Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

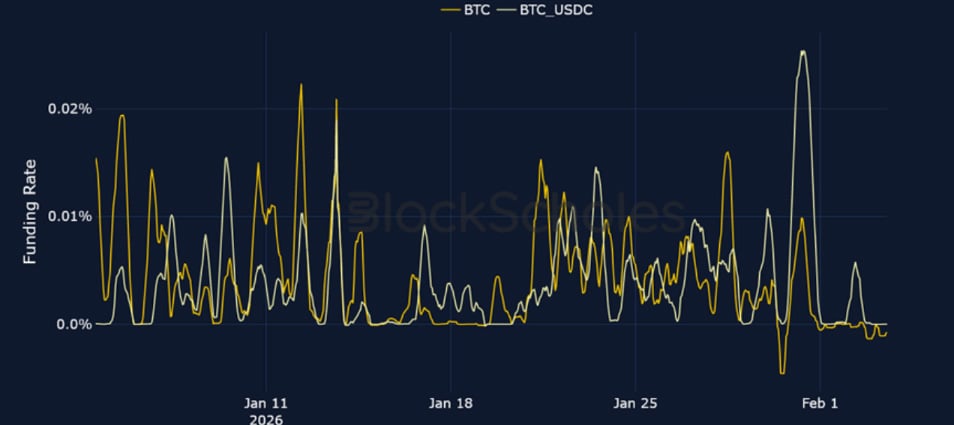

A major selloff in precious metals that saw silver prices plunge by their most in a single-day since 1980 spilled over into crypto markets over the weekend. That resulted in BTC revisiting $74K – a level it last traded at in the aftermath of the Liberation Day tariffs in April 2025 and nearly 40% below its October all-time high. The weekend selloff was the largest in crypto since October 10, 2025, seeing the most liquidations since that date. As such, the extreme bearish positioning across derivatives markets is perhaps unsurprising, with each measure of directional sentiment pointing towards further panic: short-dated ETH skew fell to its lowest since April 2025, funding rates on perpetual futures contracts fell below 0% for both BTC and ETH, and near-dated futures-implied yields also traded at a discount to spot.

Volatility expectations also surged higher following the drop in spot prices to multi-month lows – both BTC and ETH’s term structures of ATM implied volatility are currently inverted.

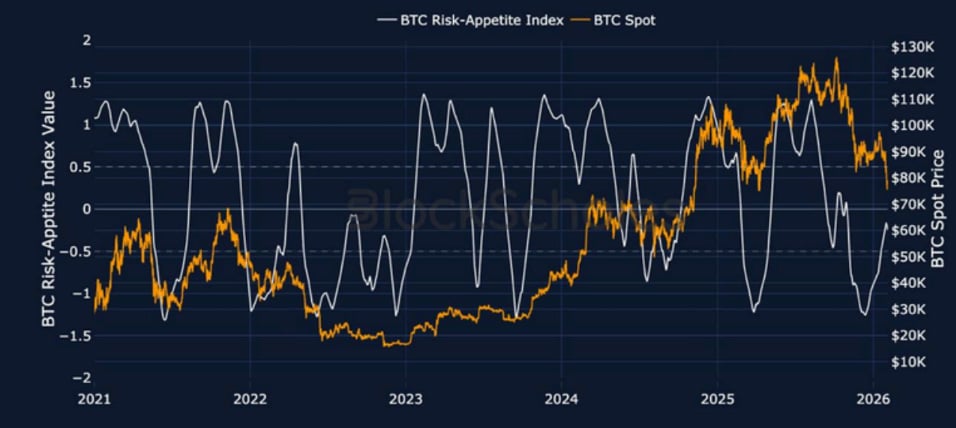

Block Scholes BTC Risk Appetite Index

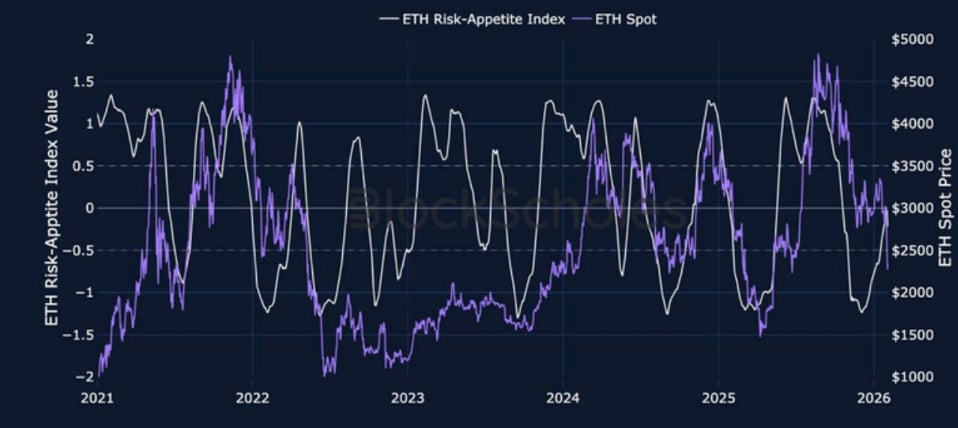

Block Scholes ETH Risk Appetite Index

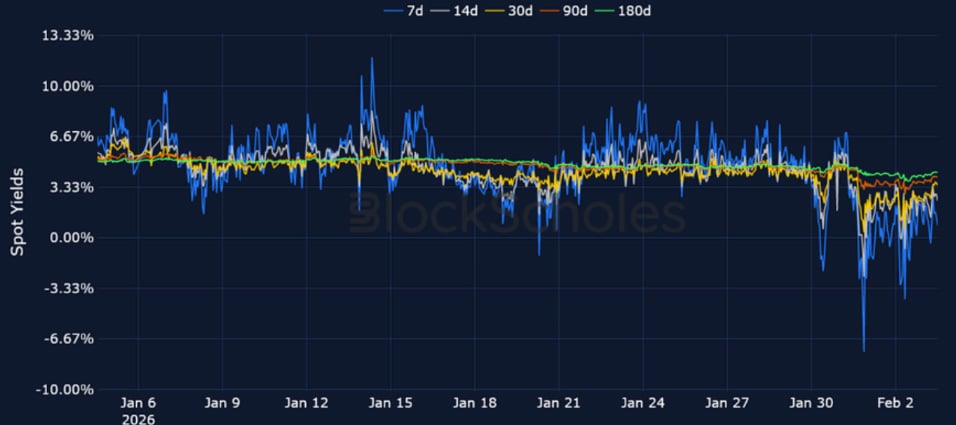

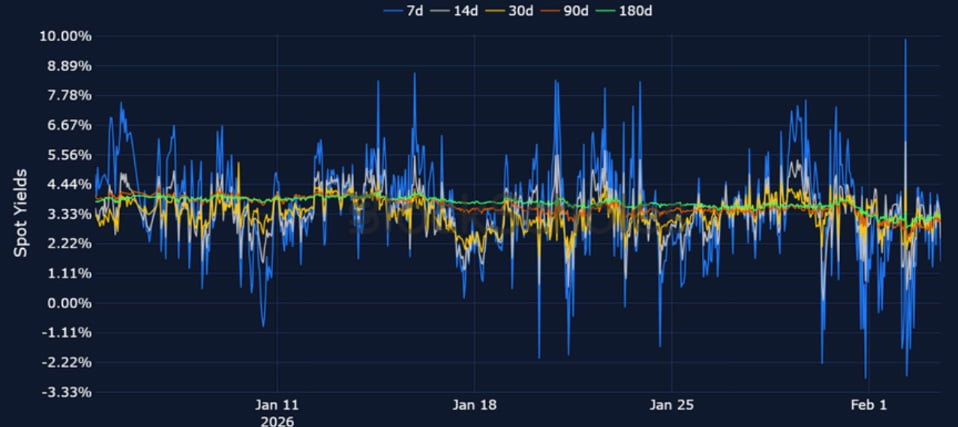

Futures Implied Yields

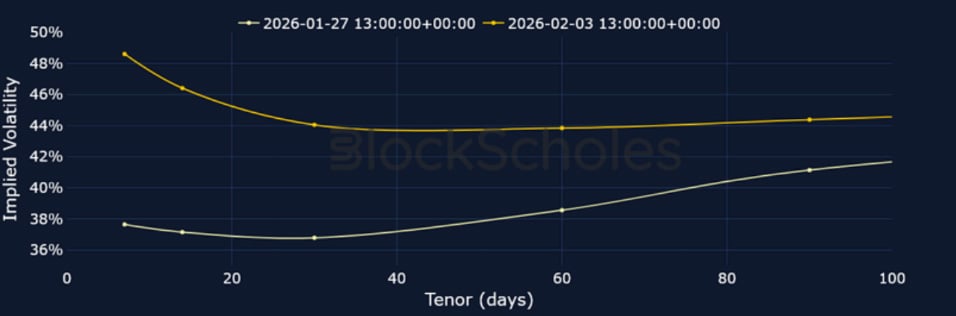

1-Month Tenor ATM Implied Volatility

Perpetual Swap Funding Rate

BTC FUNDING RATE – The selloff in precious metals spilled over into crypto risk sentiment, pushing BTC funding rates negative in a sign of extreme bearishness.

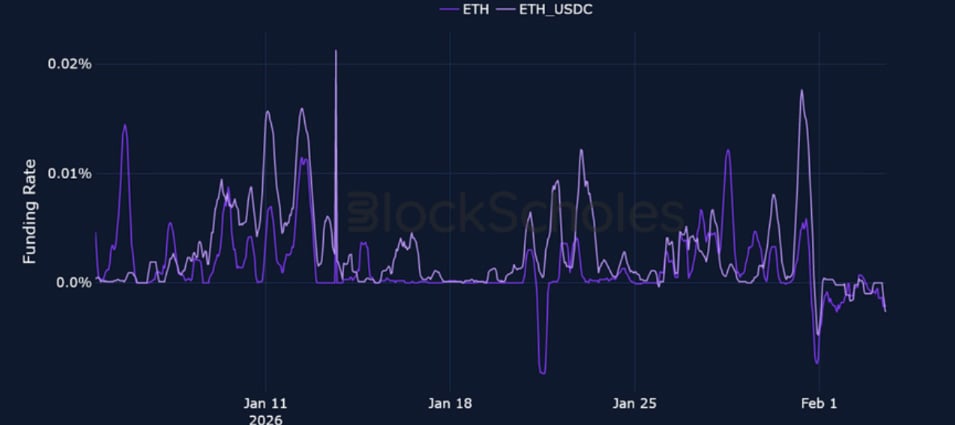

ETH FUNDING RATE – With ETH spot price now more than 50% below its ATH, short traders are willing to pay a premium betting on further price drops.

Futures Implied Yields

BTC Futures Implied Yields – Short-dated tenors turned negative for the first time this year, indicating futures prices trading at a discount to spot; another bearish signal in derivatives markets.

ETH Futures Implied Yields – Similar to BTC, positioning in ETH futures contracts flashed signs of bearish sentiment with near-term yields falling negative.

BTC Options

BTC SVI ATM IMPLIED VOLATILITY – Volatility expectations surged to their highest since November 2025, exceeding the levels reached on October 10th.

BTC 25-Delta Risk Reversal – A surge in the demand for put contracts has pushed short-dated skew to as low as -13%, indicating traders are not convinced that $74K marked the local floor.

ETH Options

ETH SVI ATM IMPLIED VOLATILITY – Short-dated ATM IV in ETH nearly doubled during the weekend selloff.

ETH 25-Delta Risk Reversal – After spending much of early January close to neutral levels, 7-day ETH skew fell to its lowest since Liberation Day in April 2025.

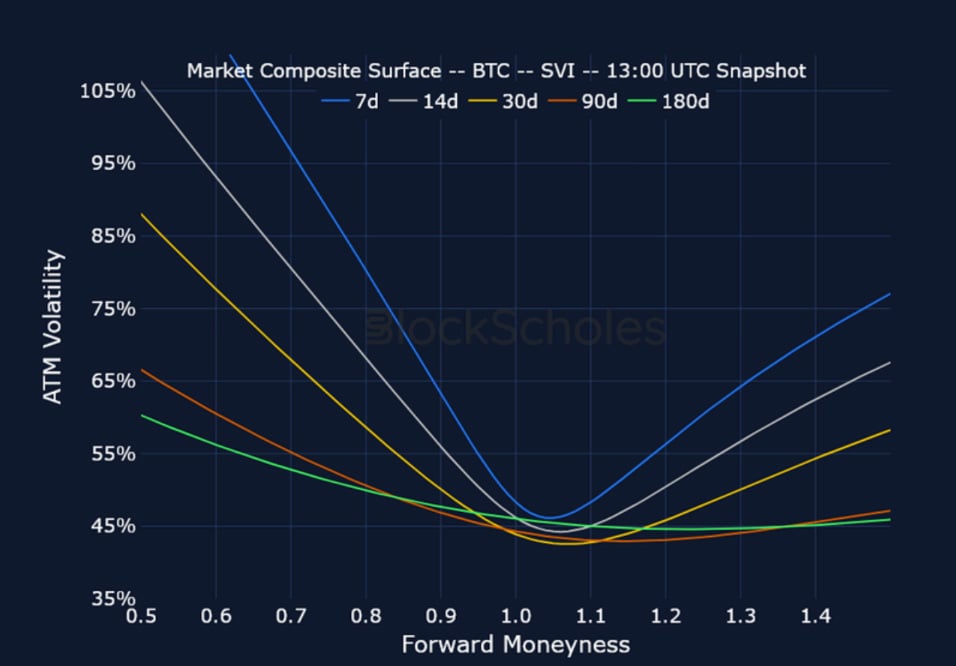

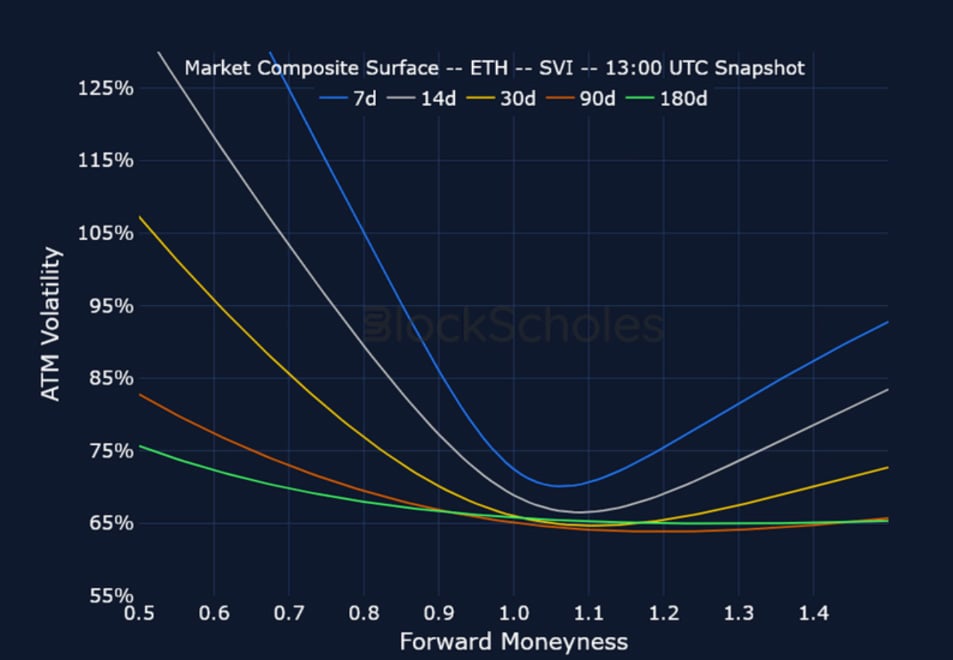

Market Composite Volatility Surface

CeFi COMPOSITE – BTC SVI – 9:00 UTC Snapshot.

CeFi COMPOSITE – ETH SVI – 9:00 UTC Snapshot.

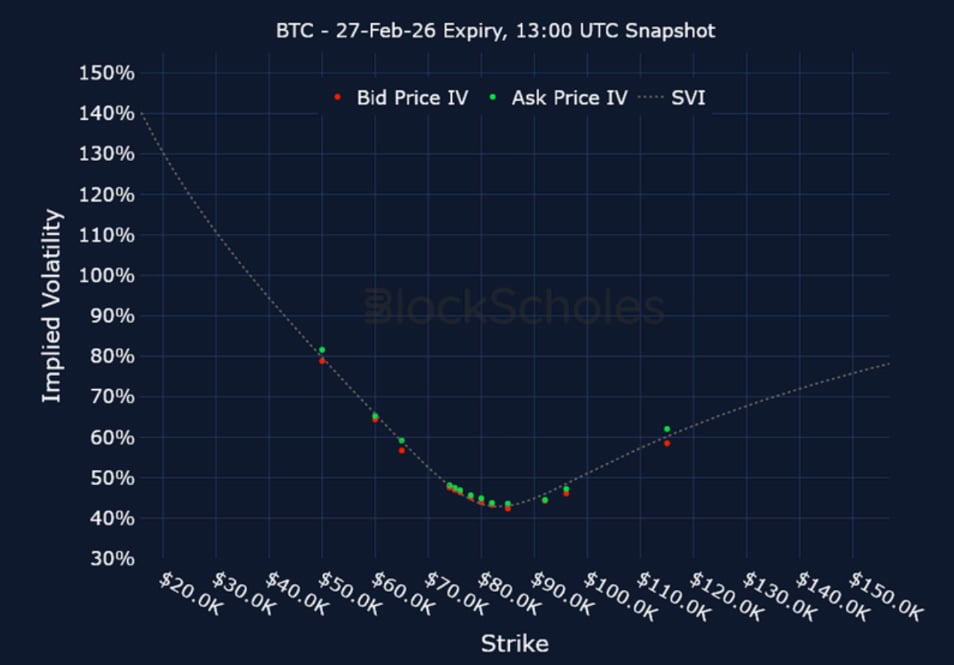

Listed Expiry Volatility Smiles

BTC 26-FEB EXPIRY – 9:00 UTC Snapshot.

ETH 26-FEB EXPIRY – 9:00 UTC Snapshot.

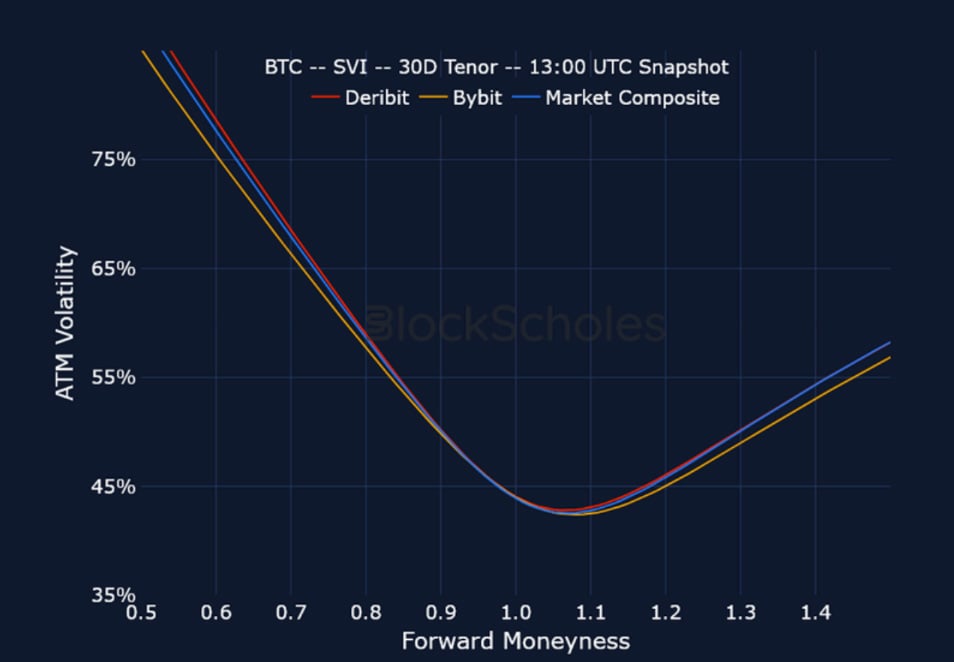

Cross-Exchange Volatility Smiles

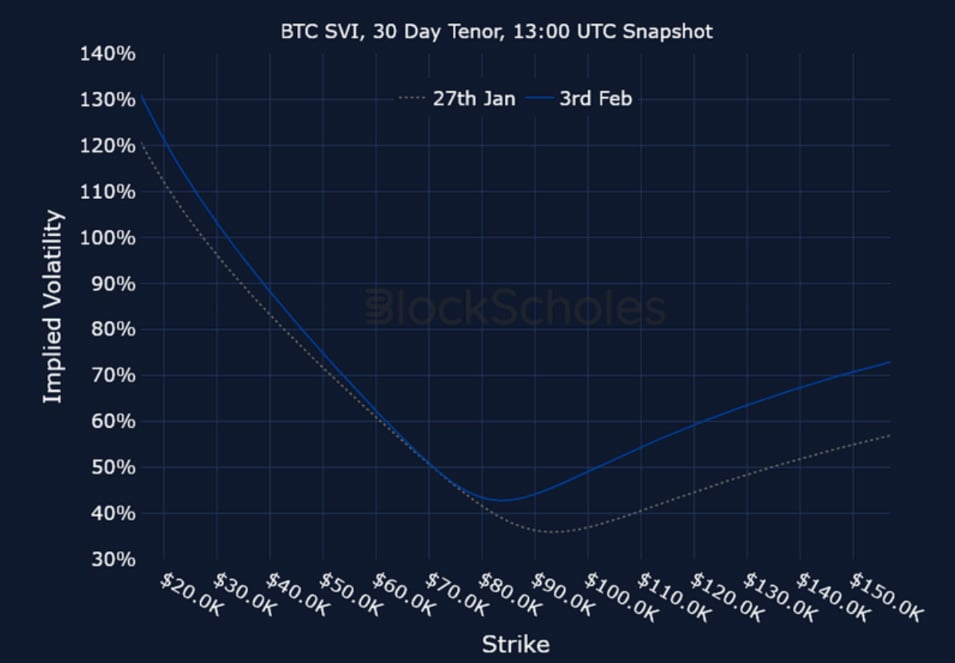

BTC SVI, 30D TENOR – 9:00 UTC Snapshot.

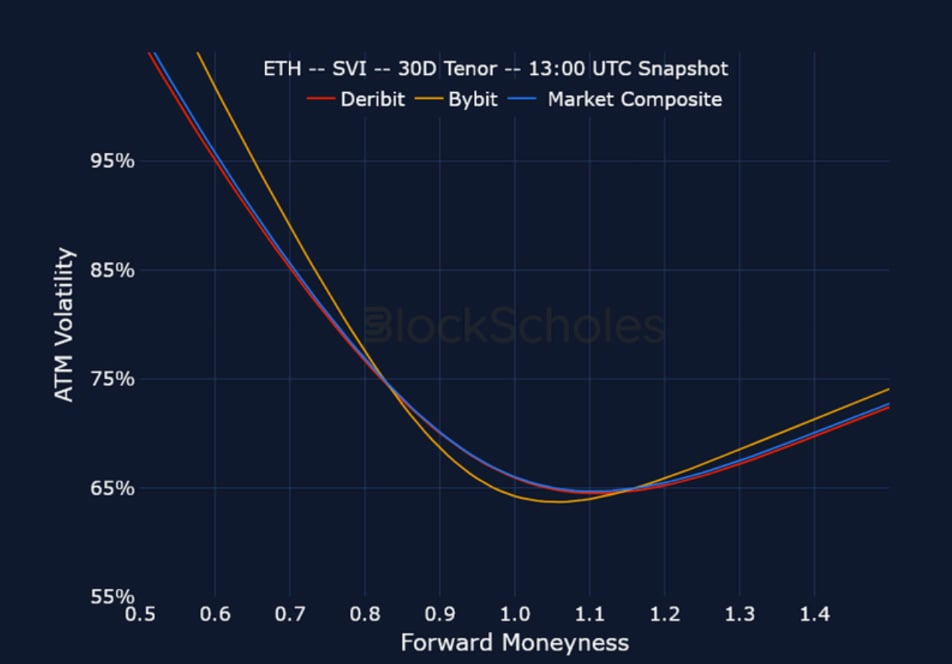

ETH SVI, 30D TENOR – 9:00 UTC Snapshot.

Constant Maturity Volatility Smiles

BTC SVI, 30D TENOR – 9:00 UTC Snapshot.

ETH SVI, 30D TENOR – 9:00 UTC Snapshot.

Disclaimer

This article reflects the personal views of its author, not Deribit or its affiliates. Deribit has neither reviewed nor endorsed its content.

Deribit does not offer investment advice or endorsements. The information herein is informational and shouldn’t be seen as financial advice. Always do your own research and consult professionals before investing.

Financial investments carry risks, including capital loss. Neither Deribit nor the article’s author assumes liability for decisions based on this content.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.