Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

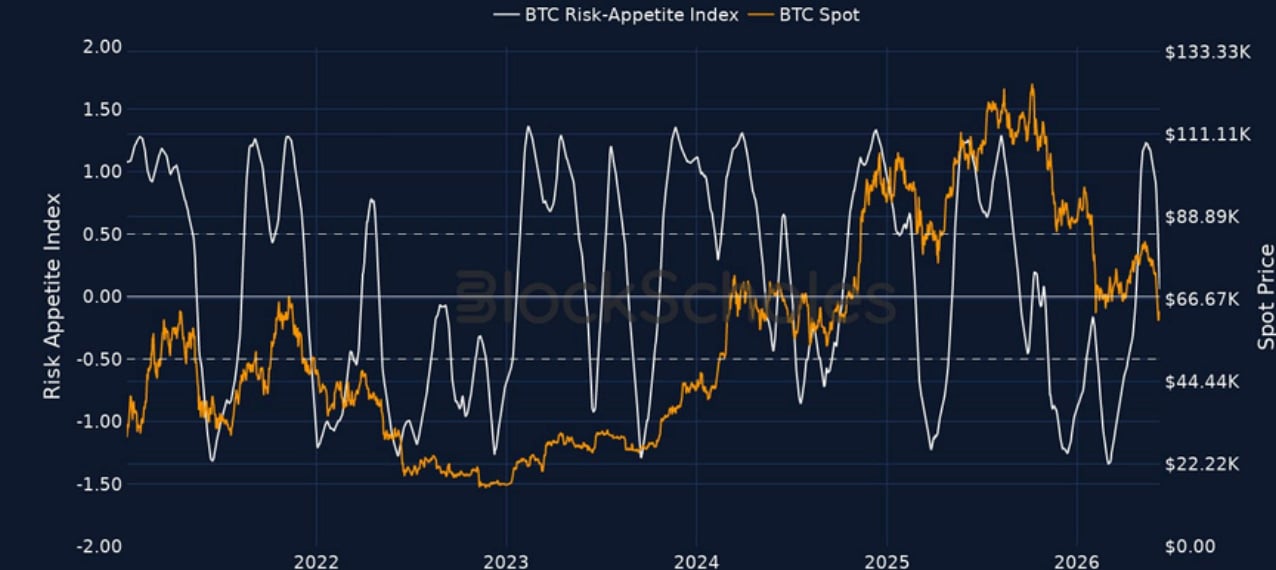

A near-20% plunge in BTC’s spot price last week has been reflected in a significant drop below 0.05 in our Block Scholes Risk Appetite Index. That selloff coincided with both the longest outflow streak from spot Bitcoin ETFs since launch (which after a brief pause has renewed), as well as Strategy Inc. (the largest BTC digital asset treasury) disclosing a 32 BTC sale. Since then, spot price has consolidated above $60K while Strategy announced a $103.1M BTC purchase of 1,550 bitcoins.

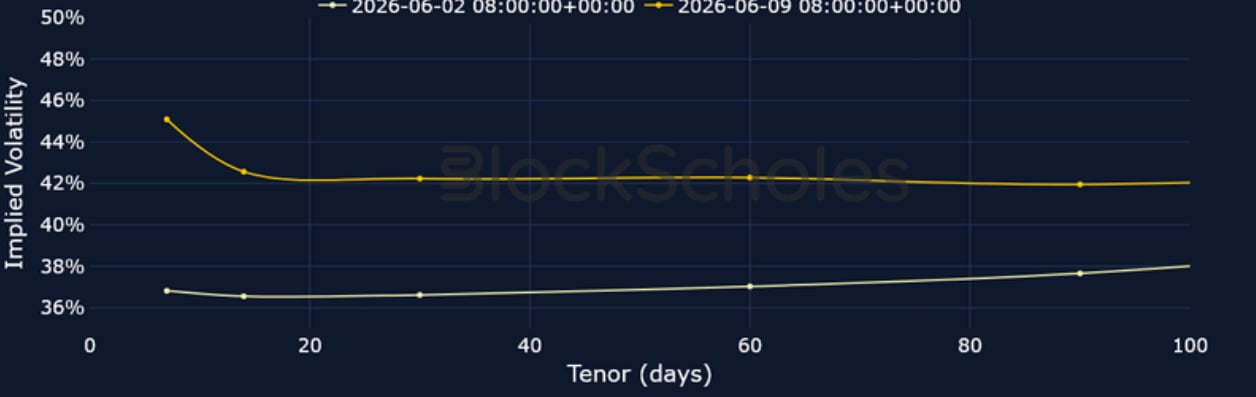

Despite the selloff easing, derivatives market positioning remains highly defensive – funding rates in ETH have traded negatively since June 5, 2026, a strong indication of the bearish bias in perp traders. Additionally, while ATM implied volatility has fallen ~20 percentage points for short-dated tenors for both BTC and ETH, term structures for both show a mild inversion. Volatility smiles also maintain a strong skew towards put options.

Block Scholes BTC Risk Appetite Index

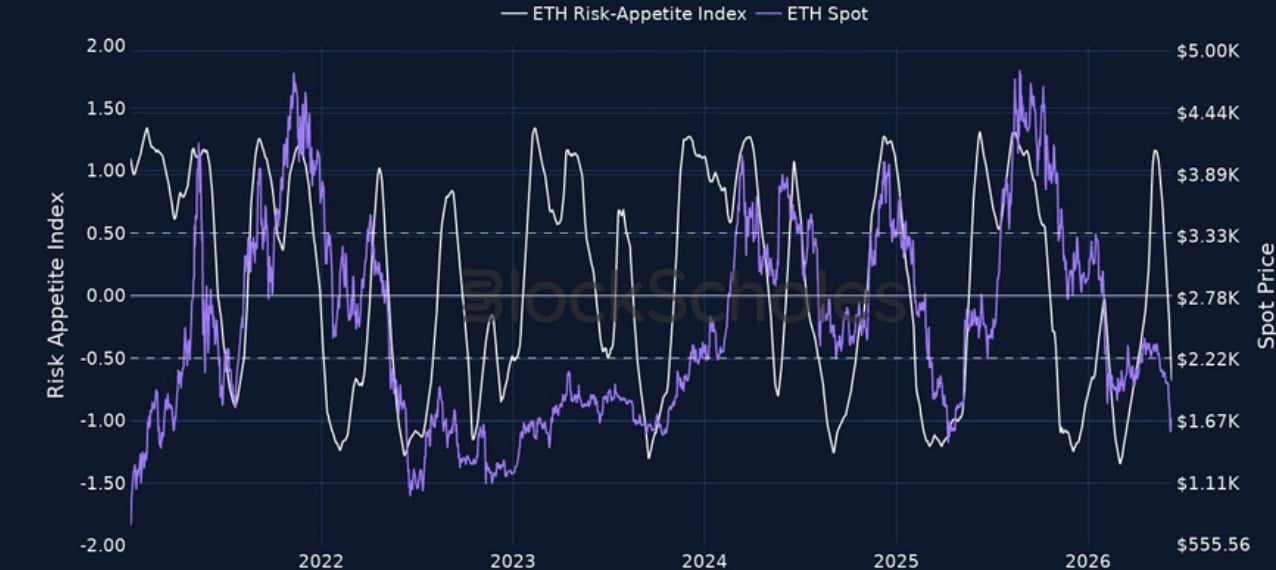

Block Scholes ETH Risk Appetite Index

1-Month Tenor ATM Implied Volatility

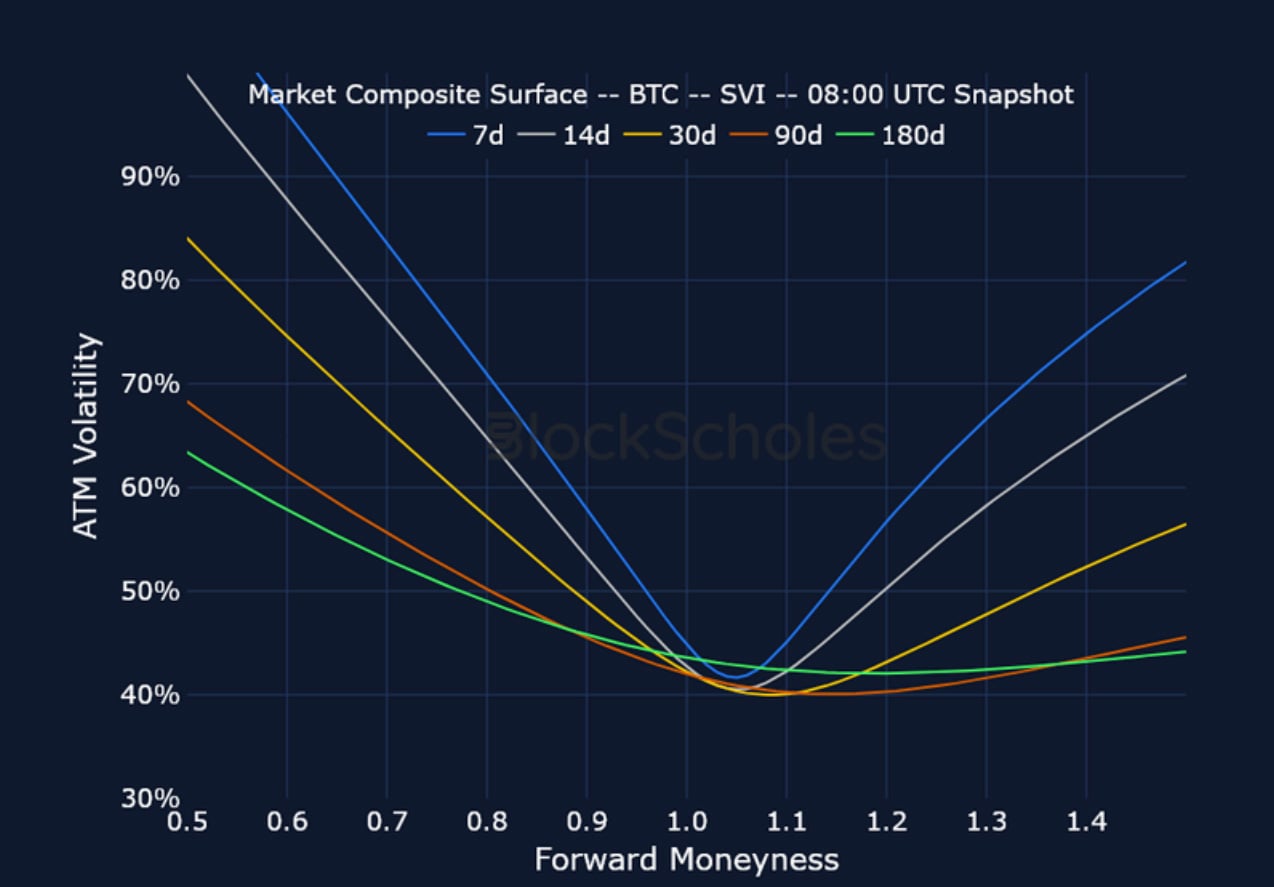

BTC Options

BTC SVI ATM IMPLIED VOLATILITY – Front-end volatility has dropped 20 percentage points as traders reduce expectations of larger-sized moves ahead.

ETH Options

ETH SVI ATM IMPLIED VOLATILITY – ETH’s term structure remains mildly inverted, with 7-day IV selling off by a similar amount to 7-day BTC IV.

BTC and ETH Skew

BTC 25-Delta Risk Reversal – The persistent put-premium that has characterised most of this year remains, with short-dated skew currently trading just shy of -9%. Still, that’s a significant improvement from the deeper -19% skew seen only five days ago, when spot price crashed below $60K.

ETH 25-Delta Risk Reversal – Similar to what we see in BTC options, ETH traders also remain hedged against further expectations for a selloff in spot price. ETH spot is currently down 66% from its record August 2025 high.

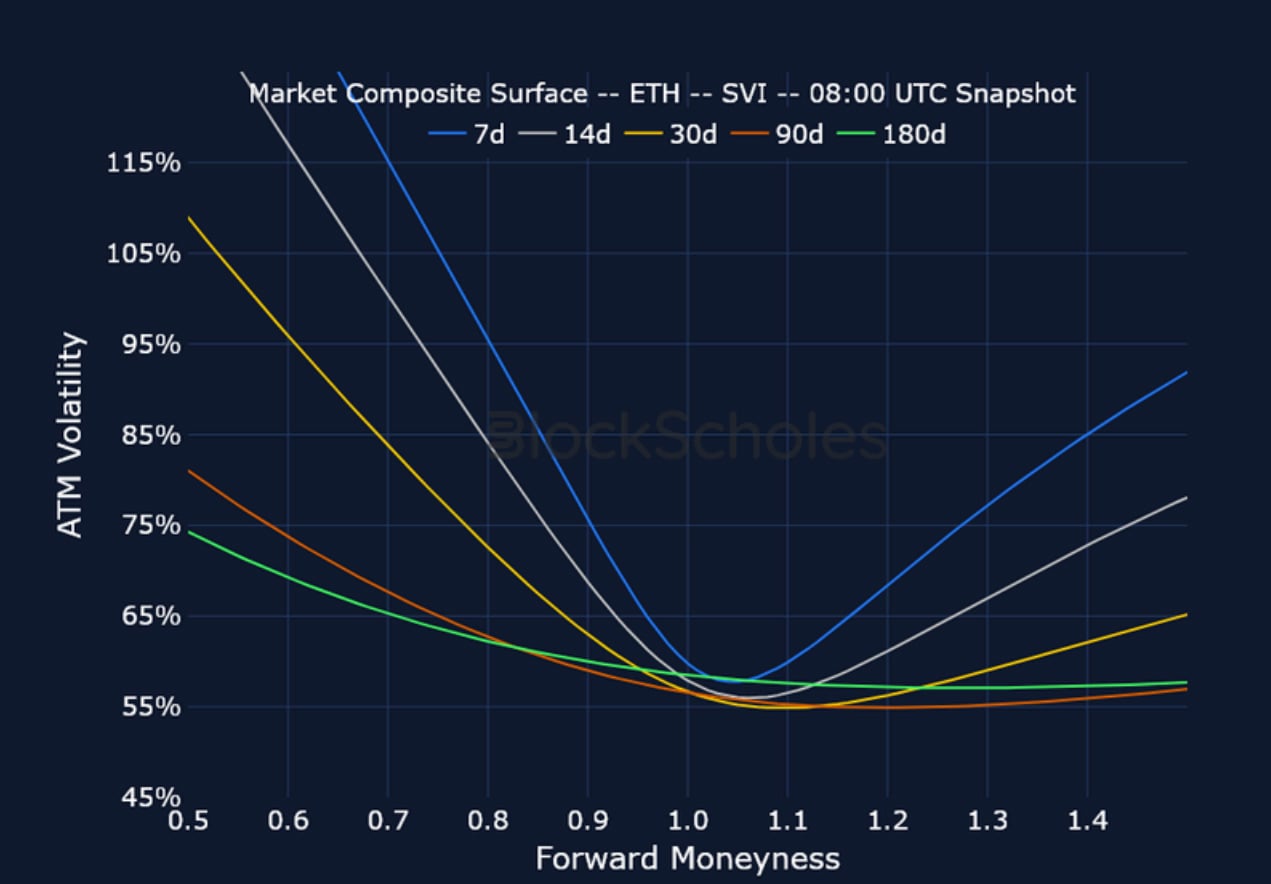

Market Composite Volatility Surface

BTC SVI – 8:00 UTC Snapshot.

ETH SVI – 8:00 UTC Snapshot.

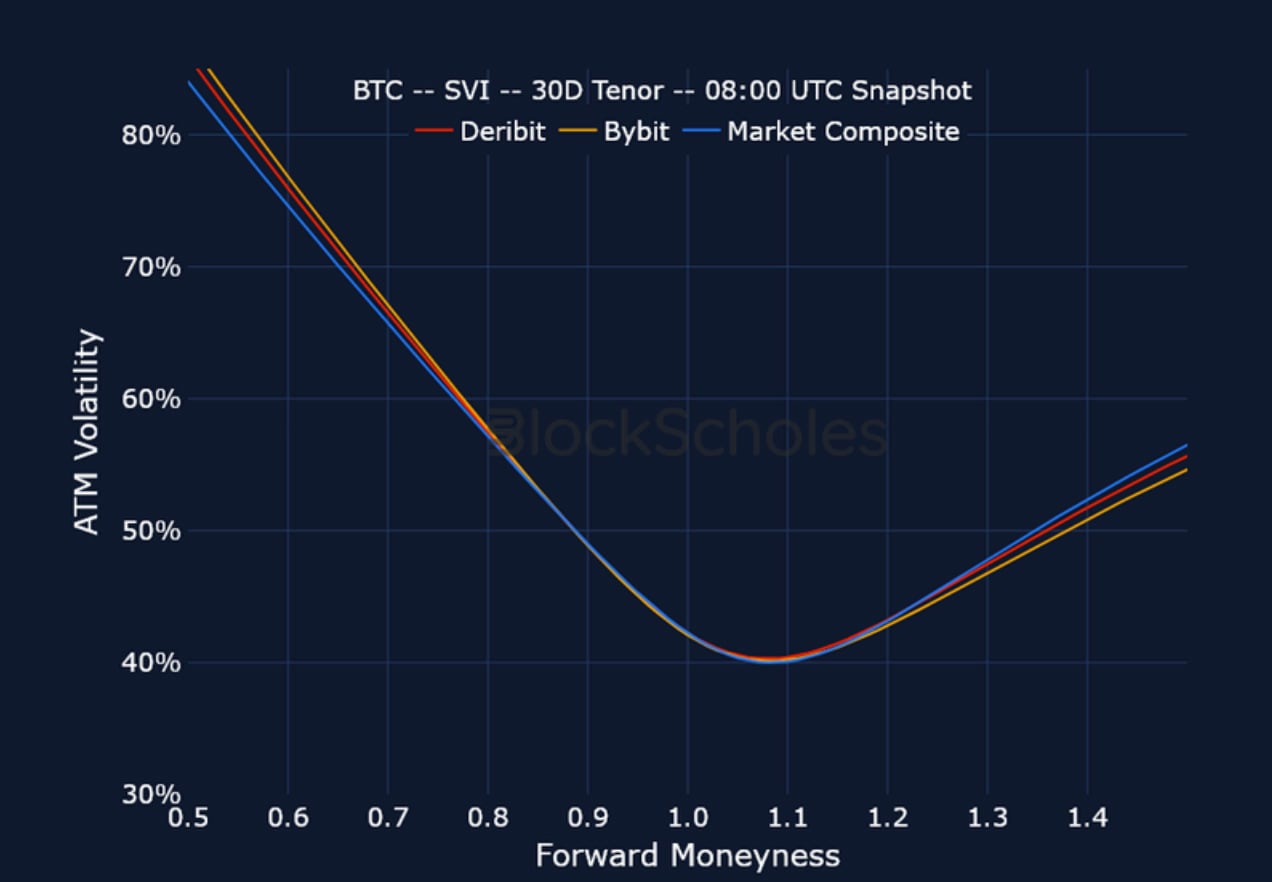

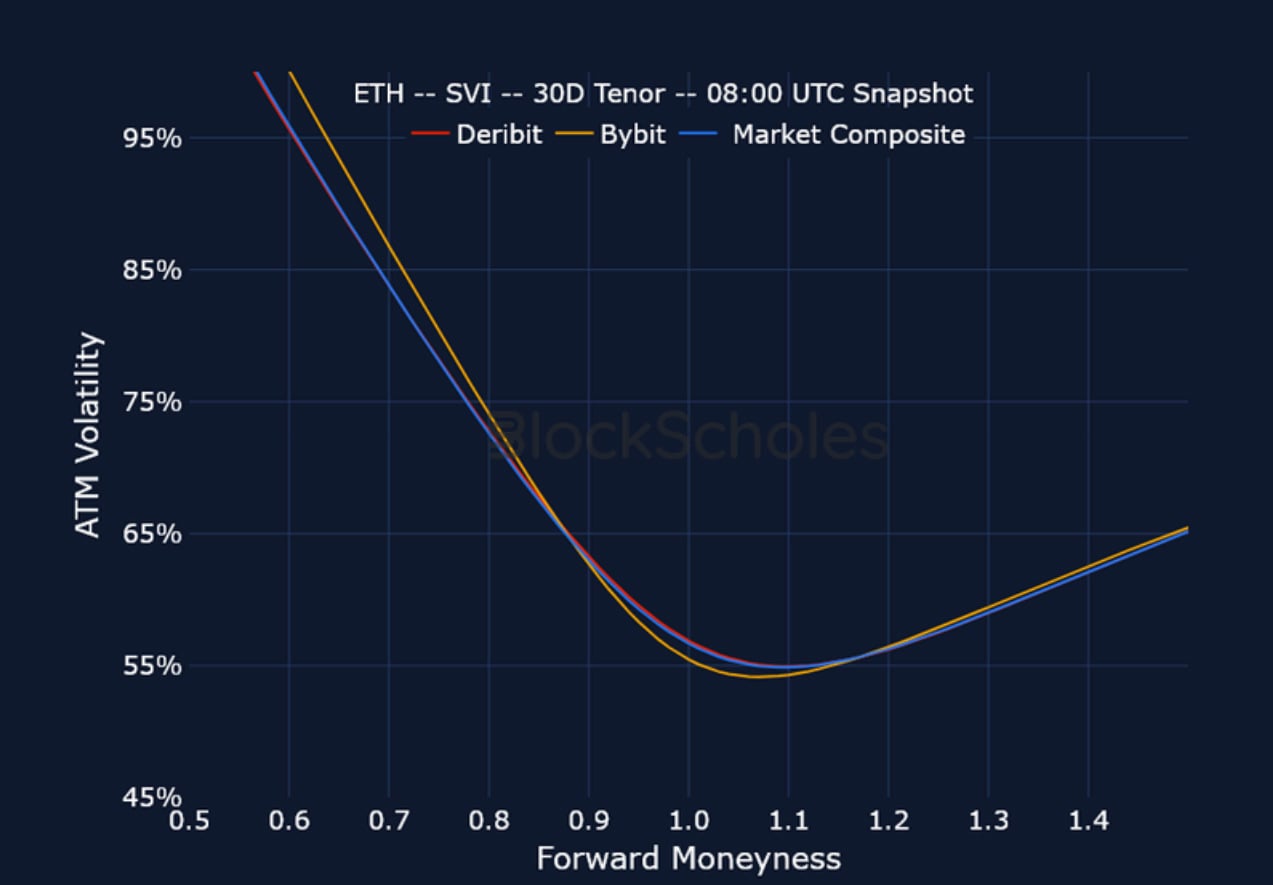

Cross-Exchange Volatility Smiles

BTC SVI, 30D TENOR – 8:00 UTC Snapshot.

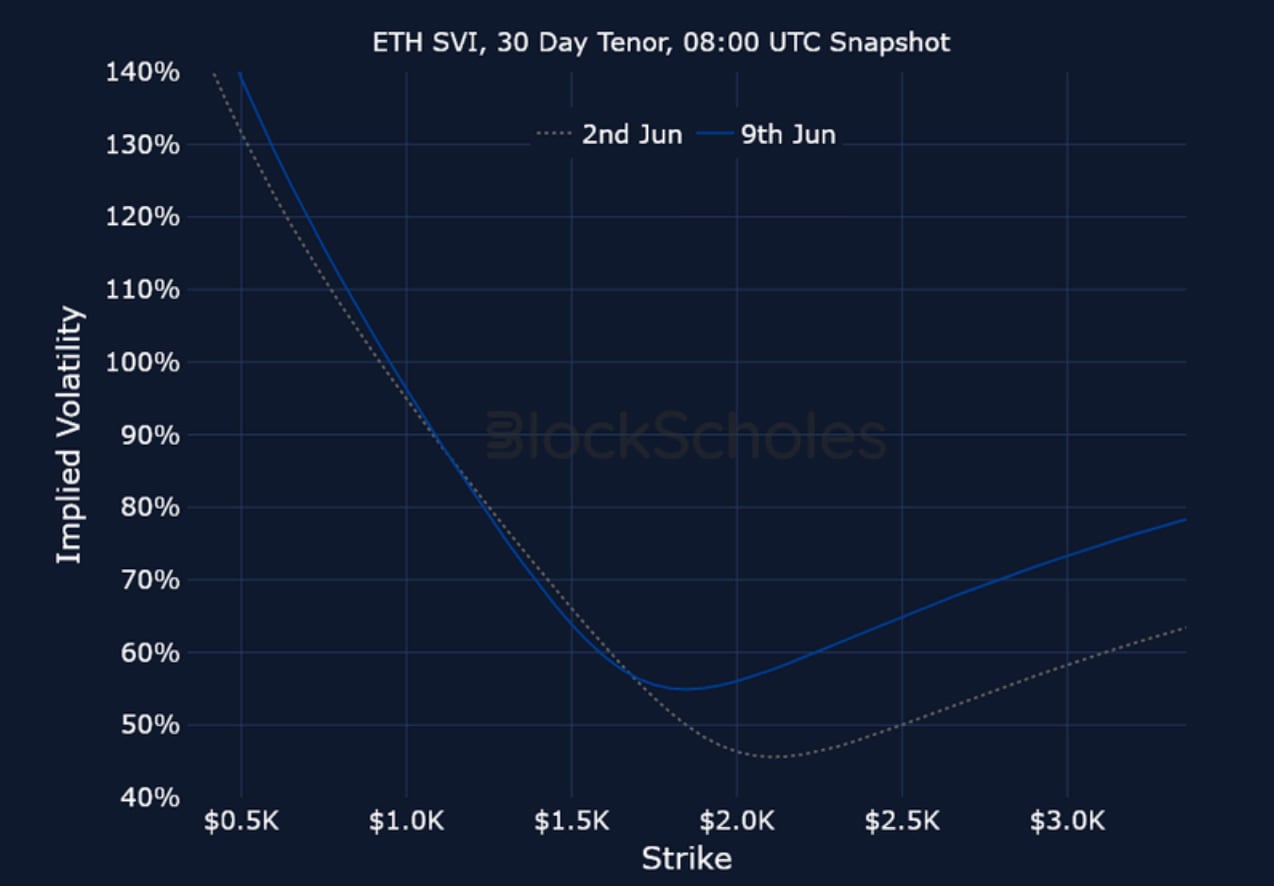

ETH SVI, 30D TENOR – 8:00 UTC Snapshot.

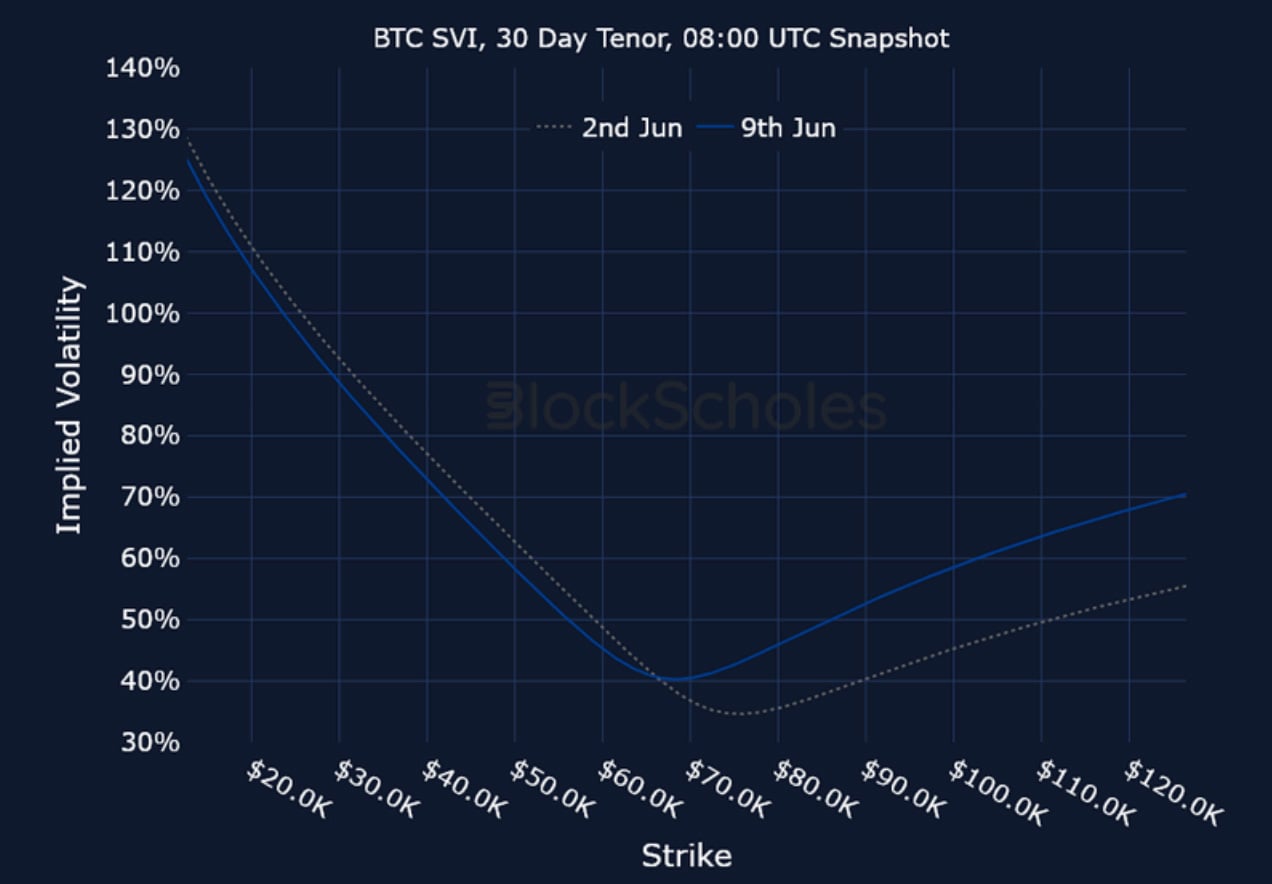

Constant Maturity Volatility Smiles

BTC SVI, 30D TENOR – 8:00 UTC Snapshot.

ETH SVI, 30D TENOR – 8:00 UTC Snapshot.

Data Reference

Block Scholes Risk Appetite (BTC/ETH)

Block Scholes’ Risk Appetite index uses a composite spot index price; POST /api/v1/price/index

1-month ATM implied volatility (BTC/ETH)

At-the-money IV at a constant 1-month tenor; forward- looking vol expectations; POST /api/v1/iv/moneyness

Volatility term structure & SVI ATM IV by tenor (BTC/ETH)

SVI-fitted ATM IV across constant tenors (7d / 14d / 30d / 90d / 180d); POST /api/v1/modelparams

25-delta risk reversal / skew (BTC/ETH)

Spread between 25Δ call and 25Δ put IV; a measure of upside vs downside option demand; POST /api/v1/iv/risk-reversal

Market composite volatility surface (BTC/ETH)

BlockScholes composite SVI surface across forward moneyness and tenor, aggregating market-wide options pricing into one clean fitted surface; POST /api/v1/iv/moneyness + POST /api/v1/modelparams

Cross-exchange volatility smiles (BTC/ETH)

Venue-level (Deribit, Bybit) and composite smiles at a fixed tenor, for comparing exchange pricing against the market composite; POST /api/v1/iv/moneyness

Constant-maturity volatility smiles (BTC/ETH)

Like-for-like smile at a fixed tenor across strikes, showing how the smile shifted between dates; POST /api/v1/iv/strike

Disclaimer

This article reflects the personal views of its author, not Deribit or its affiliates. Deribit has neither reviewed nor endorsed its content.

Deribit does not offer investment advice or endorsements. The information herein is informational and shouldn’t be seen as financial advice. Always do your own research and consult professionals before investing.

Financial investments carry risks, including capital loss. Neither Deribit nor the article’s author assumes liability for decisions based on this content.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.