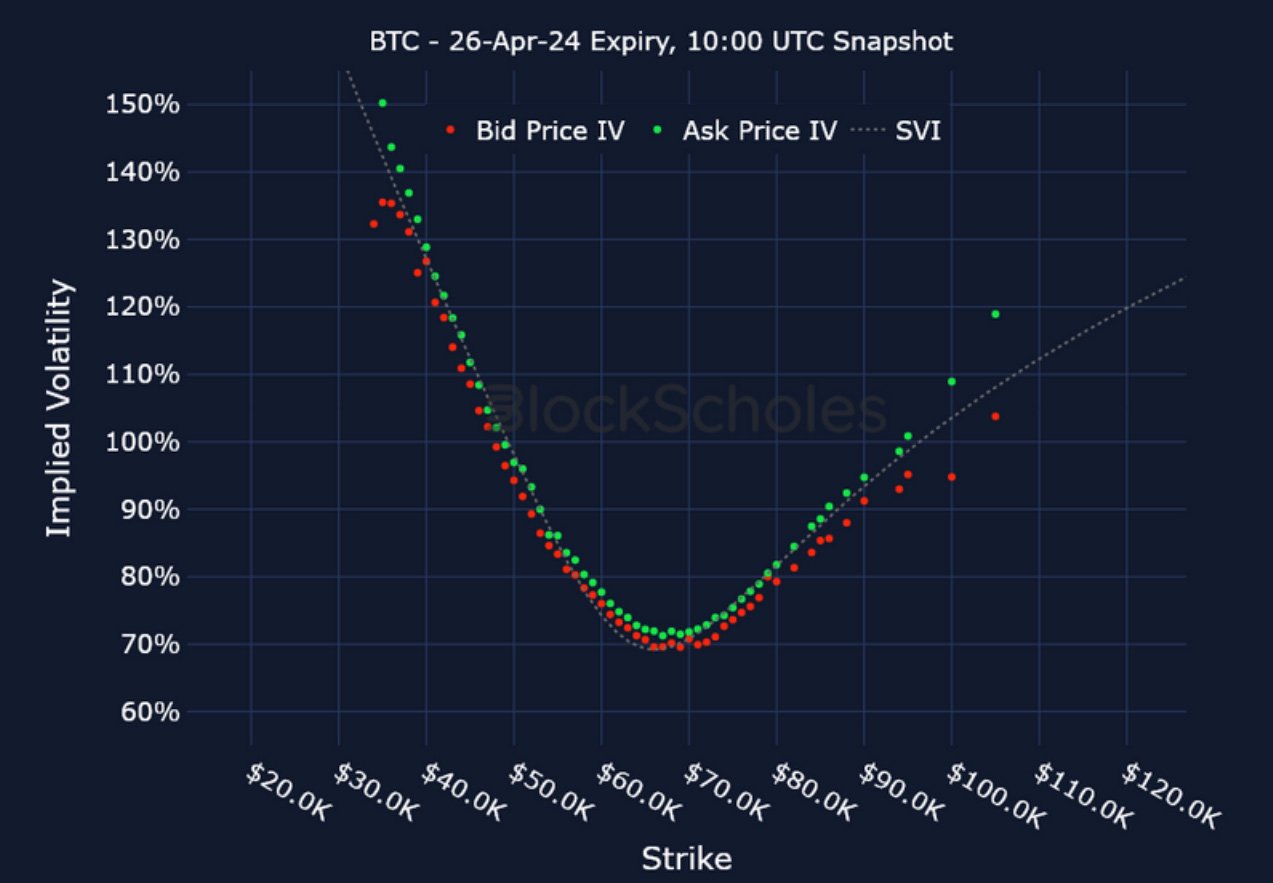

Listed Expiry Volatility Smiles

BTC 26-APR EXPIRY– 10:00 UTC Snapshot.

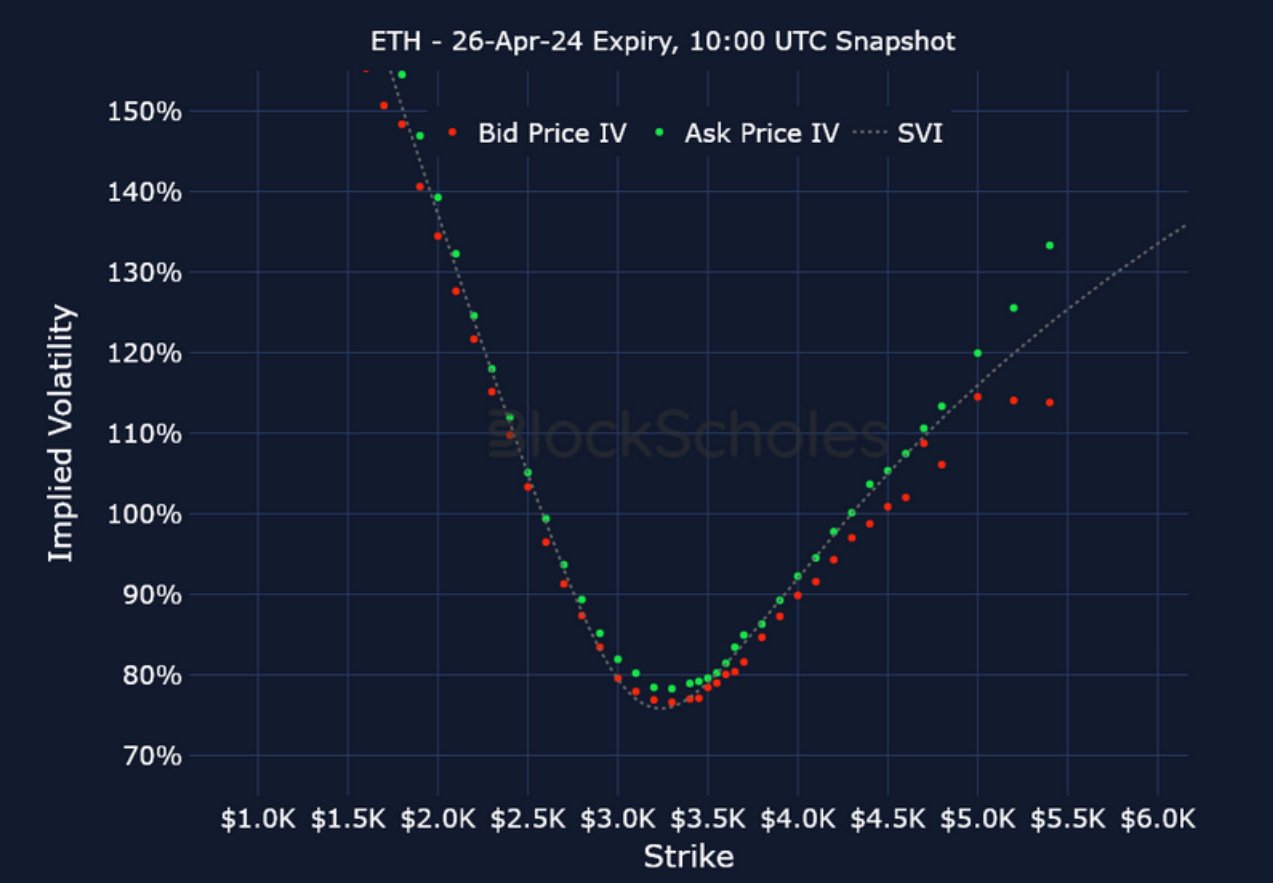

ETH 26-APR EXPIRY – 10:00 UTC Snapshot.

Cross-Exchange Volatility Smiles

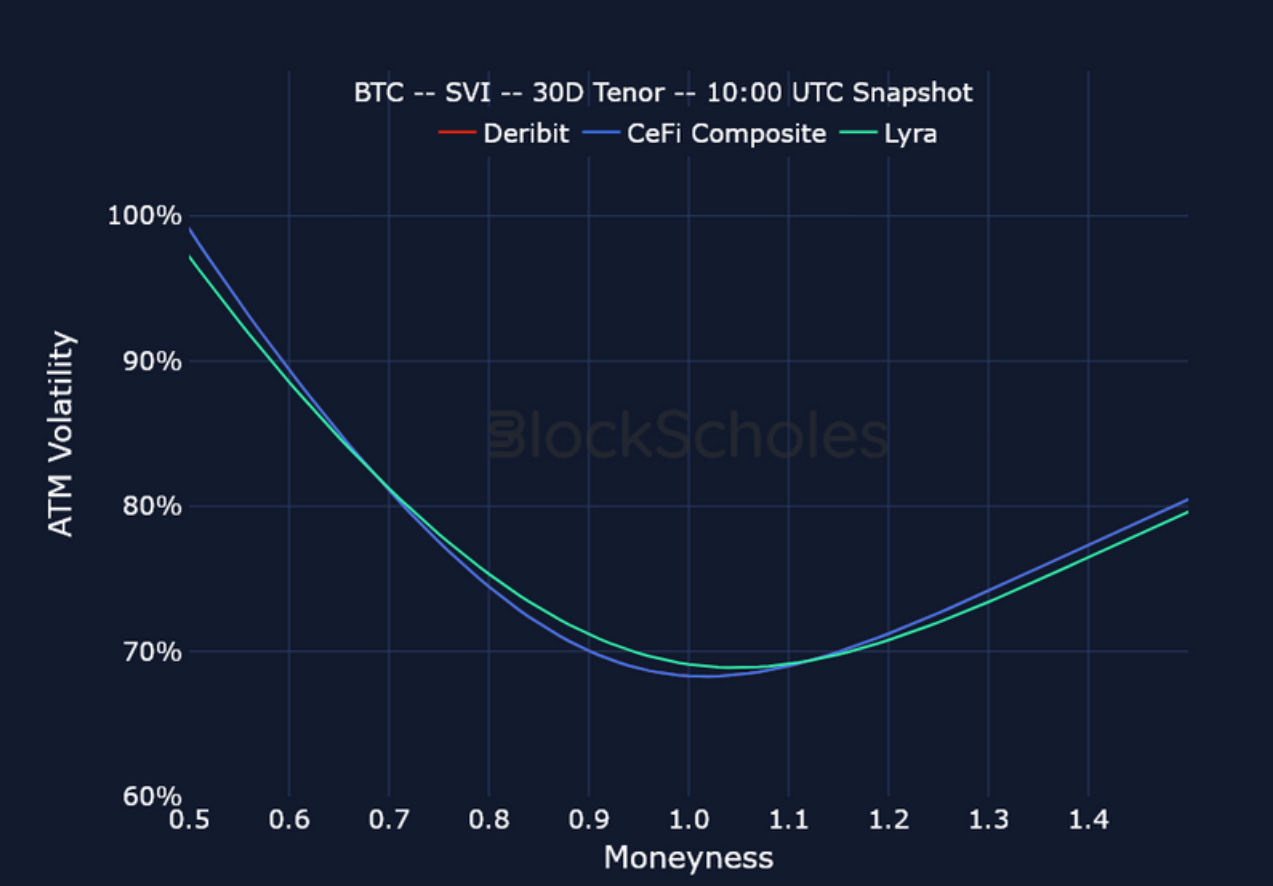

BTC SVI, 30D TENOR – 10:00 UTC Snapshot.

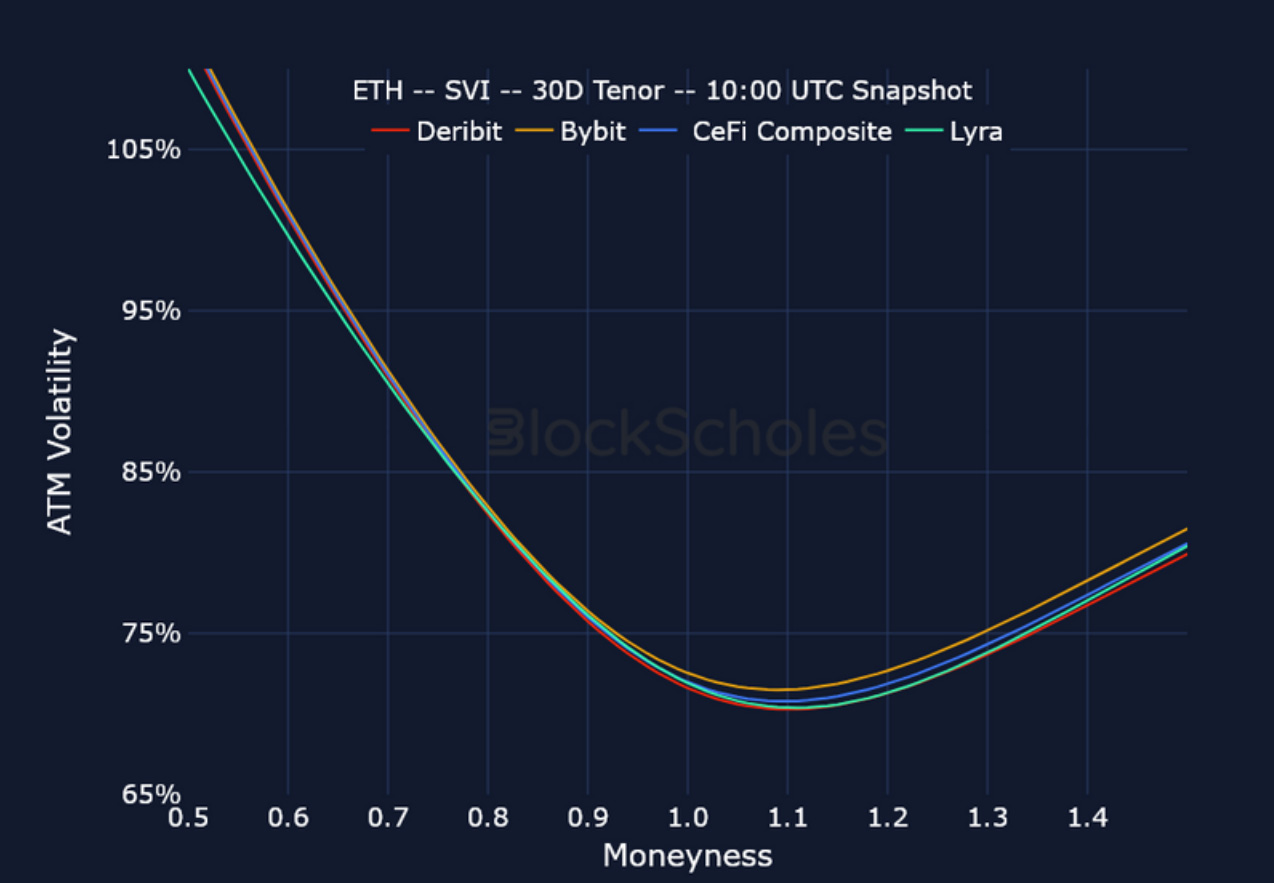

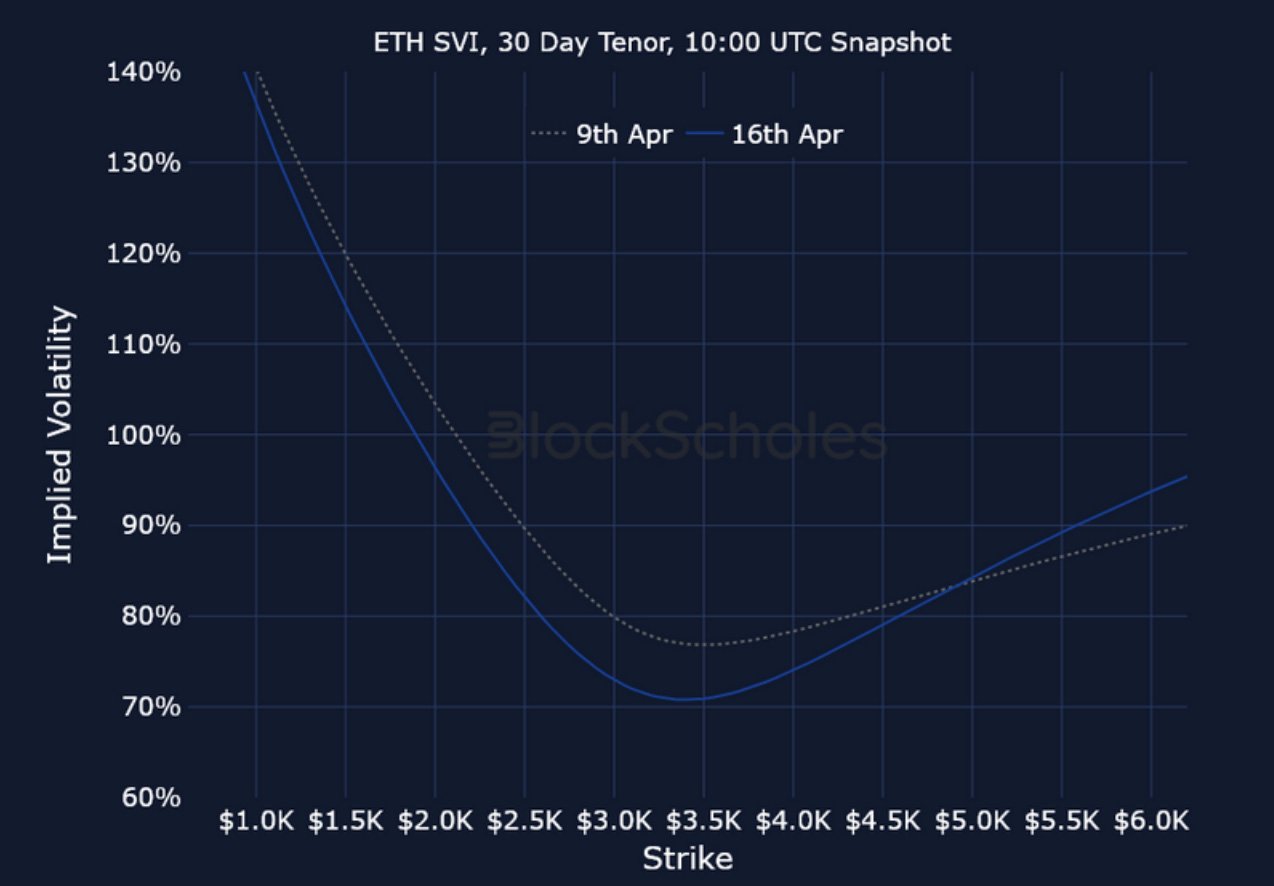

ETH SVI, 30D TENOR – 10:00 UTC Snapshot.

Constant Maturity Volatility Smiles

BTC SVI, 30D TENOR – 10:00 UTC Snapshot.

ETH SVI, 30D TENOR – 10:00 UTC Snapshot.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.