Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

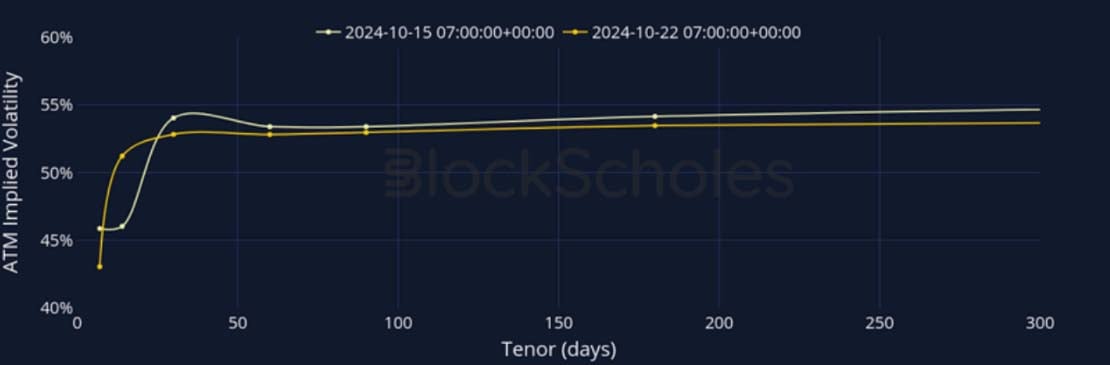

The positive sentiment observed last week has consolidated, with bullishness reflected across key metrics for both majors. Perpetual funding rates remain positive, implied futures yields continue to show elevated levels and an inverted term structure, and the implied volatility smiles’ skew remains strongly tilted toward calls across tenors. The upcoming election is still impacting market dynamics greatly, with implied volatility for 14-day tenor options in both ETH and BTC rising, now approaching levels seen in longer-tenor options. At the same time, volatility at the far end of the term structure continues to trend sideways, only showing a slight decrease for BTC options. Notably, 7-day tenor options saw a spike in volatility last week, now having dropped sharply and sitting lower than last week.

Futures Implied Yield, 1-Month Tenor

ATM Implied Volatility, 1-Month Tenor

Crypto Senti-Meter

BTC Derivatives Sentiment

ETH Derivatives Sentiment

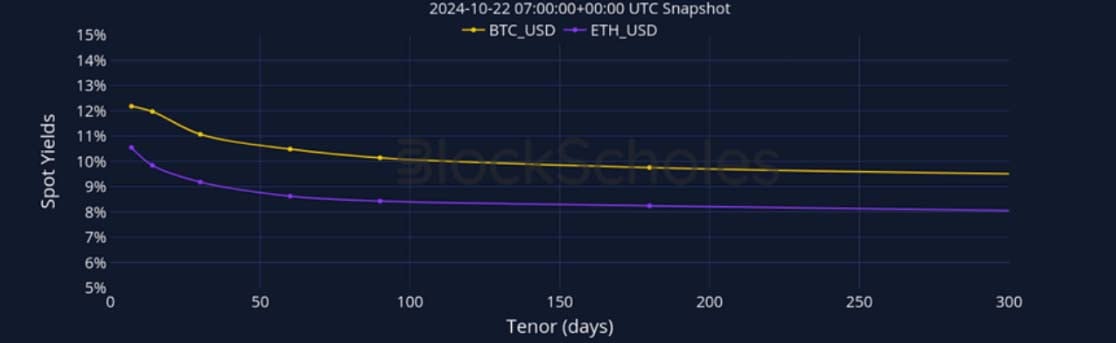

Futures

BTC ANNUALISED YIELDS – The term structure remains inverted as last week, but the front end has decreased resulting in a flattened curve.

ETH ANNUALISED YIELDS – ETH’s futures yield term structure has disinverted and re-inverted over the past week, returning to a similar state as last week.

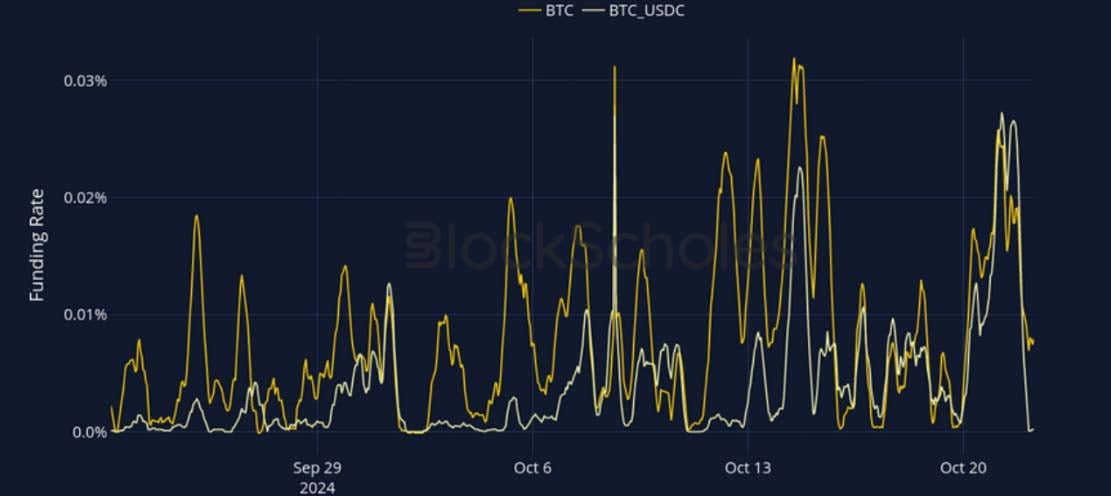

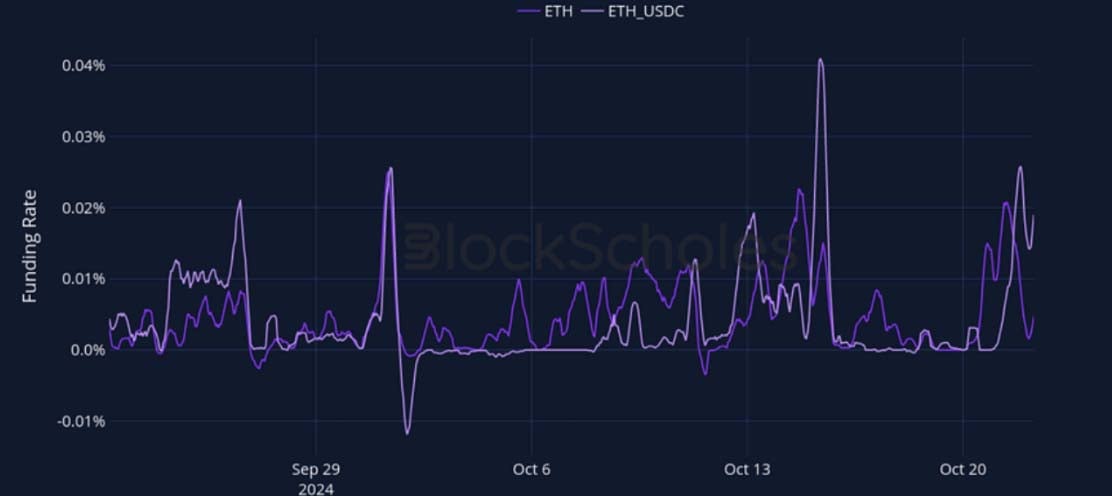

Perpetual Swap Funding Rate

BTC FUNDING RATE – BTC’s perpetual funding rate has fluctuated at positive levels over the past week.

ETH FUNDING RATE – ETH’s perpetual swap funding rate is exhibiting positive sentiment similarly to BTC’s.

BTC Options

BTC SVI ATM IMPLIED VOLATILITY – Volatility continues to rise at the front end of the term structure, with 14-day tenor options showing elevated levels.

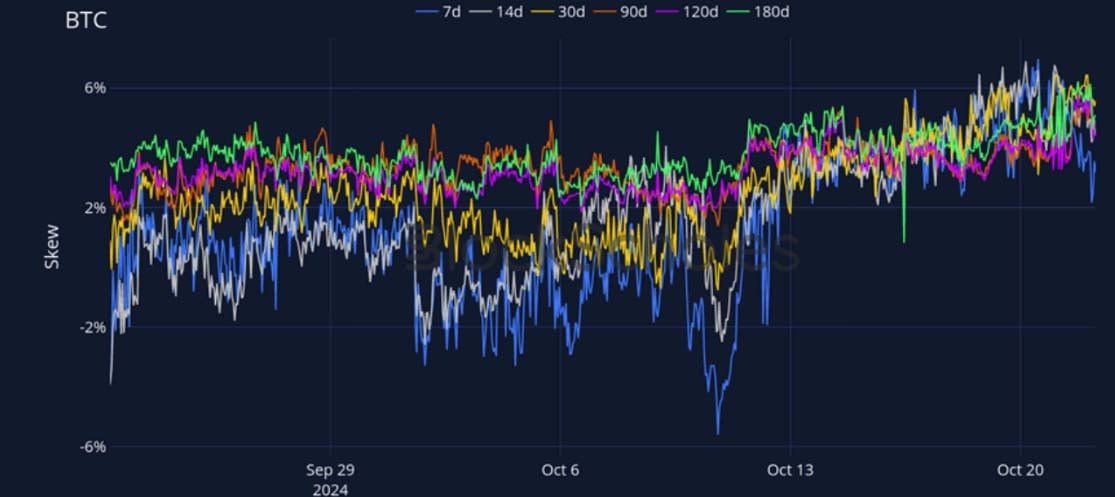

BTC 25-Delta Risk Reversal – Option smiles have maintained a strong skew towards calls, with the skew increasing slightly compared to last week.

ETH Options

ETH SVI ATM IMPLIED VOLATILITY – Implied volatility for ETH 14-day tenor options has risen, mirroring the increase seen in BTC ahead of the US election.

ETH 25-Delta Risk Reversal – ETH’s implied volatility smiles are still exhibiting a strong call-skew across tenors.

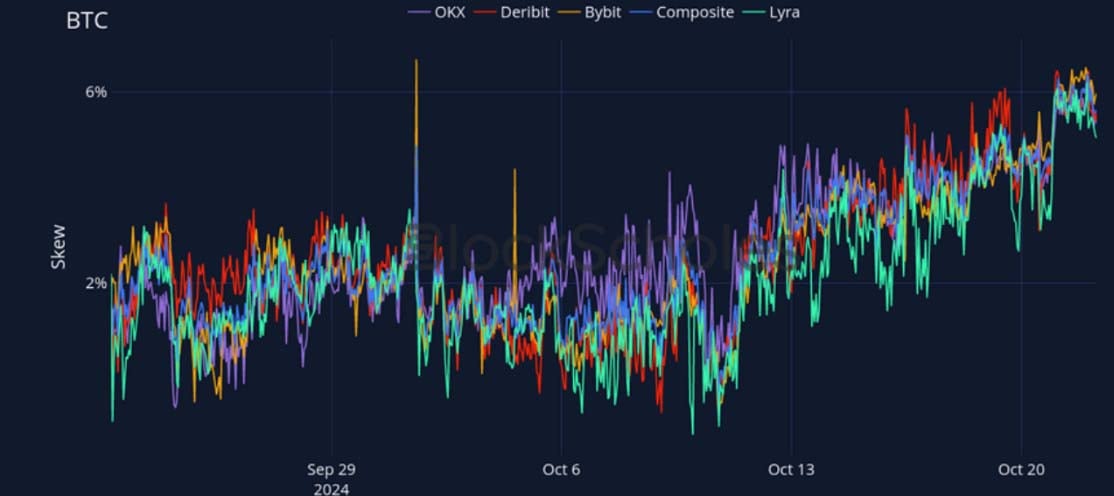

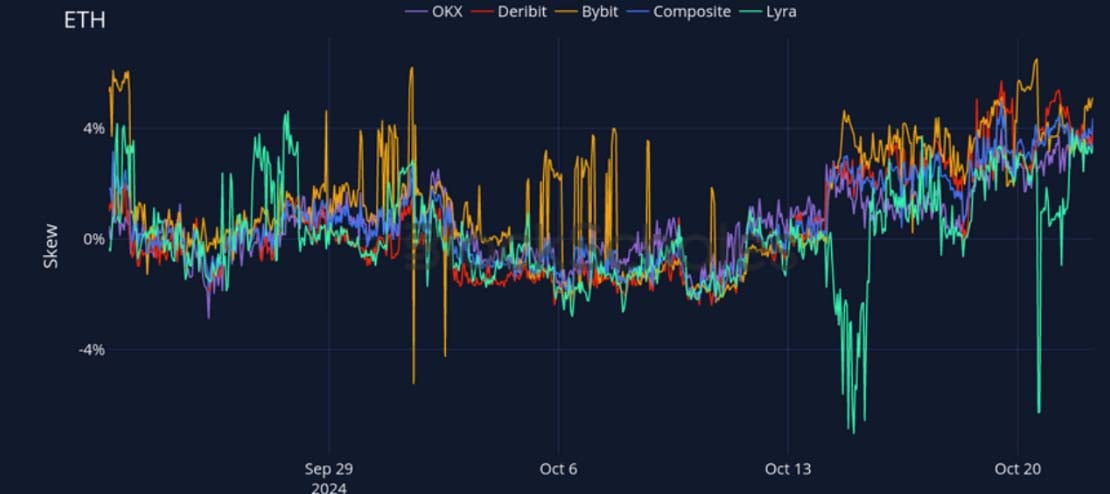

Volatility by Exchange

BTC, 1-MONTH TENOR, SVI CALIBRATION

ETH, 1-MONTH TENOR, SVI CALIBRATION

Put-Call Skew by Exchange

BTC, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

ETH, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

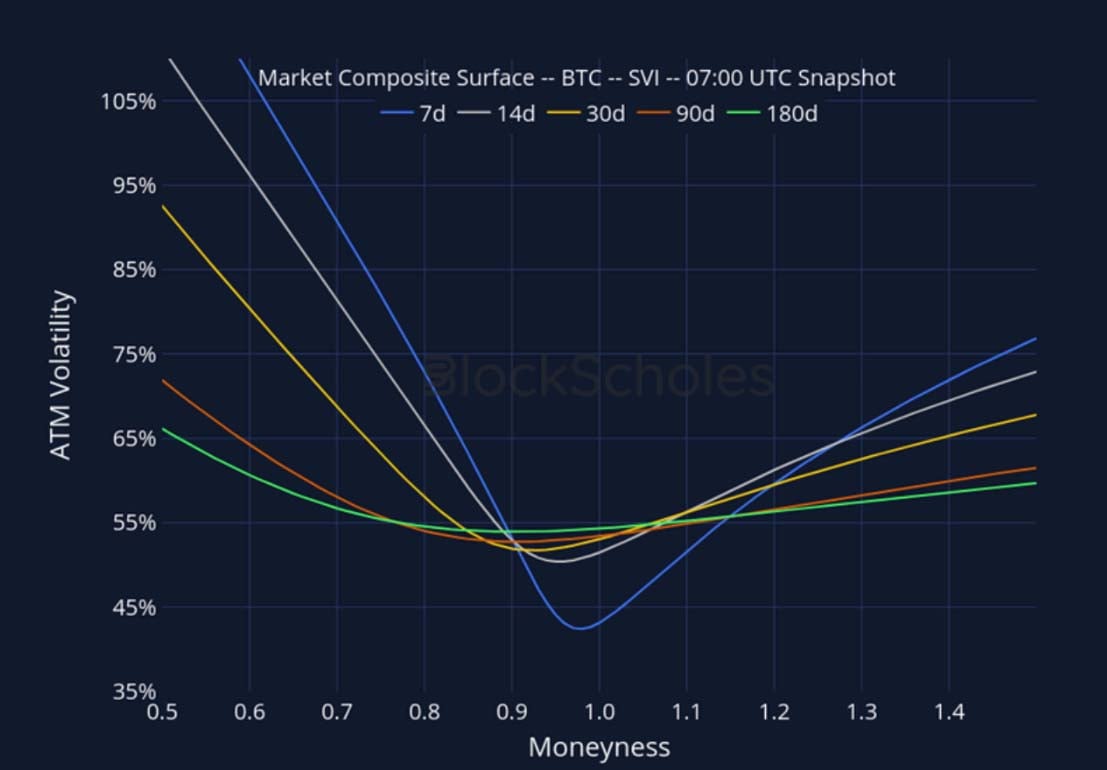

Market Composite Volatility Surface

CeFi COMPOSITE – BTC SVI – 7:00 UTC Snapshot.

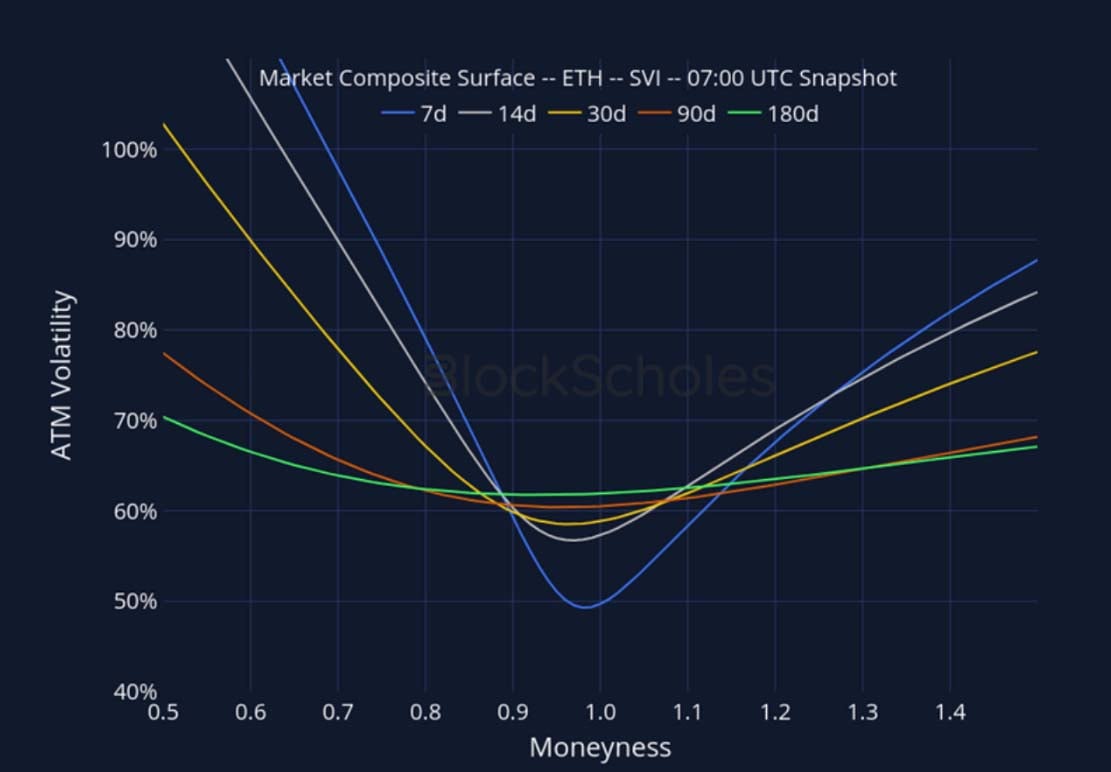

CeFi COMPOSITE – ETH SVI – 7:00 UTC Snapshot.

Listed Expiry Volatility Smiles

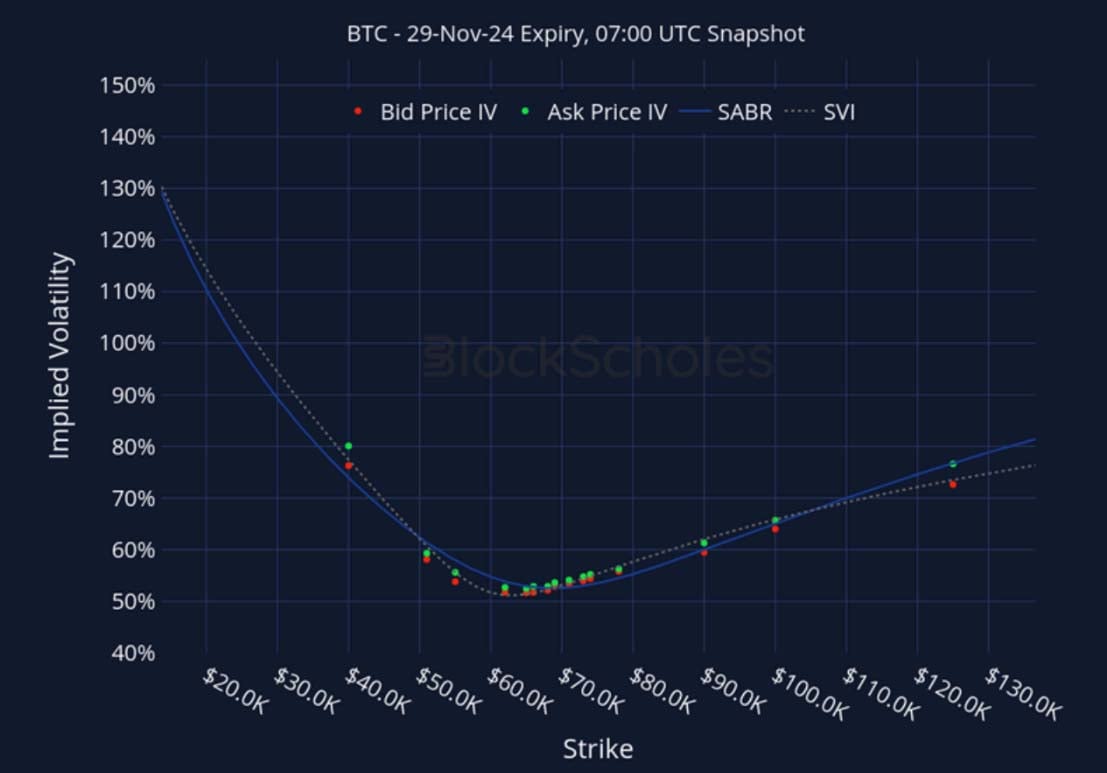

BTC 29-NOV EXPIRY – 7:00 UTC Snapshot.

ETH 29-NOV EXPIRY – 7:00 UTC Snapshot.

Cross-Exchange Volatility Smiles

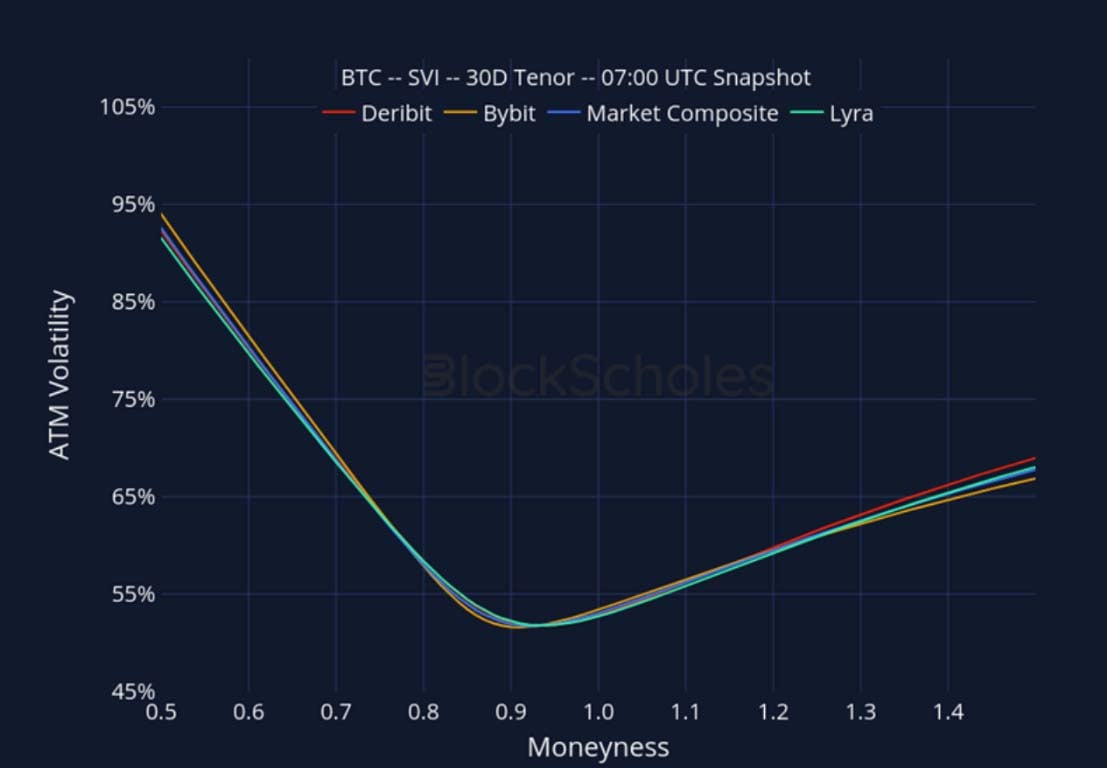

BTC SVI, 30D TENOR – 7:00 UTC Snapshot.

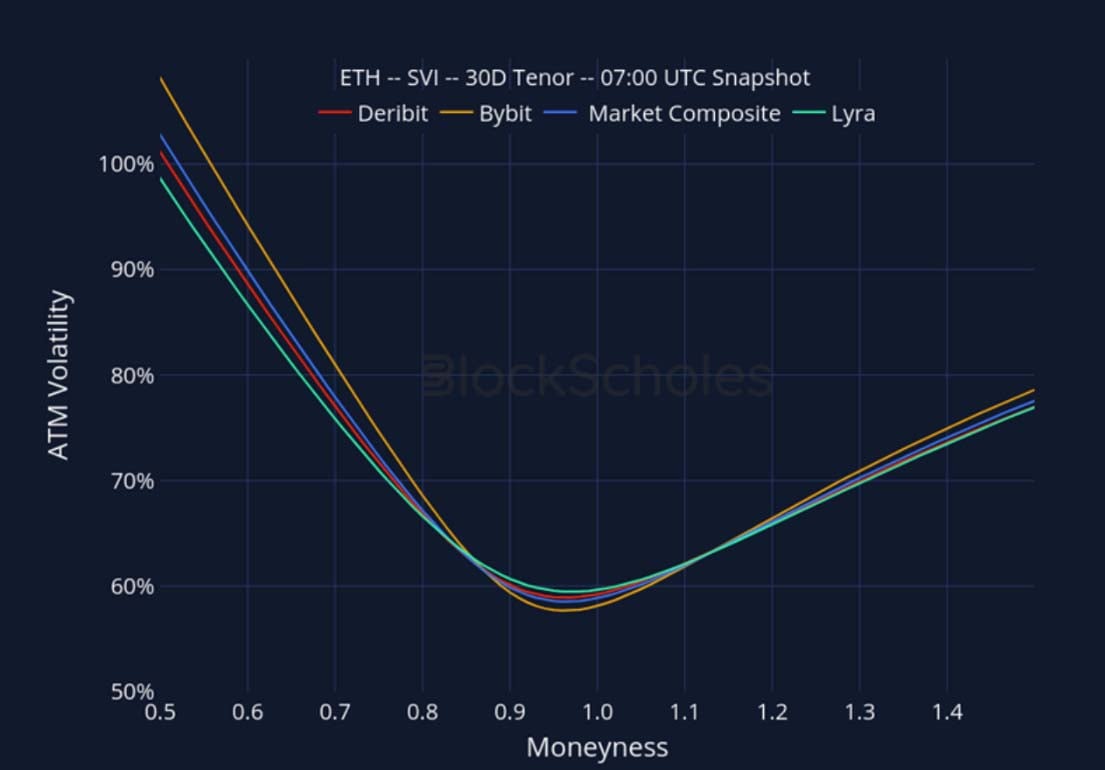

ETH SVI, 30D TENOR – 7:00 UTC Snapshot.

Constant Maturity Volatility Smiles

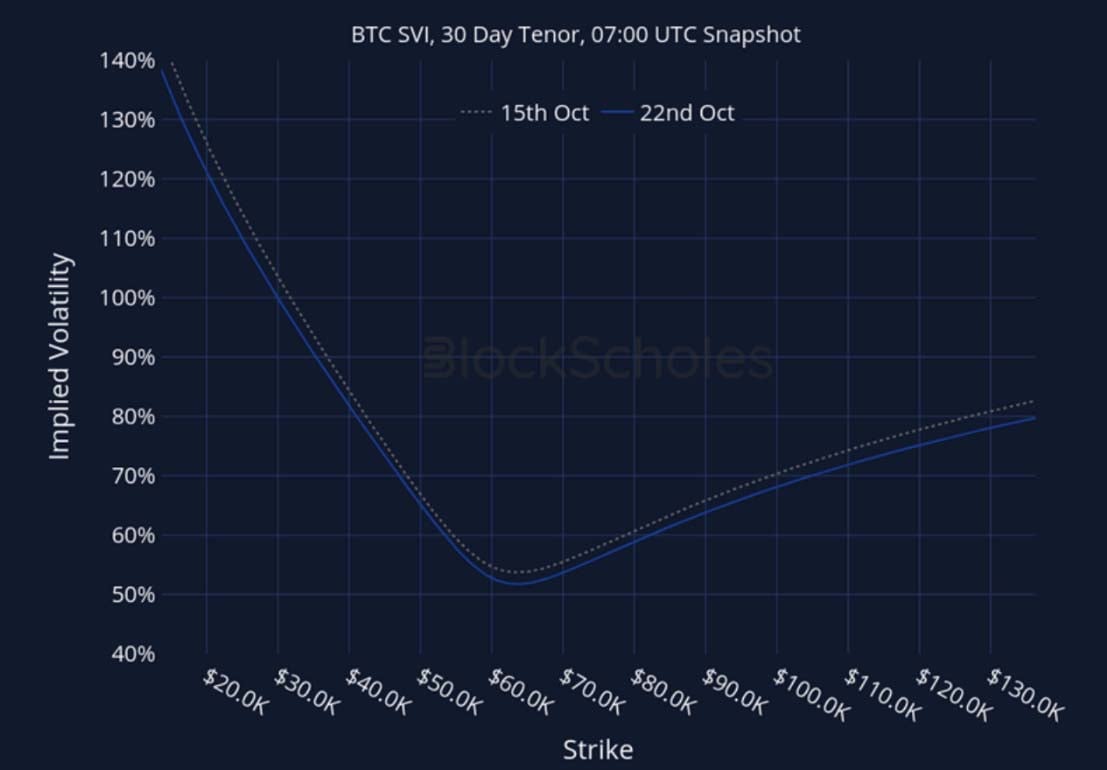

BTC SVI, 30D TENOR – 7:00 UTC Snapshot.

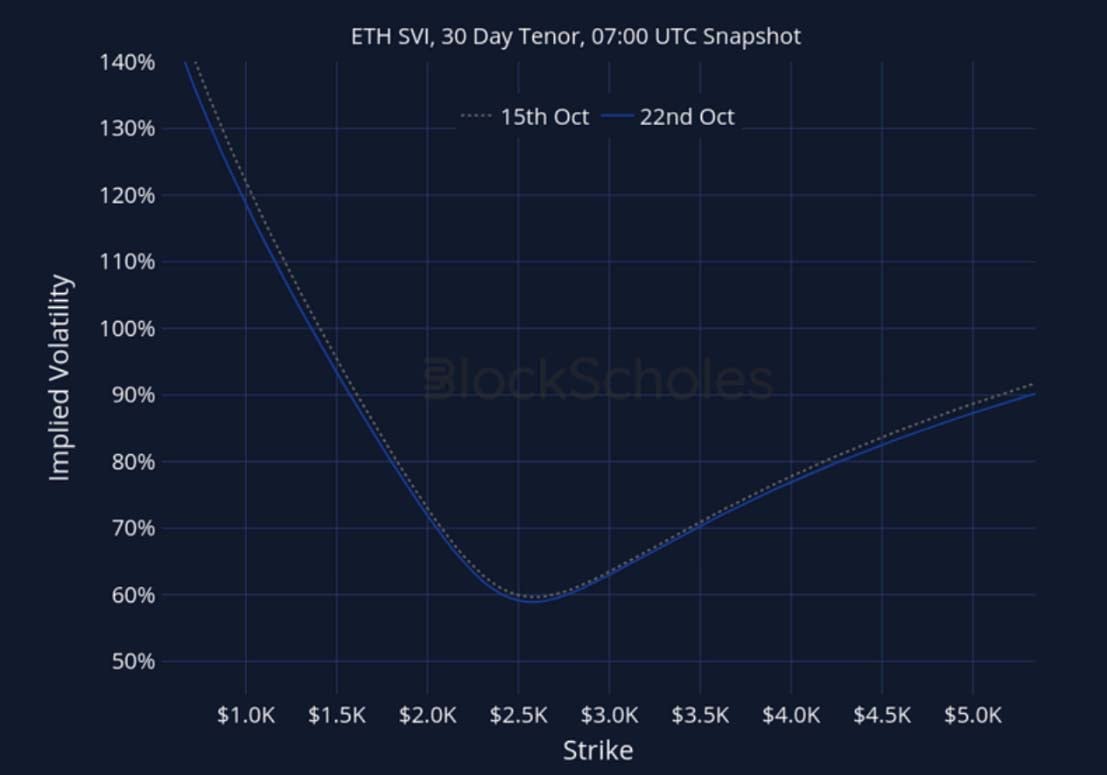

ETH SVI, 30D TENOR – 7:00 UTC Snapshot.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.