Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

Following the market selloff and the surge in volatility we have witnessed last week, derivatives market sseem to have stabilized. Volatility has dropped for both BTC and ETH at the front end of the term structure, and funding rates returned positive for BTC while slowly rising for ETH. The period of market distress we have observed after the sudden risk-off event appears to have abated for now. However, skew has confirmed the trend we highlighted last week, as longer-dated volatility smiles remain skewed towards OTM calls and shorter tenors show a preference for OTM puts. While sentiment in the long-run still remains bullish, markets still show caution in the short term.

Futures Implied Yield, 1-Month Tenor

ATM Implied Volatility, 1-Month Tenor

Crypto Senti-Meter

BTC Derivatives Sentiment

ETH Derivatives Sentiment

Futures

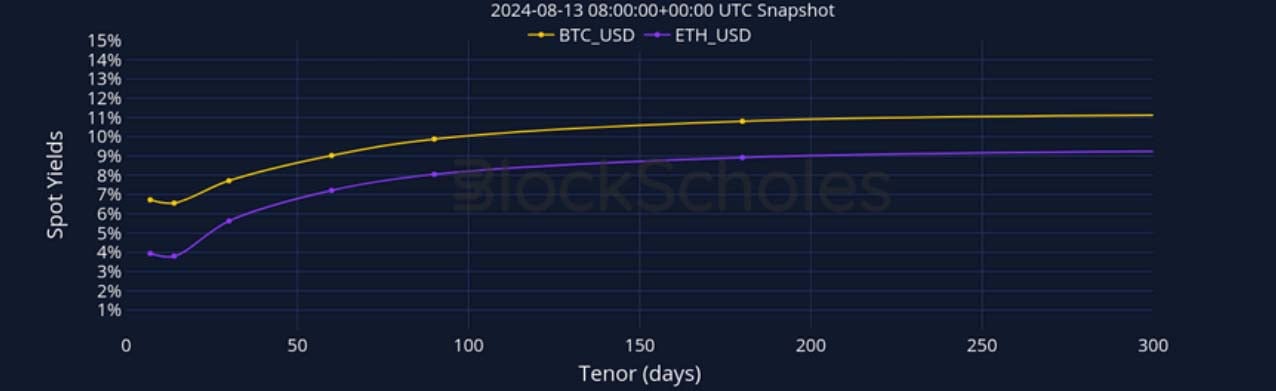

BTC ANNUALISED YIELDS – the curve has steepened slightly as front end yields fall while remaining steady for longer tenors.

ETH ANNUALISED YIELDS – still trade slightly lower than BTC’s at all tenors with a similar steep shape of the term structure.

Perpetual Swap Funding Rate

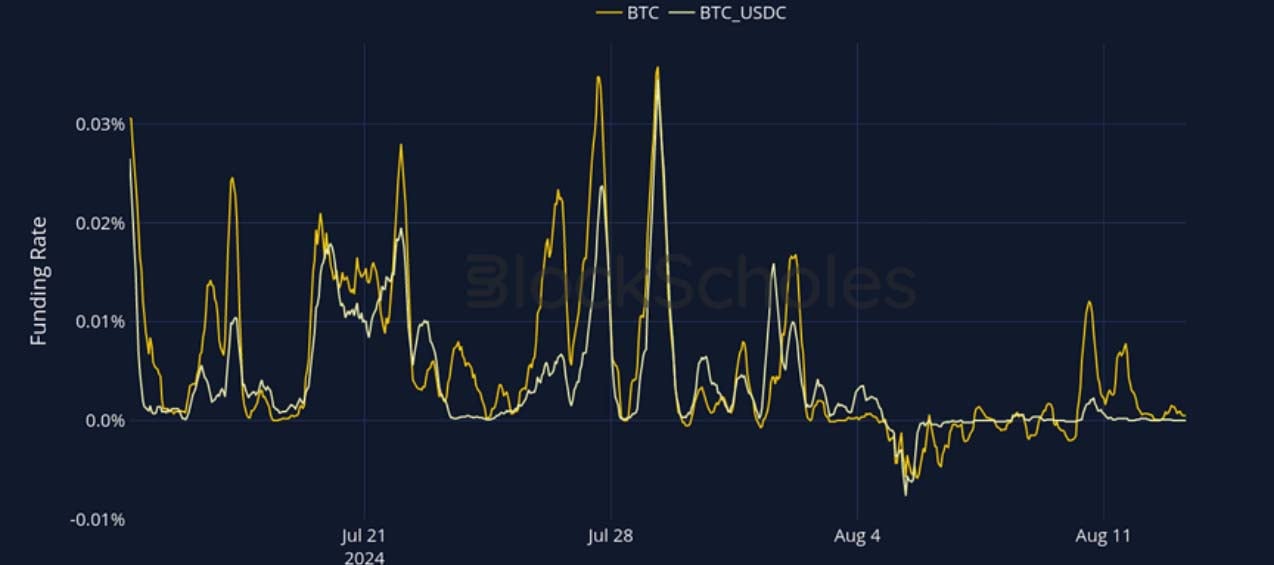

BTC FUNDING RATE – have started trading positive again as traders enter express demand for long exposure.

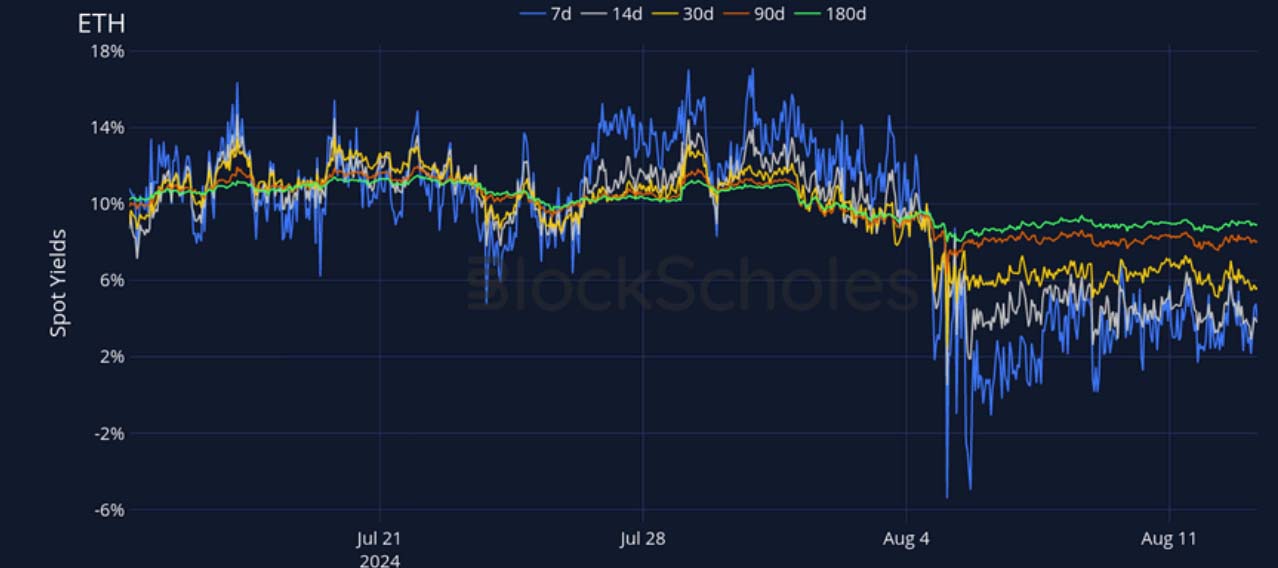

ETH FUNDING RATE – is still trading negative but slowly recovering.

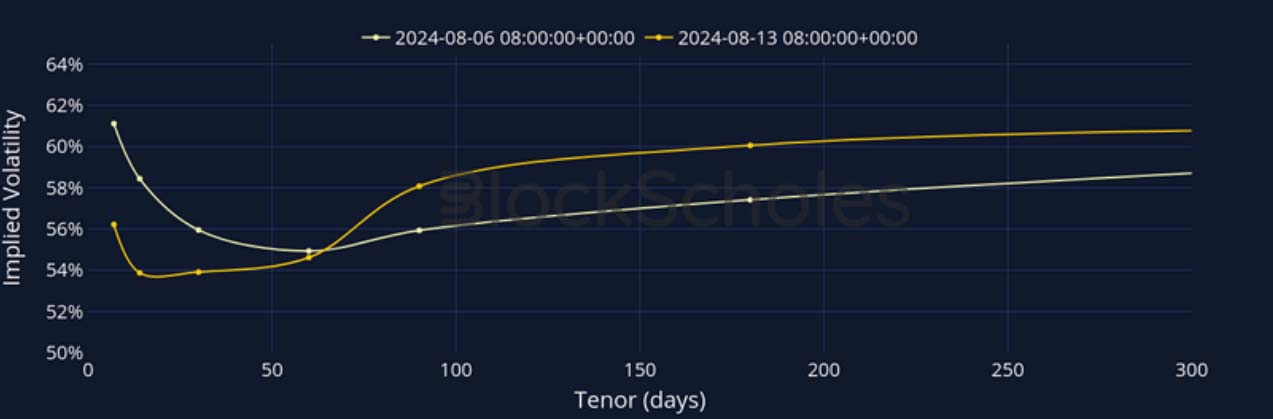

BTC Options

BTC SVI ATM IMPLIED VOLATILITY – volatility levels have dropped for short tenors while increasing for longer ones.

BTC 25-Delta Risk Reversal – is showing the same trend we have observed after the selloff, as longer-tenor smiles remained steadfastly call-skewed.

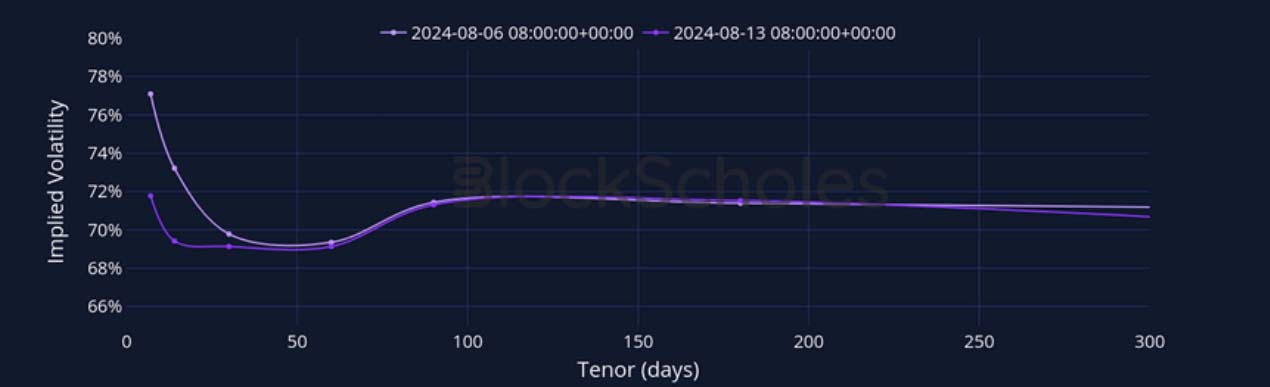

ETH Options

ETH SVI ATM IMPLIED VOLATILITY -shows a decrease in premia for short tenors, while remaining constant for long-term ones.

ETH 25-Delta Risk Reversal – the magnitude of skew for short tenors has been strongly oscillating while remaining negative.

Volatility by Exchange

BTC, 1-MONTH TENOR, SVI CALIBRATION

ETH, 1-MONTH TENOR, SVI CALIBRATION

Put-Call Skew by Exchange

BTC, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

ETH, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

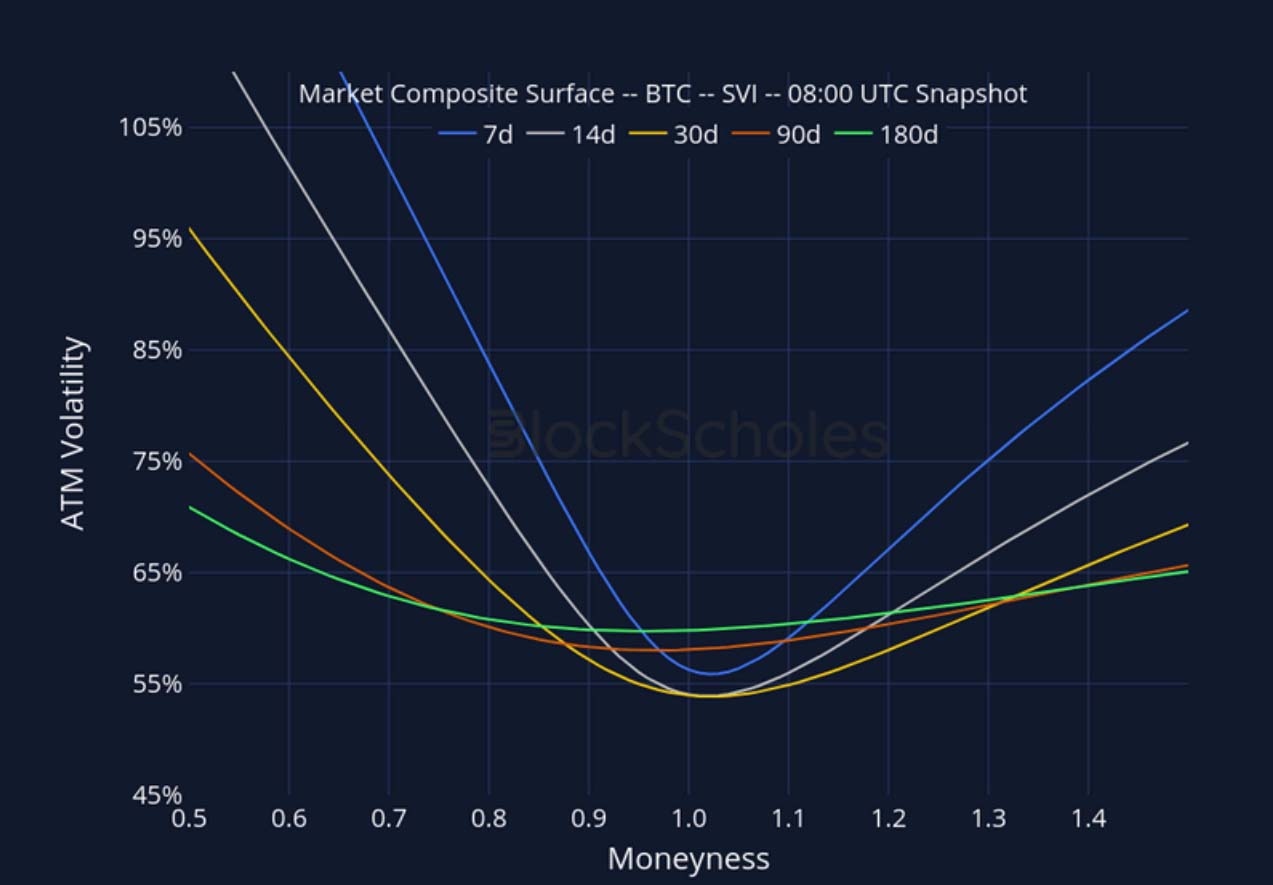

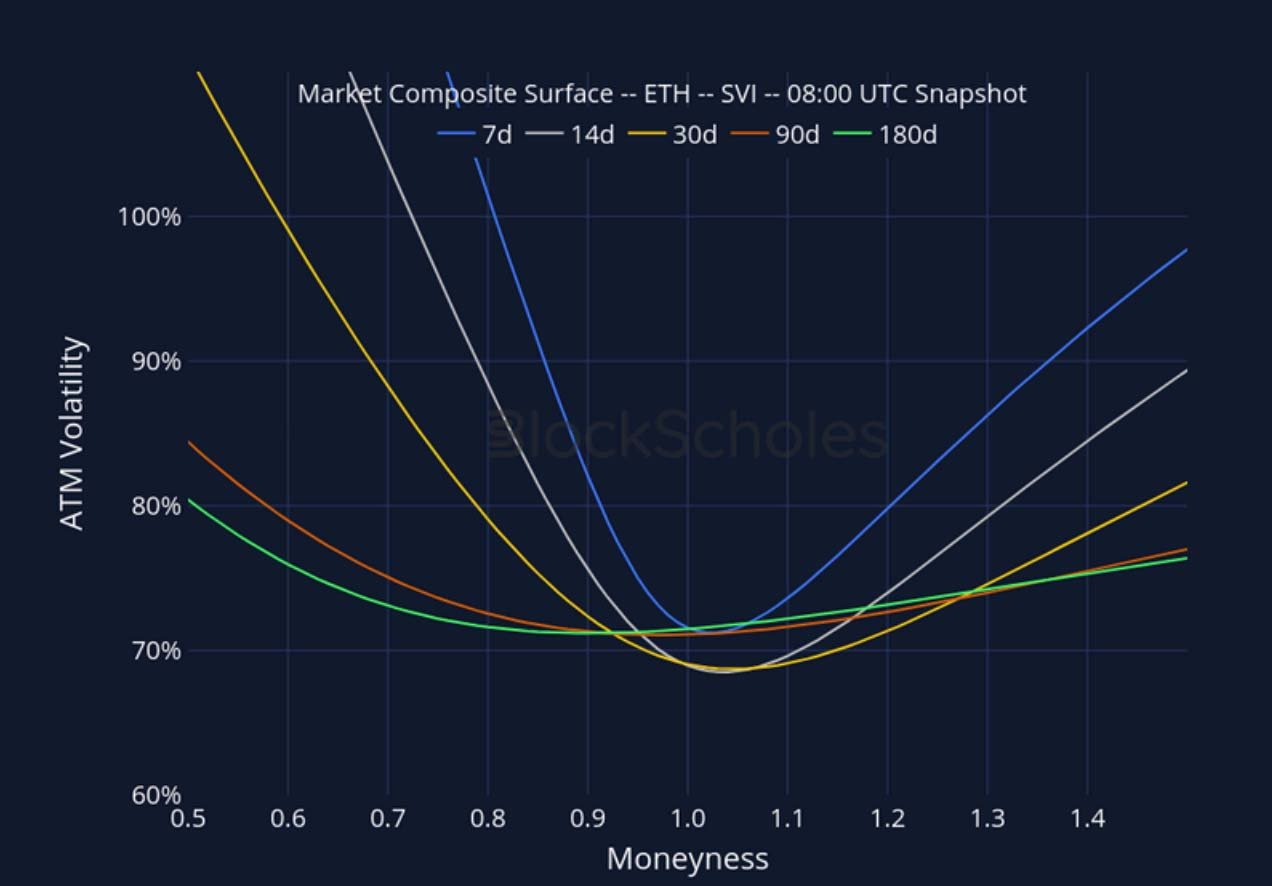

Market Composite Volatility Surface

CeFi COMPOSITE – BTC SVI – 8:00 UTC Snapshot.

CeFi COMPOSITE – ETH SVI – 8:00 UTC Snapshot.

Listed Expiry Volatility Smiles

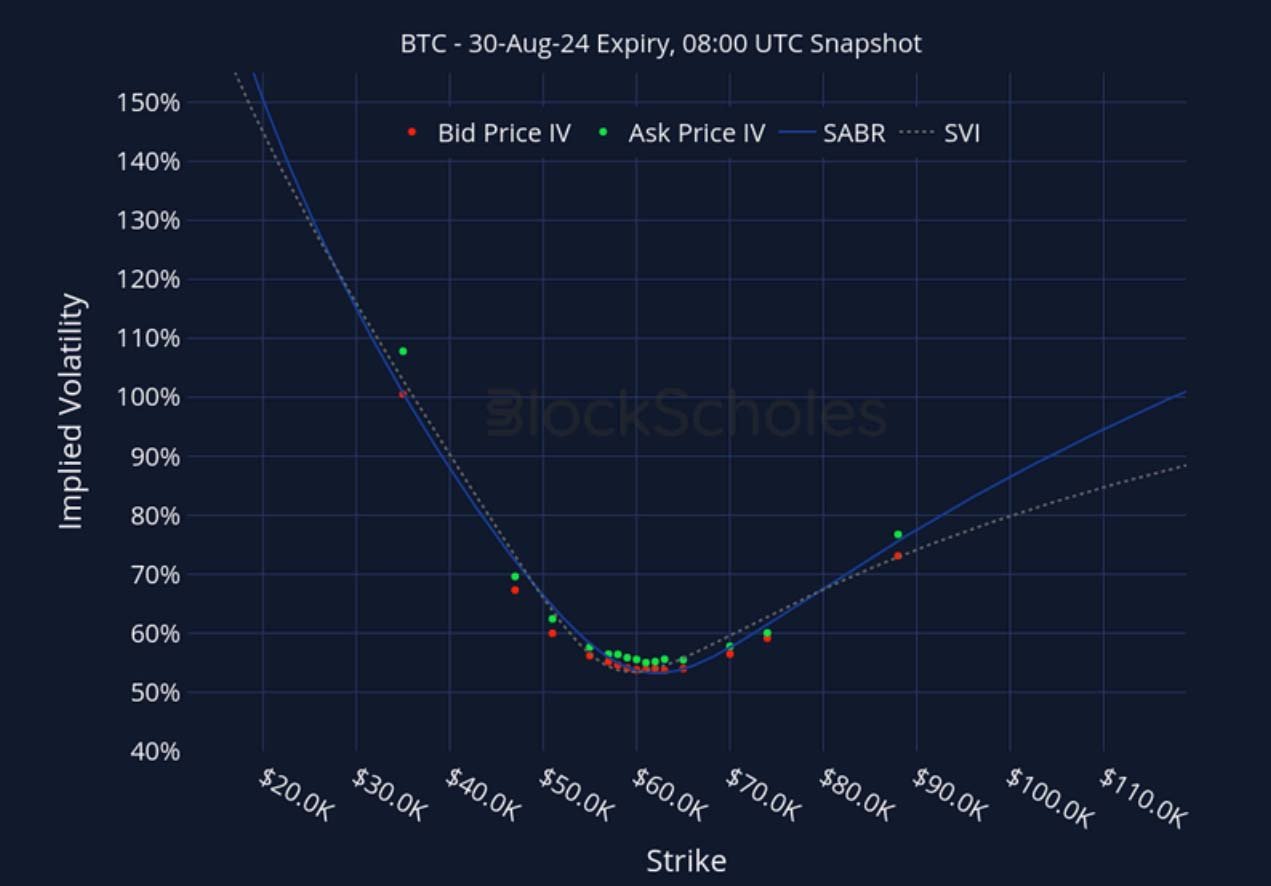

BTC 30-AUG EXPIRY – 8:00 UTC Snapshot.

ETH 30-AUG EXPIRY – 8:00 UTC Snapshot.

Cross-Exchange Volatility Smiles

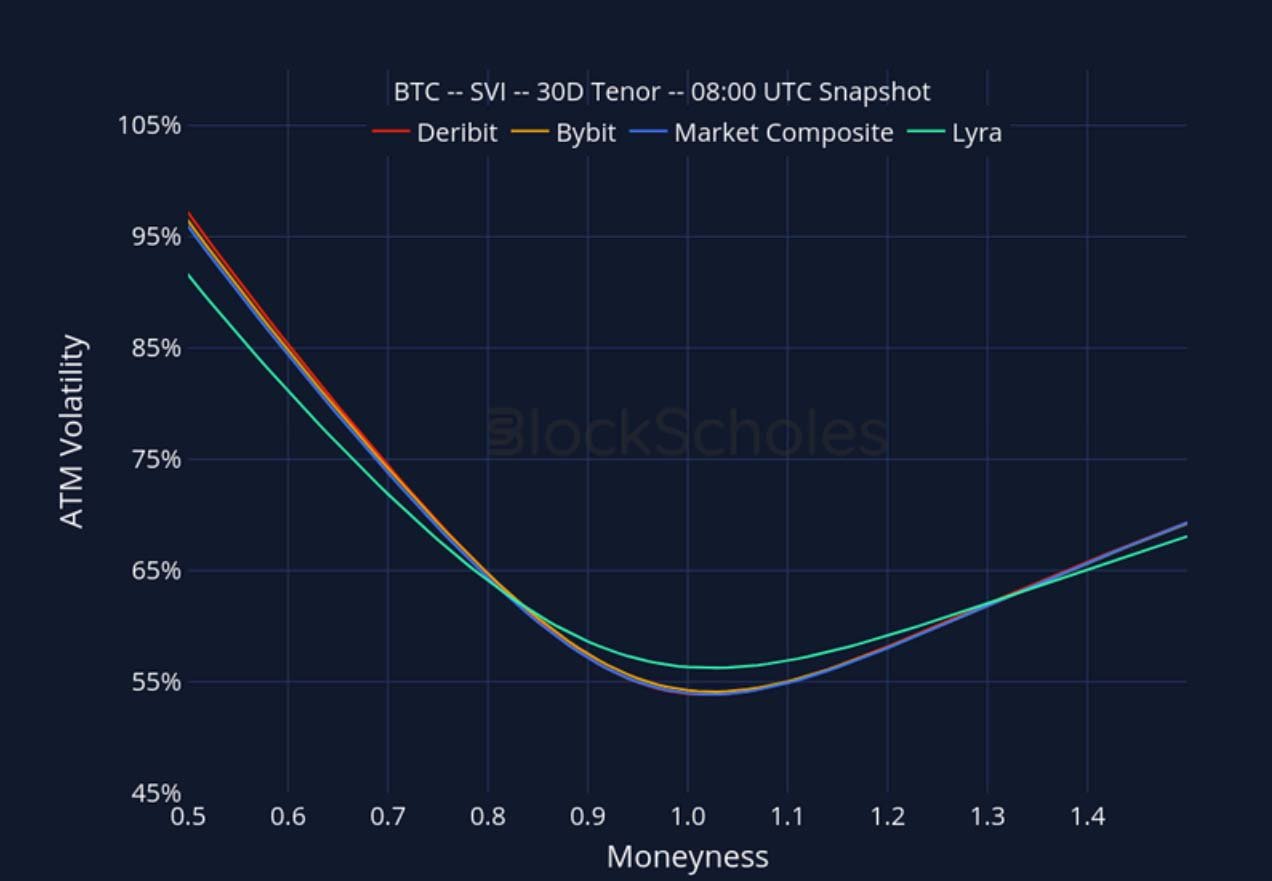

BTC SVI, 30D TENOR – 8:00 UTC Snapshot.

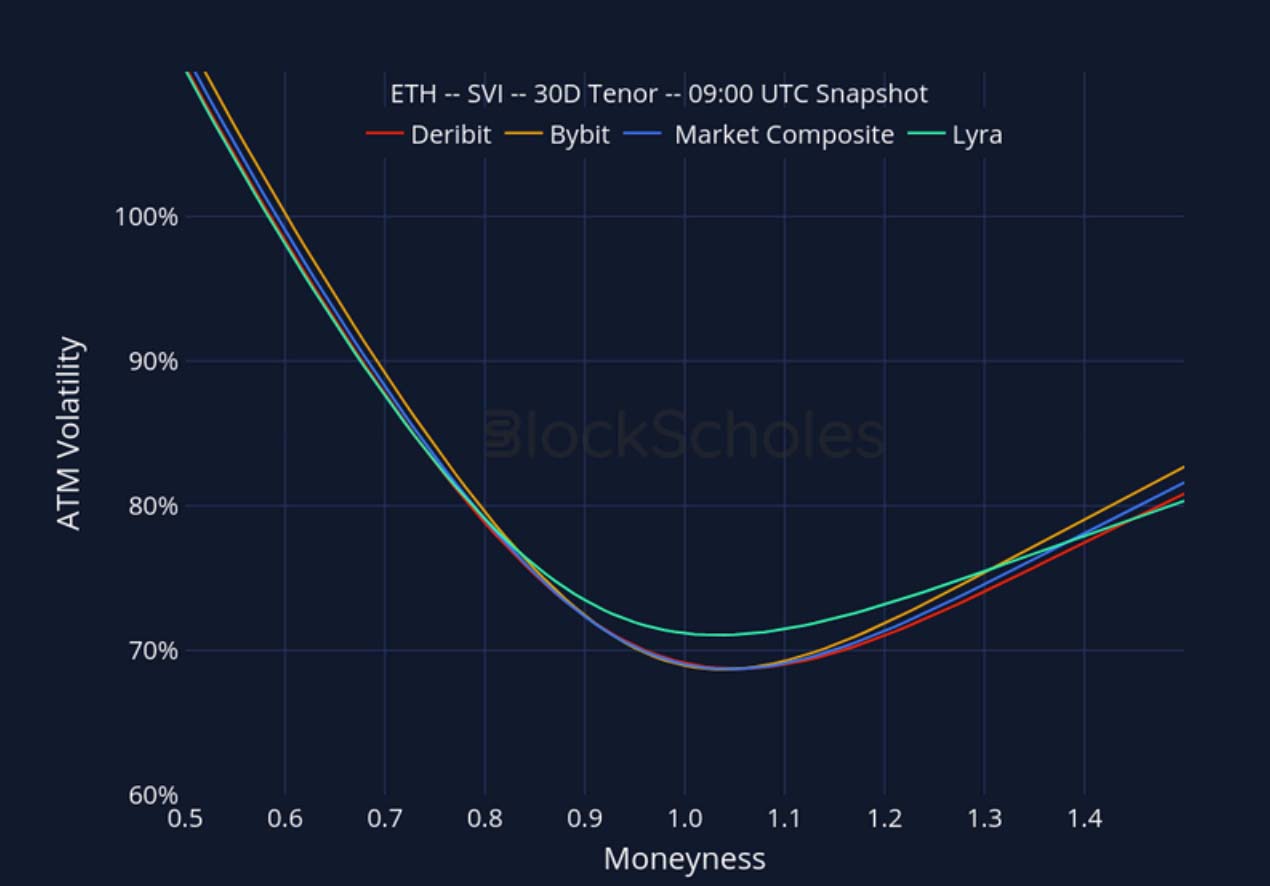

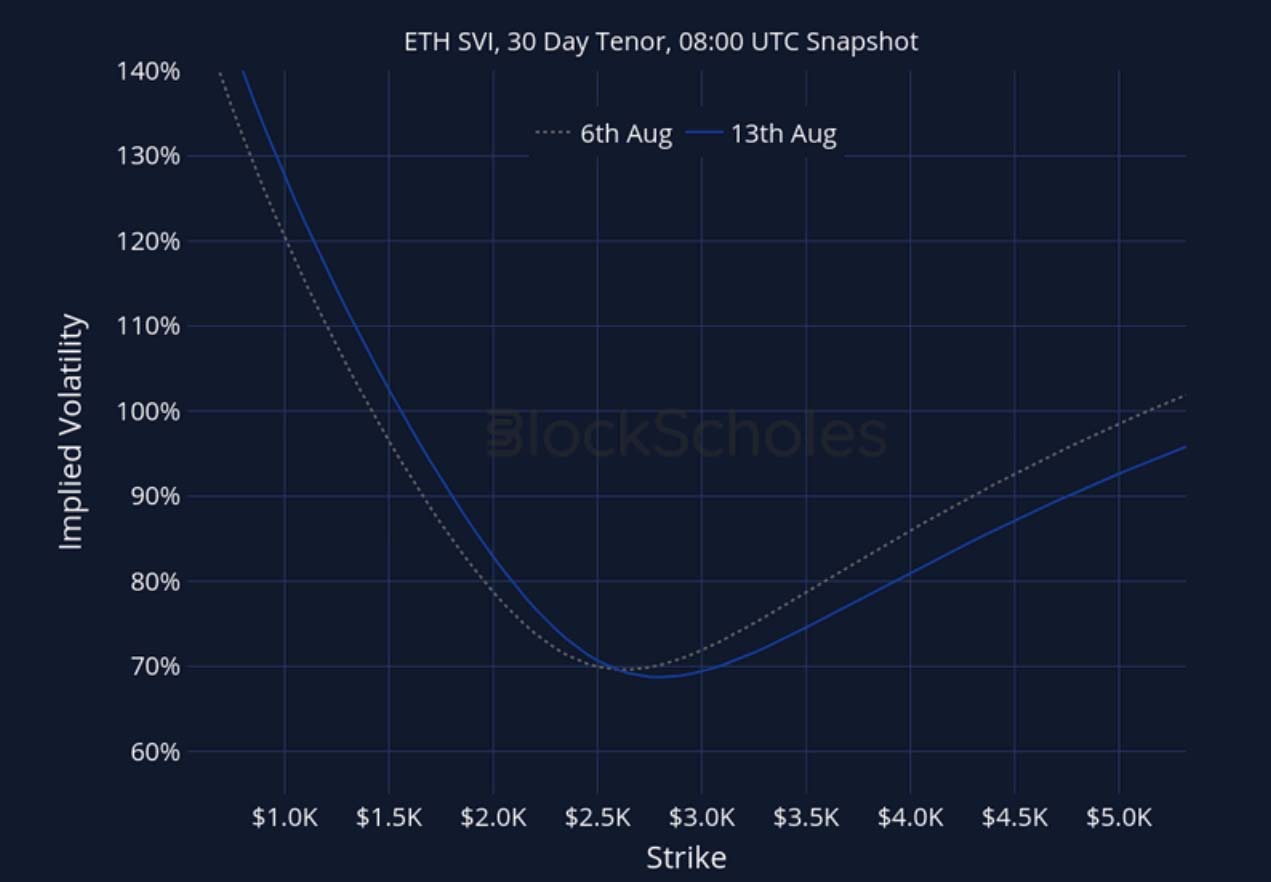

ETH SVI, 30D TENOR – 8:00 UTC Snapshot.

Constant Maturity Volatility Smiles

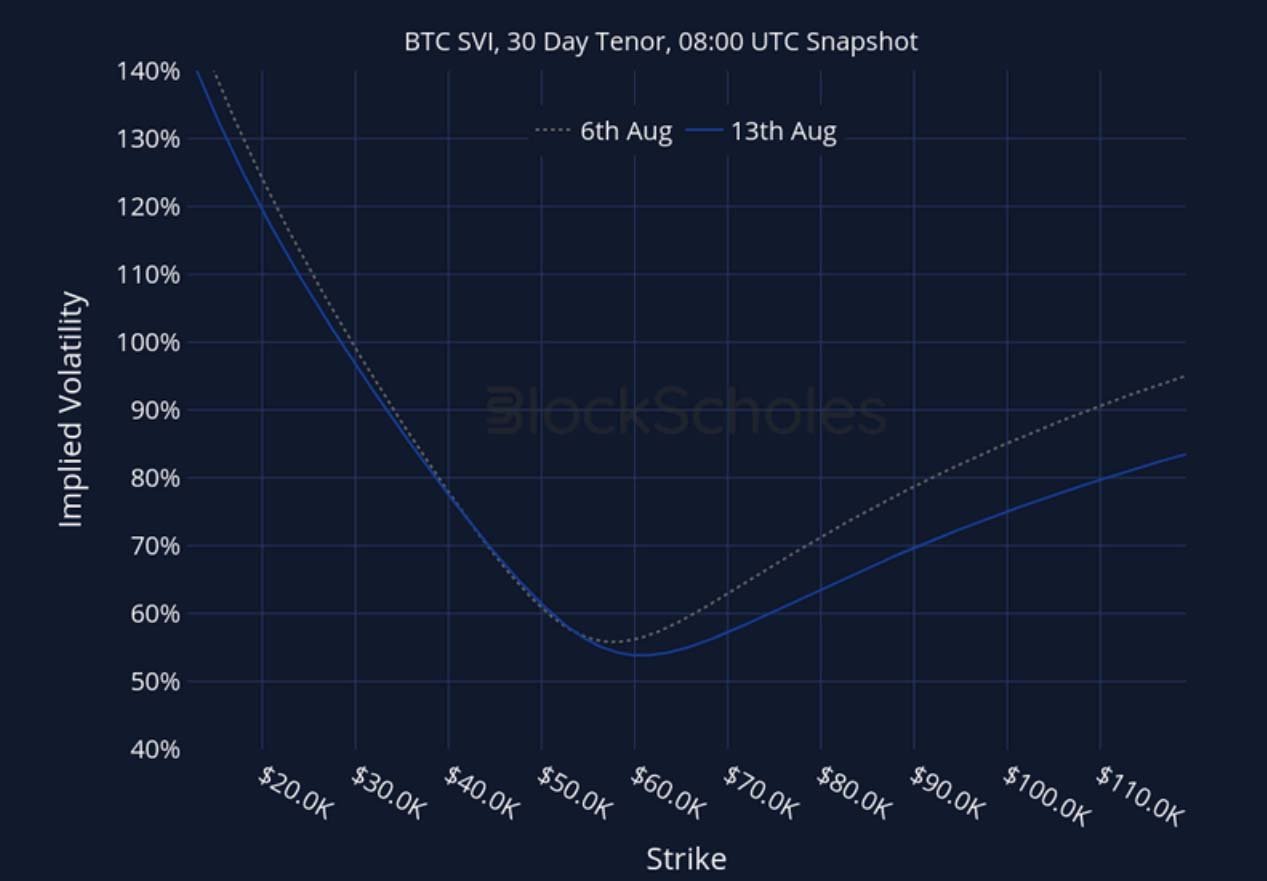

BTC SVI, 30D TENOR – 8:00 UTC Snapshot.

ETH SVI, 30D TENOR – 8:00 UTC Snapshot.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.