In this week’s edition of Option Flows, Tony Stewart is commenting on the recent market movements.

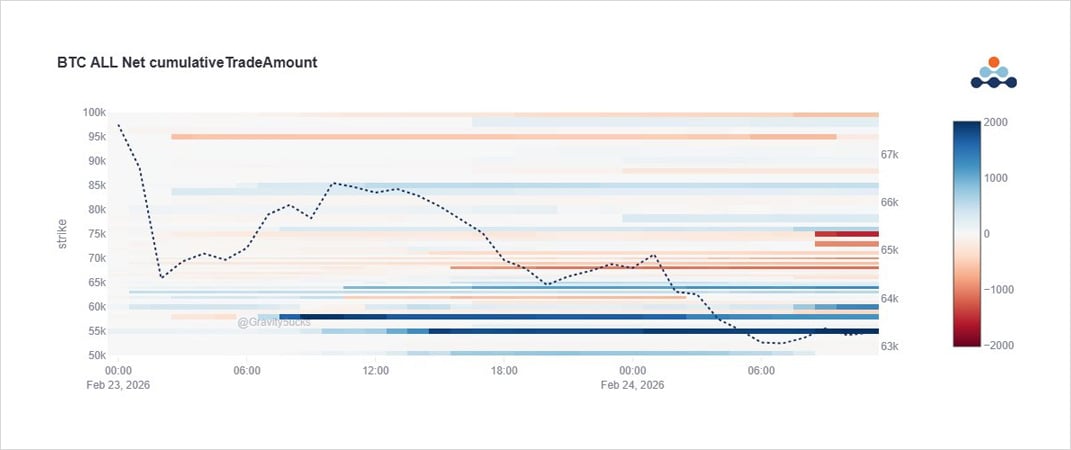

In a continuous downtrend in the existing range, it’s not a surprise to see ongoing downside plays (protection and bearish) on BTC.

How these are initiated determines the degree of likely returns.

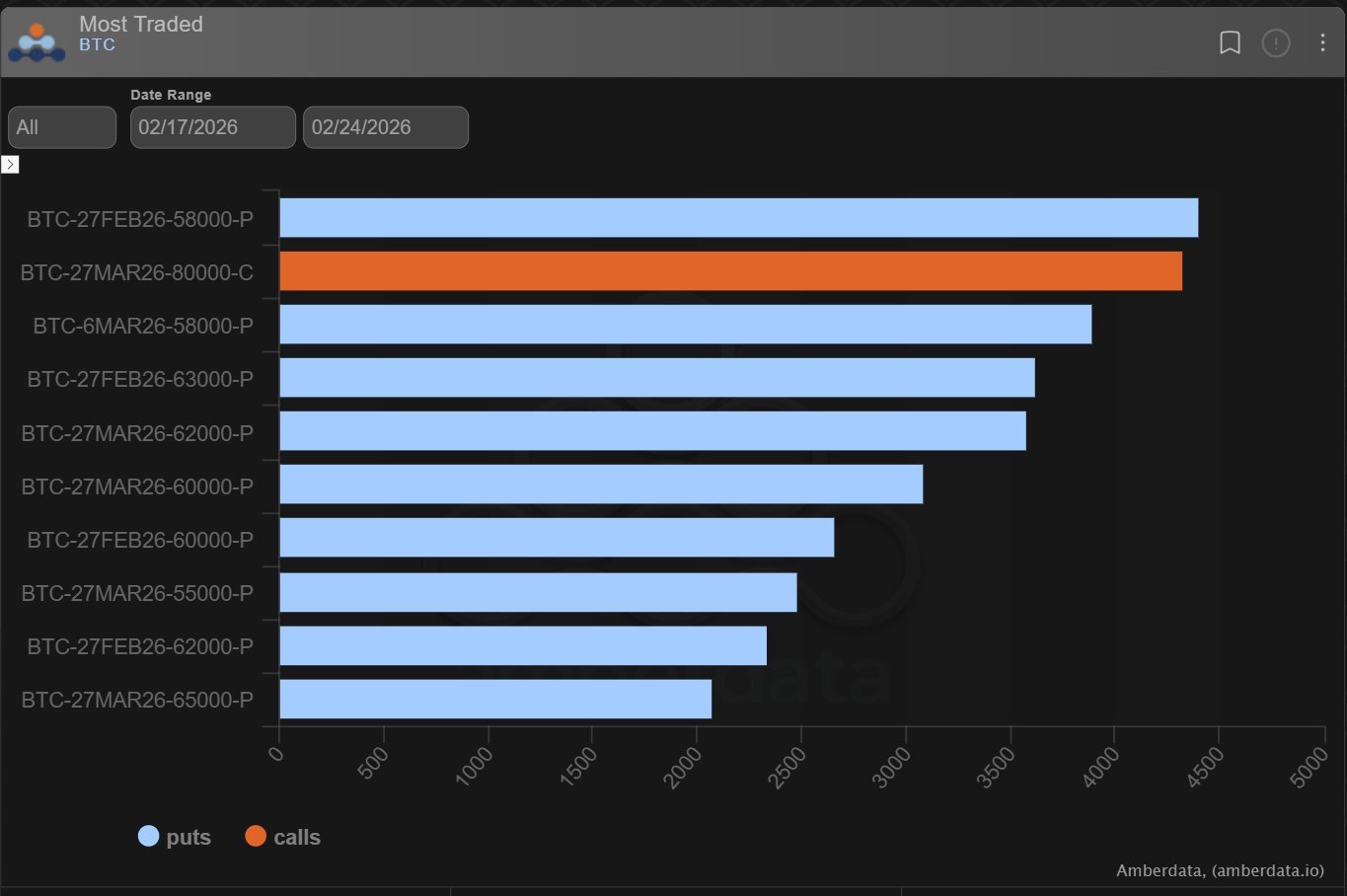

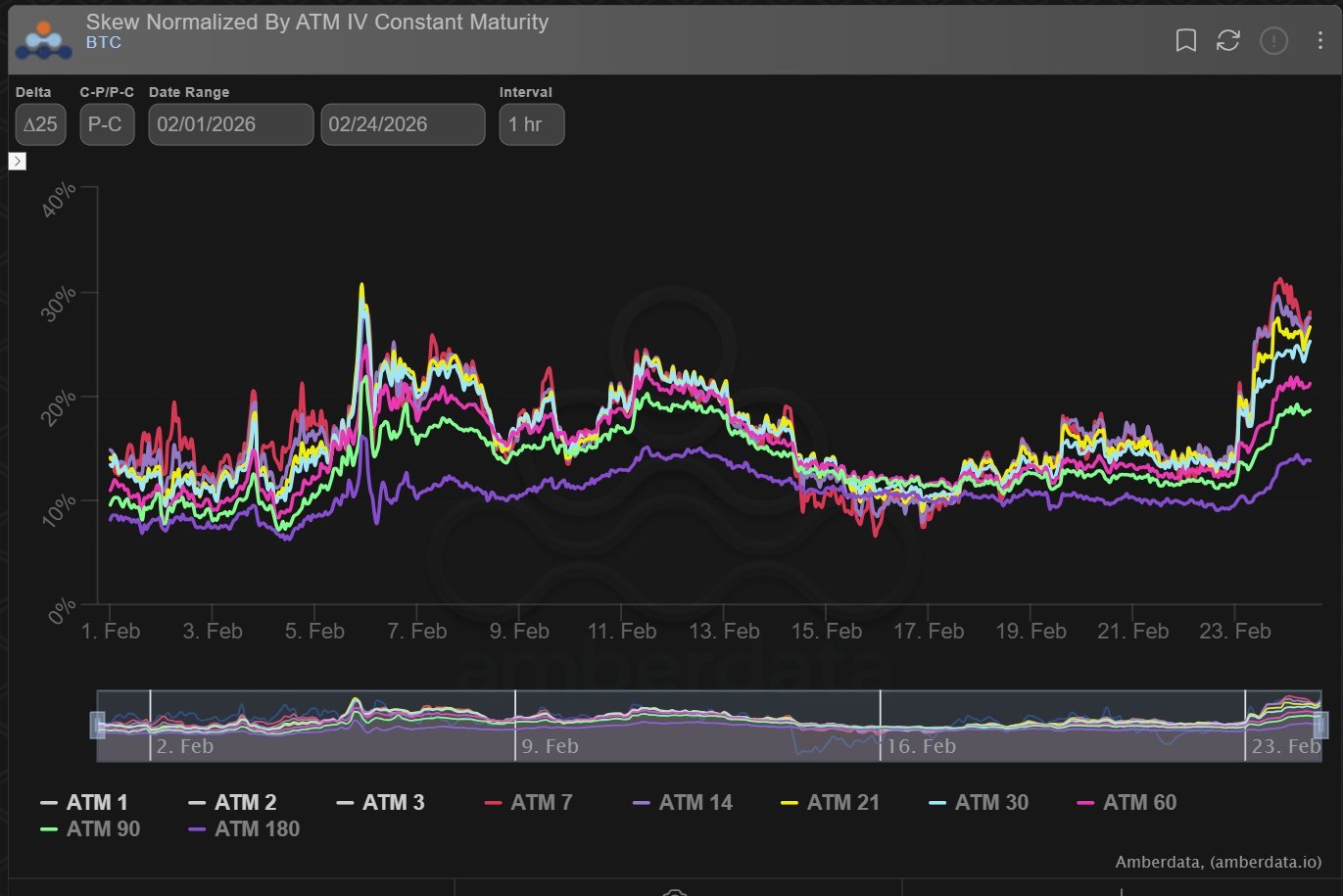

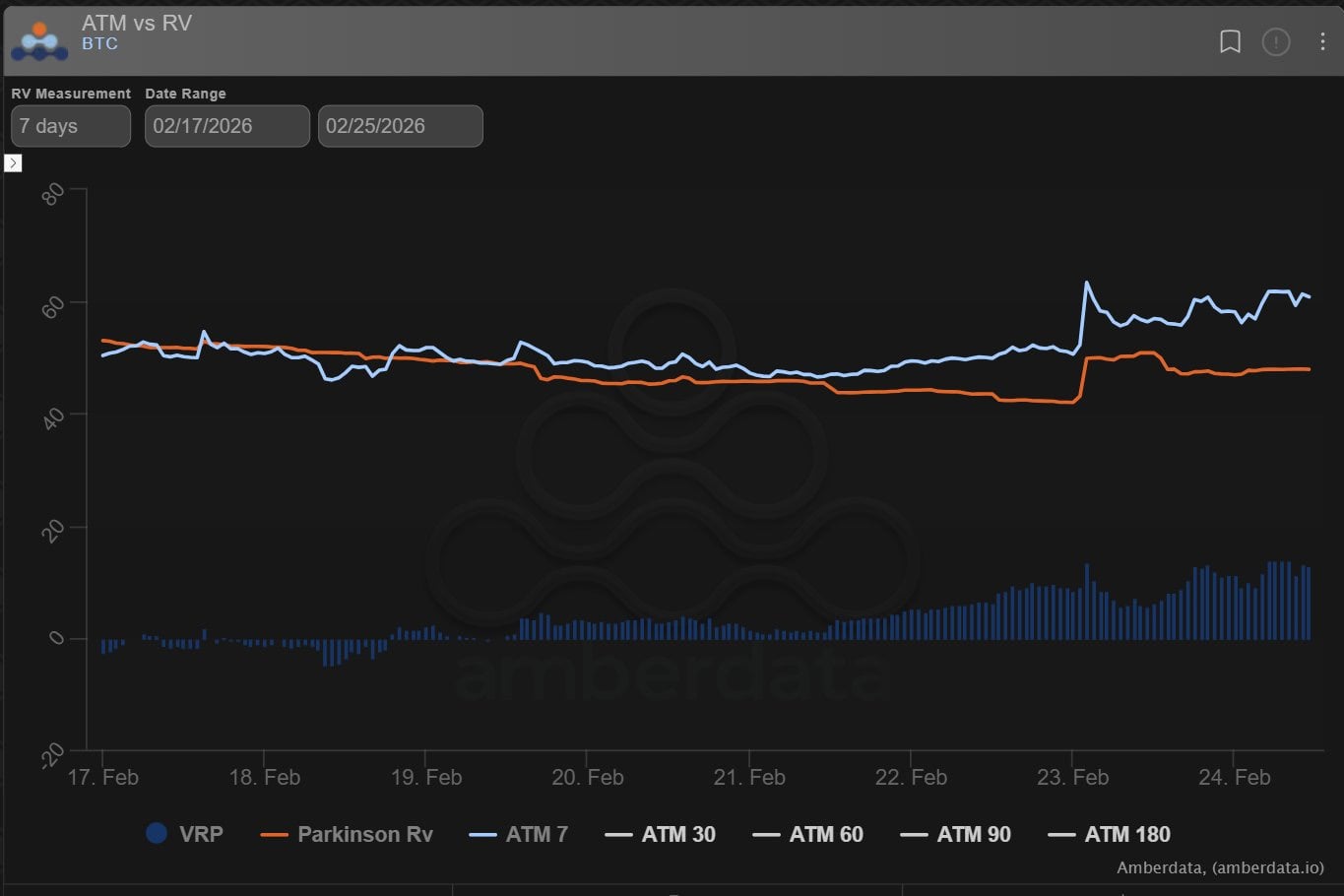

Put skew is back to Feb5th levels, IV>RV. 58k Puts in demand, Put spreads, +RRs.

Over the last week the data could not be clearer.

And yesterday saw the latest with an addition of Mar6 58k Puts, $200m notional bought, $2m premium.

So much demand has pushed Put Skew to Feb5 levels of extreme elevation, without that day’s sharp spot move to blame.

The level of fear protection and/or pure bearish views is also manifested by the levels of Implied Vols at >10% premium to Realized Vols on this 7day measure.

And so funds are using Put spreads and RiskReversals to attempt to mitigate their primary Put Strike level via either selling lower down extreme level Puts, or upside Calls (even at the discount they trade).

This extends the duration of success and returns over outright Puts.

See original post on X here.

Disclaimer

This article reflects the personal views of its author, not Deribit or its affiliates. Deribit has neither reviewed nor endorsed its content.

Deribit does not offer investment advice or endorsements. The information herein is informational and shouldn’t be seen as financial advice. Always do your own research and consult professionals before investing.

Financial investments carry risks, including capital loss. Neither Deribit nor the article’s author assumes liability for decisions based on this content.

AUTHOR(S)

ex-MS Head of Trading desk /BTC Vol. Prop trading /Option Market forensics/ Alter Ego account Digital Asset arena. Tweets are my opinion, not financial advice.