Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

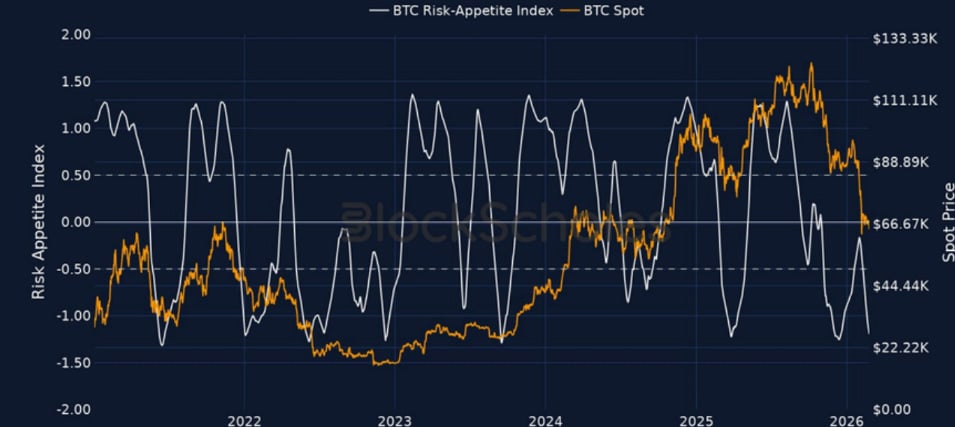

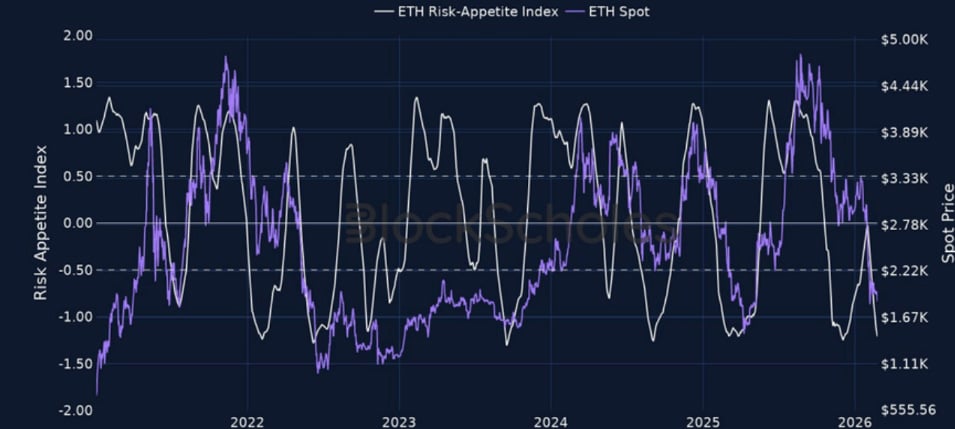

Risk appetite continues to deteriorate with BTC briefly falling to $62K amidst a broader risk-off sentiment across asset classes following President Trump’s announcement to raise global tariffs to 15%. Our in-house Risk Appetite Indexes for both BTC and ETH are now approaching the 2025 lows they bounced off from as BTC is now on track for its fifth monthly loss.

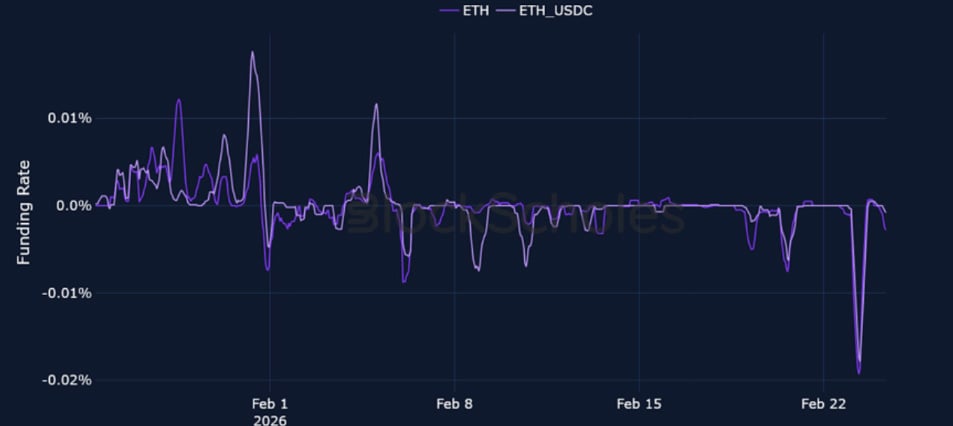

All three measures of derivative market sentiment reflect the current bearishness. ETH perpetual futures funding rates fell to their most negative since the 10/10 liquidation, volatility smiles have sharply tilted even further towards puts as the demand for downside hedging renews, and futures- implied yields for short-dated futures contracts remains below spot price.

Block Scholes BTC Risk Appetite Index

Block Scholes ETH Risk Appetite Index

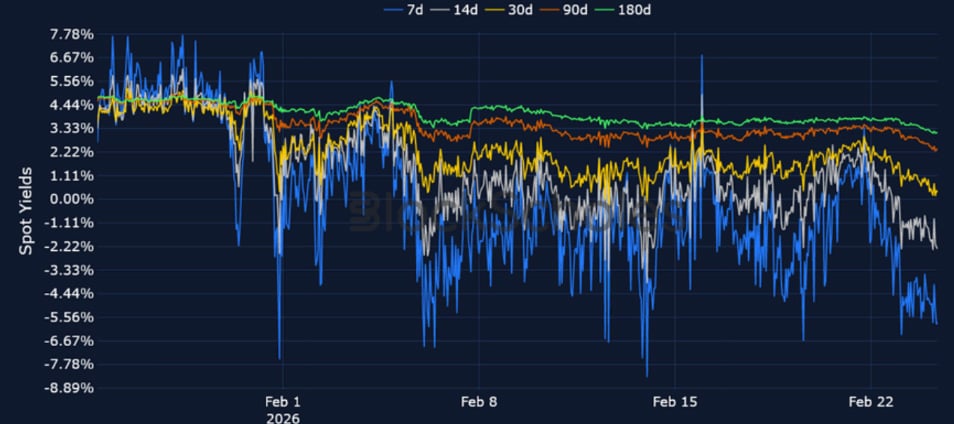

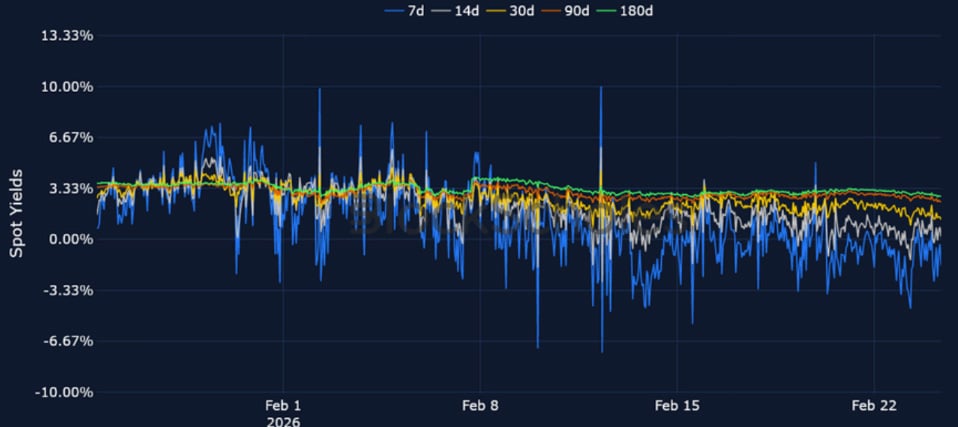

Futures Implied Yields

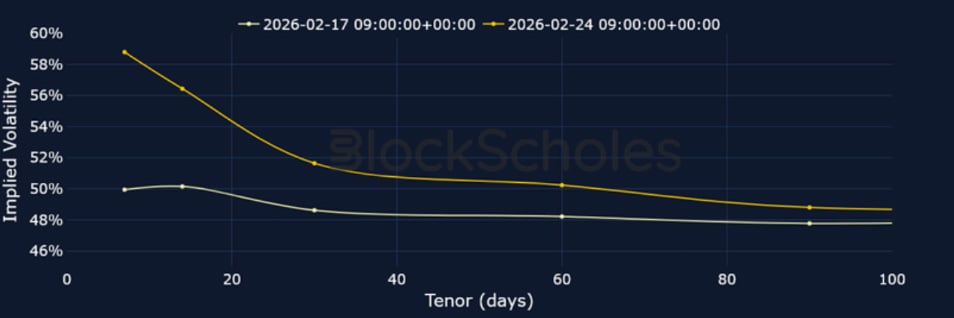

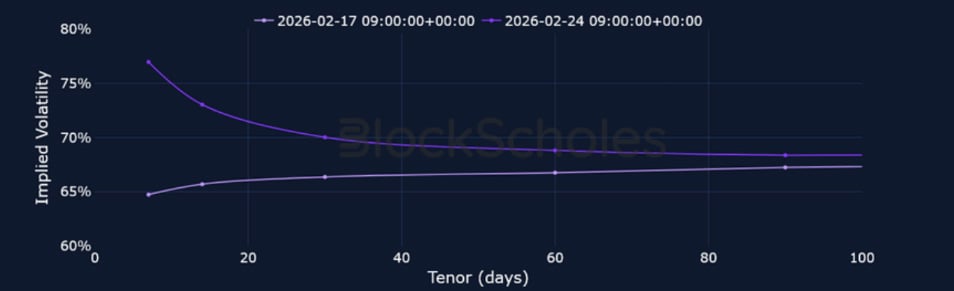

1-Month Tenor ATM Implied Volatility

Perpetual Swap Funding Rate

BTC FUNDING RATE – After a period of sideways funding rates and spot price consolidation between $65K and $70K, funding fell to a two-week low as BTC spot price briefly traded at $62K.

ETH FUNDING RATE – ETH funding rates fell to their most negative since the 10/10 liquidation yesterday as short perp traders showed a strong willingness to maintain their positions.

Futures Implied Yields

BTC Futures Implied Yields – Sentiment in futures contracts mirrors the same bearishness currently priced in perp funding rates and volatility smile skews, as short-dated futures now trade at a sharp discount to spot price.

ETH Futures Implied Yields – 7-day ETH futures implied yields also turned negative yesterday, though have shown some signs of recovery unlike equivalently dated BTC futures contracts.

BTC Options

BTC SVI ATM IMPLIED VOLATILITY – BTC’s vol term structure has mildly inverted after nearly three weeks of sideways trading.

BTC 25-Delta Risk Reversal – With BTC on track for its worst month since June 2022, traders are once more showing increased demand for puts protecting against further downside moves in spot price. As such, the 7-day put-call skew has plunged from -6% to -17% over the last 24 hours.

ETH Options

ETH SVI ATM IMPLIED VOLATILITY – 7-day ETH ATM vol has jumped up from 60% to 77%, in line with a spike higher in realised vol.

ETH 25-Delta Risk Reversal – ETH volatility smiles also show traders hedging against further downward moves in spot prices, with short-dated skew now trading at -16%.

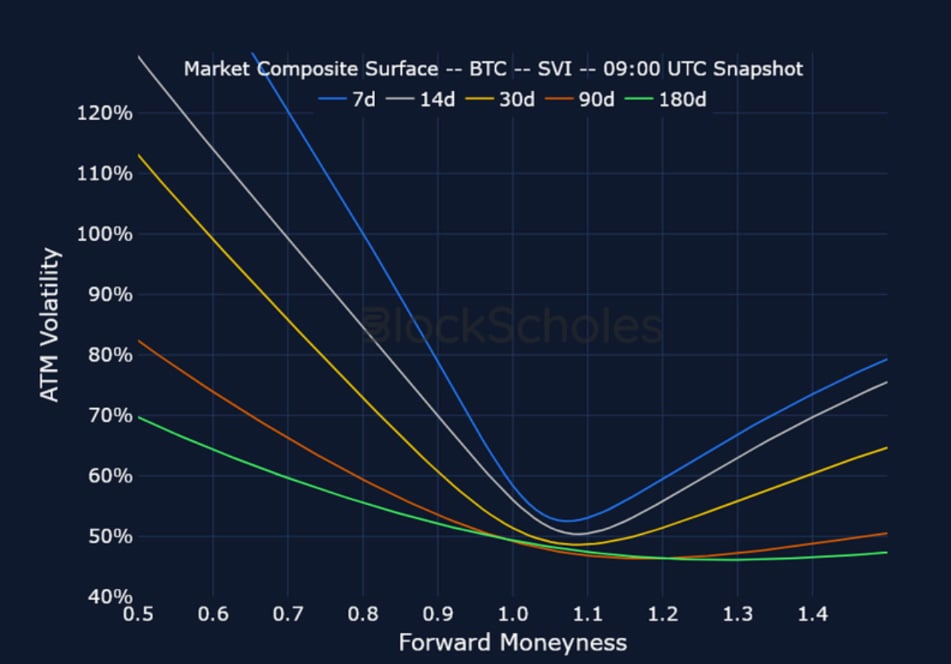

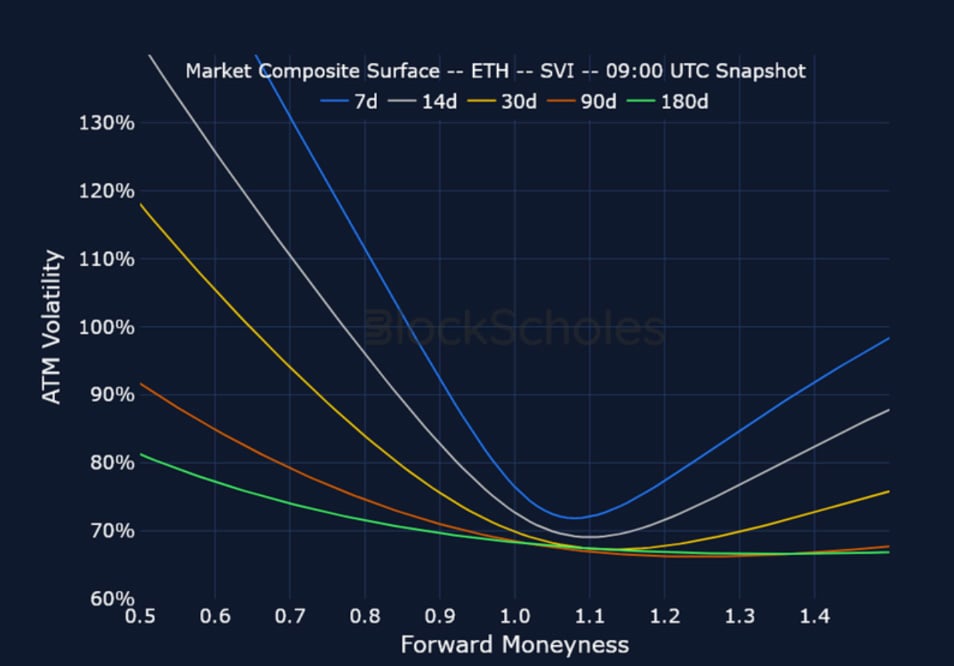

Market Composite Volatility Surface

CeFi COMPOSITE – BTC SVI – 9:00 UTC Snapshot.

CeFi COMPOSITE – ETH SVI – 9:00 UTC Snapshot.

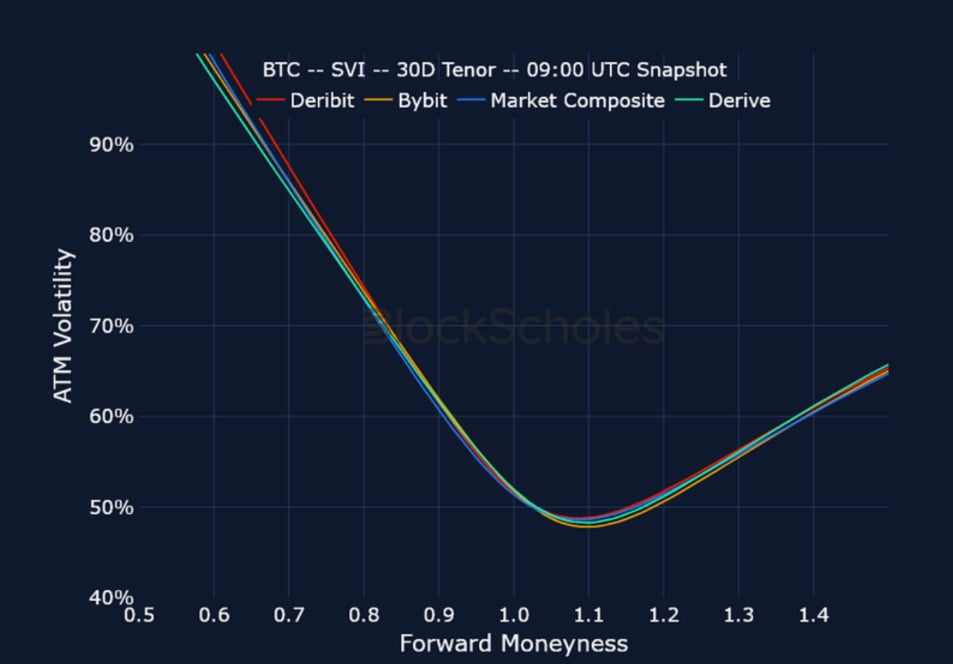

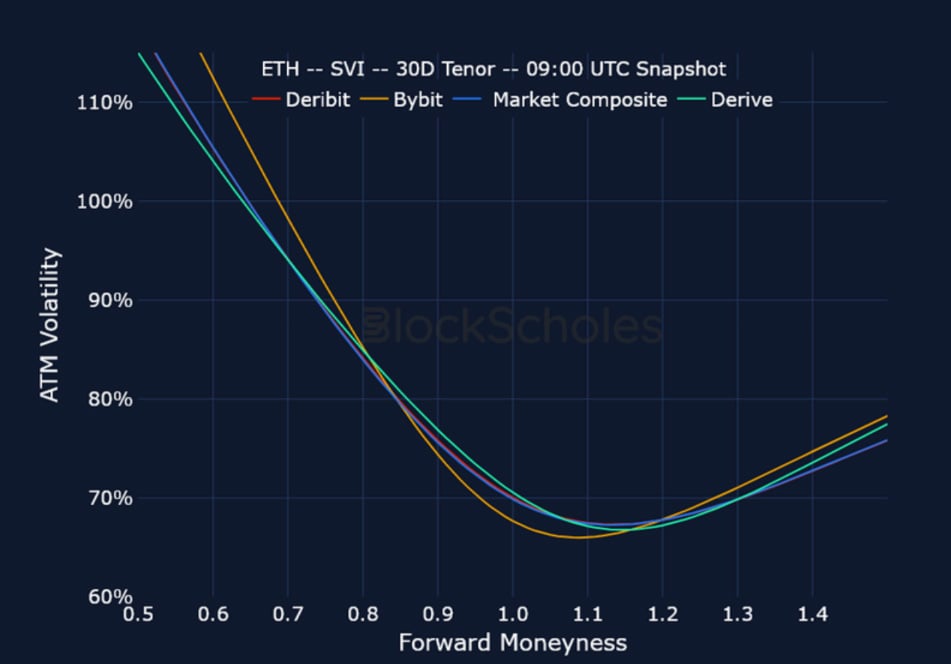

Cross-Exchange Volatility Smiles

BTC SVI, 30D TENOR – 9:00 UTC Snapshot.

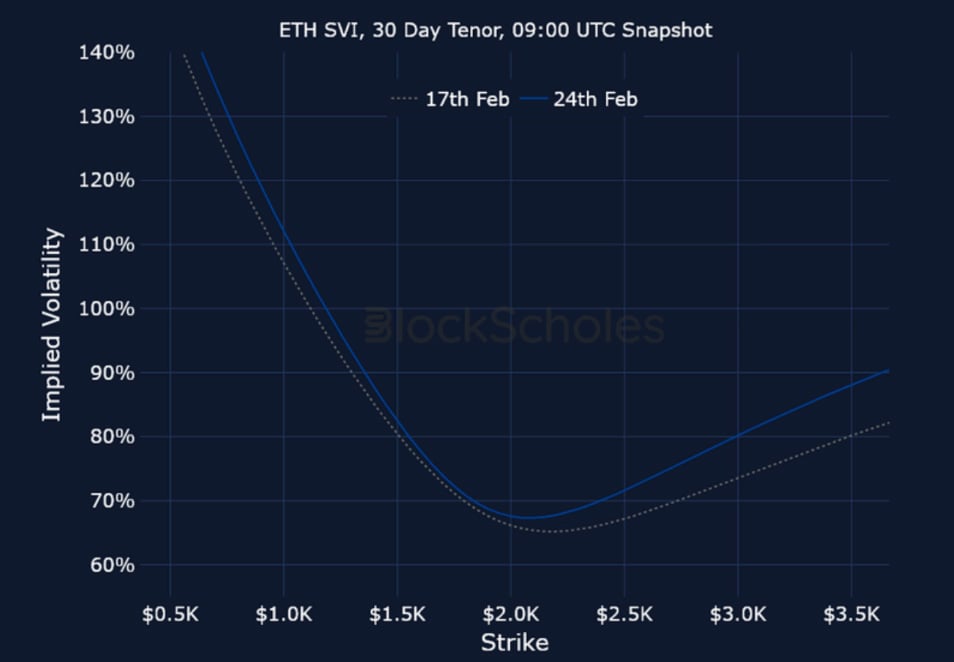

ETH SVI, 30D TENOR – 9:00 UTC Snapshot.

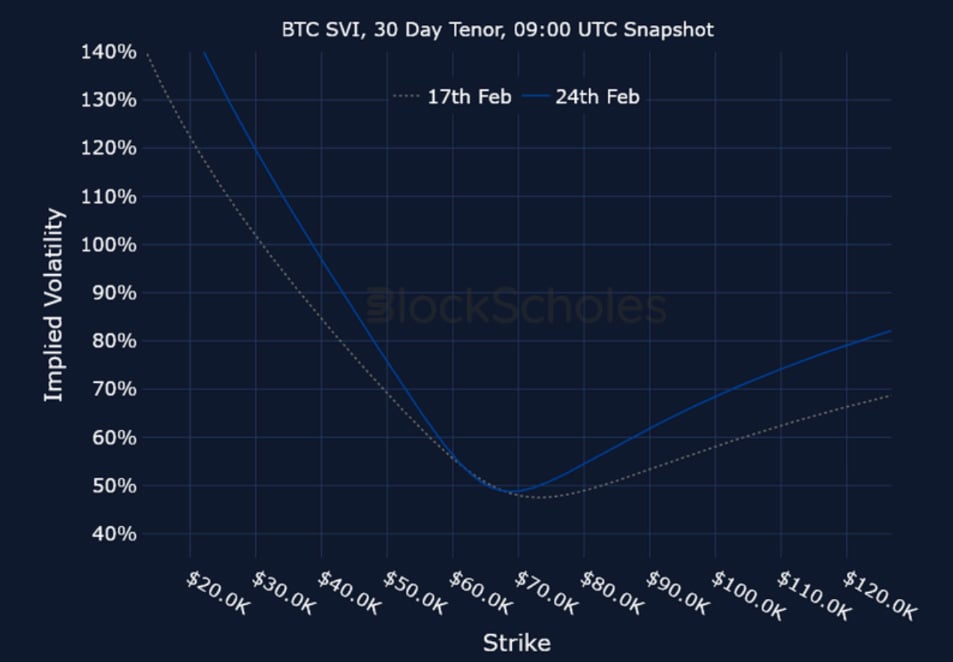

Constant Maturity Volatility Smiles

BTC SVI, 30D TENOR – 9:00 UTC Snapshot.

ETH SVI, 30D TENOR – 9:00 UTC Snapshot.

Disclaimer

This article reflects the personal views of its author, not Deribit or its affiliates. Deribit has neither reviewed nor endorsed its content.

Deribit does not offer investment advice or endorsements. The information herein is informational and shouldn’t be seen as financial advice. Always do your own research and consult professionals before investing.

Financial investments carry risks, including capital loss. Neither Deribit nor the article’s author assumes liability for decisions based on this content.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.