Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

After falling below $60K, a level last seen in October 2024, BTC reached a two-week high above $67K. Sentiment across risk-on assets has rebounded after President Trump confirmed the electronic signing of a Memorandum of Understanding (MOU) with Iran, pushing down oil prices and causing markets to re- evaluate the probability of a Fed rate hike by year-end. In derivatives markets, much of the bearish premium that options traders had assigned earlier in the month has reversed with 7-day skew reaching -2.2% and -0.7% respectively for BTC and ETH.

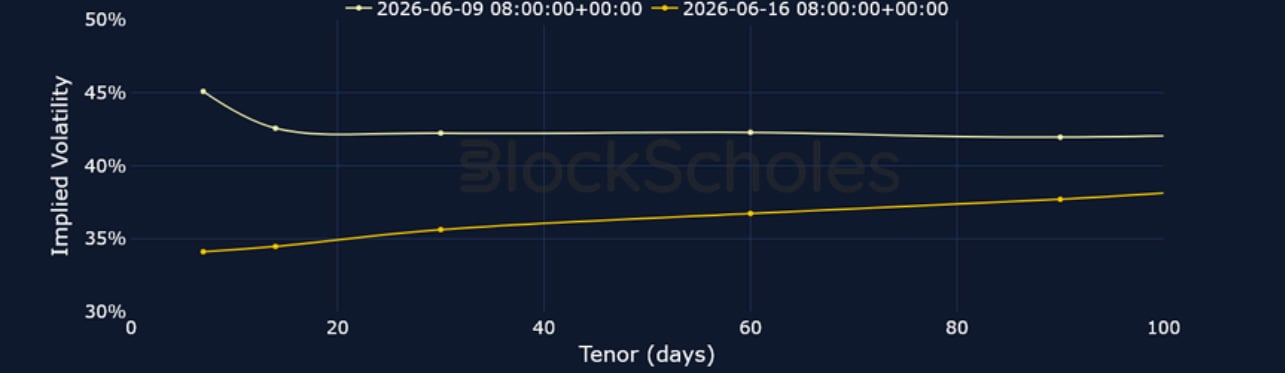

The moves towards a more permanent peace deal have also seen at-the-money implied volatility fall back towards its year-to-date lows, in line with a summer volatility lull that we’ve seen every year since 2023. 7- day ATM IV currently trades around 33%, only a few percentage points above the May YTD low of 28%.

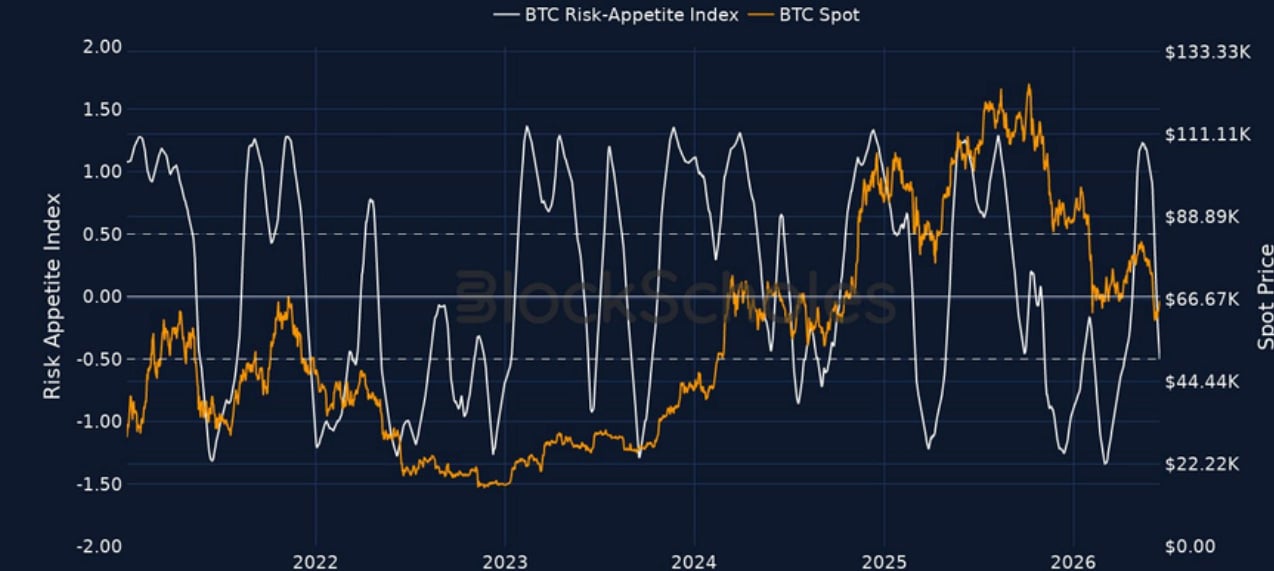

Block Scholes BTC Risk Appetite Index

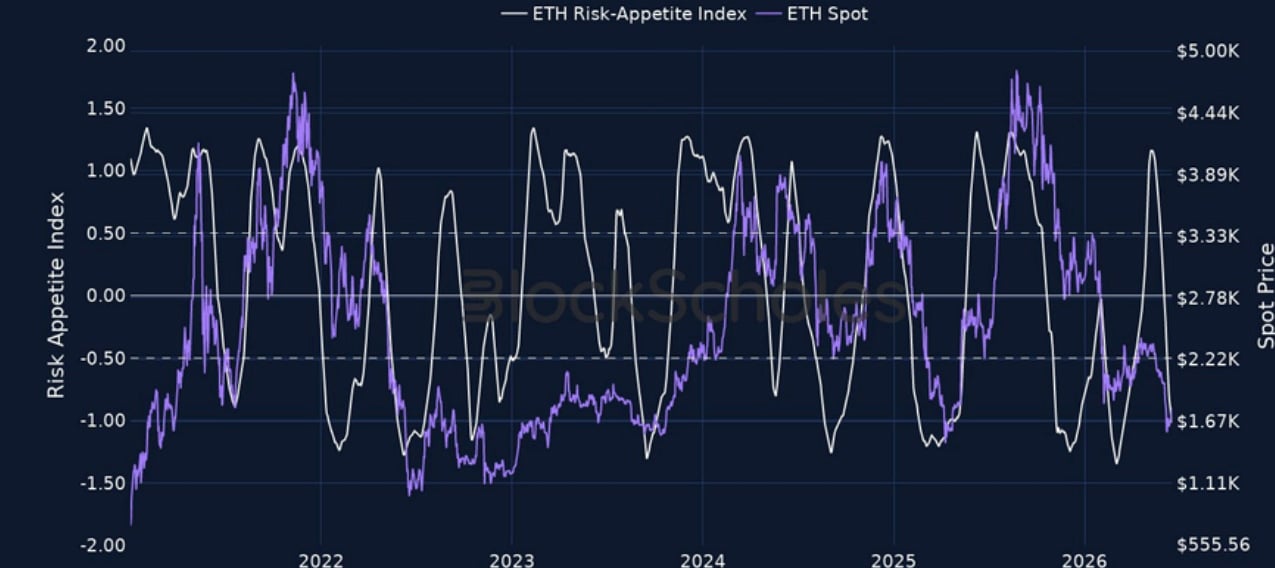

Block Scholes ETH Risk Appetite Index

1-Month Tenor ATM Implied Volatility

BTC Options

BTC SVI ATM IMPLIED VOLATILITY – The summer volatility lull that we’ve seen since 2023 is visible as 7-day vol trades slightly above the YTD low of 28%.

ETH Options

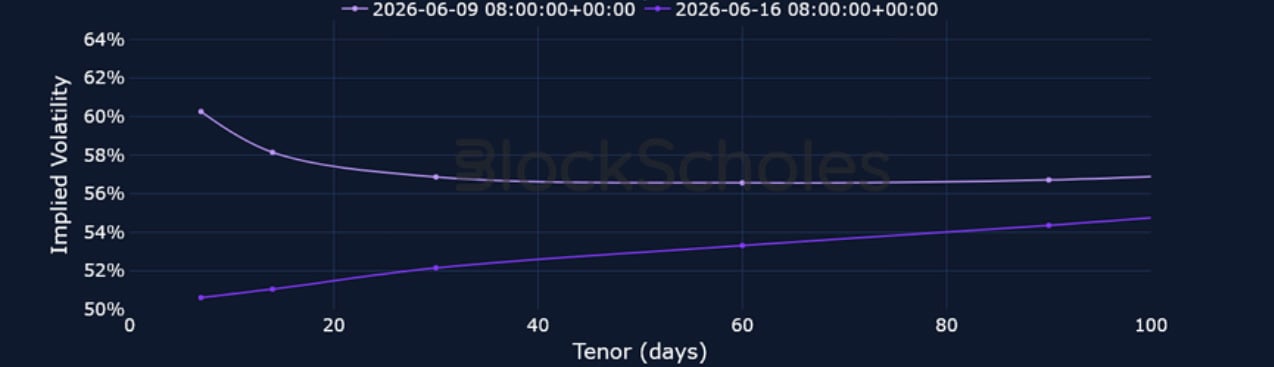

ETH SVI ATM IMPLIED VOLATILITY – ETH’s term structure has normalised from last week’s mild inversion.

BTC and ETH Skew

BTC 25-Delta Risk Reversal – With spot price briefly trading above $67K, volatility smiles have continued to price out the skew towards put options. While still negative, the 25-delta for 7-day options reached -2.2%, a one- month high.

ETH 25-Delta Risk Reversal – The volatility smile for ETH is slightly less bearish than BTC as the 25-delta put-call skew traded at -0.8% when ETH spot price broke through $1,800.

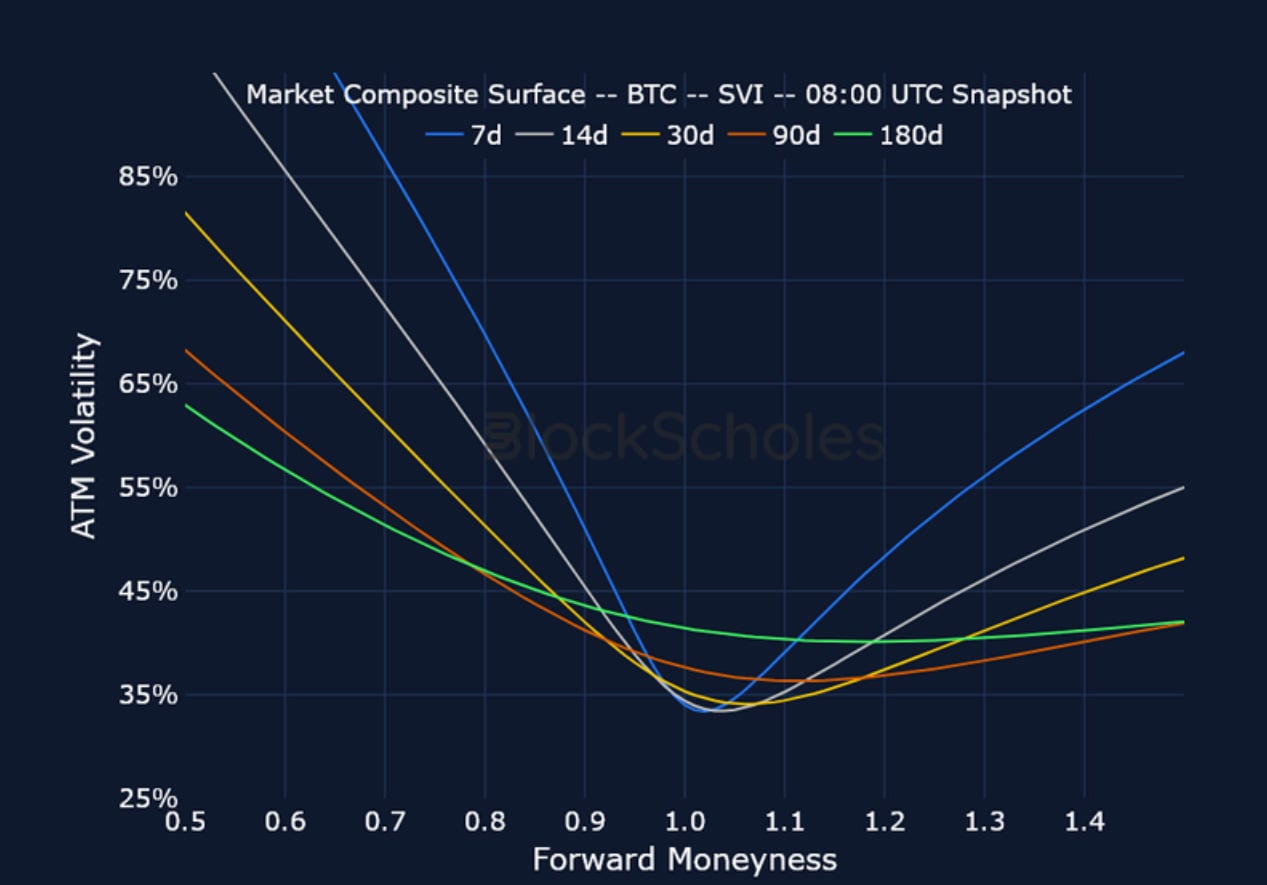

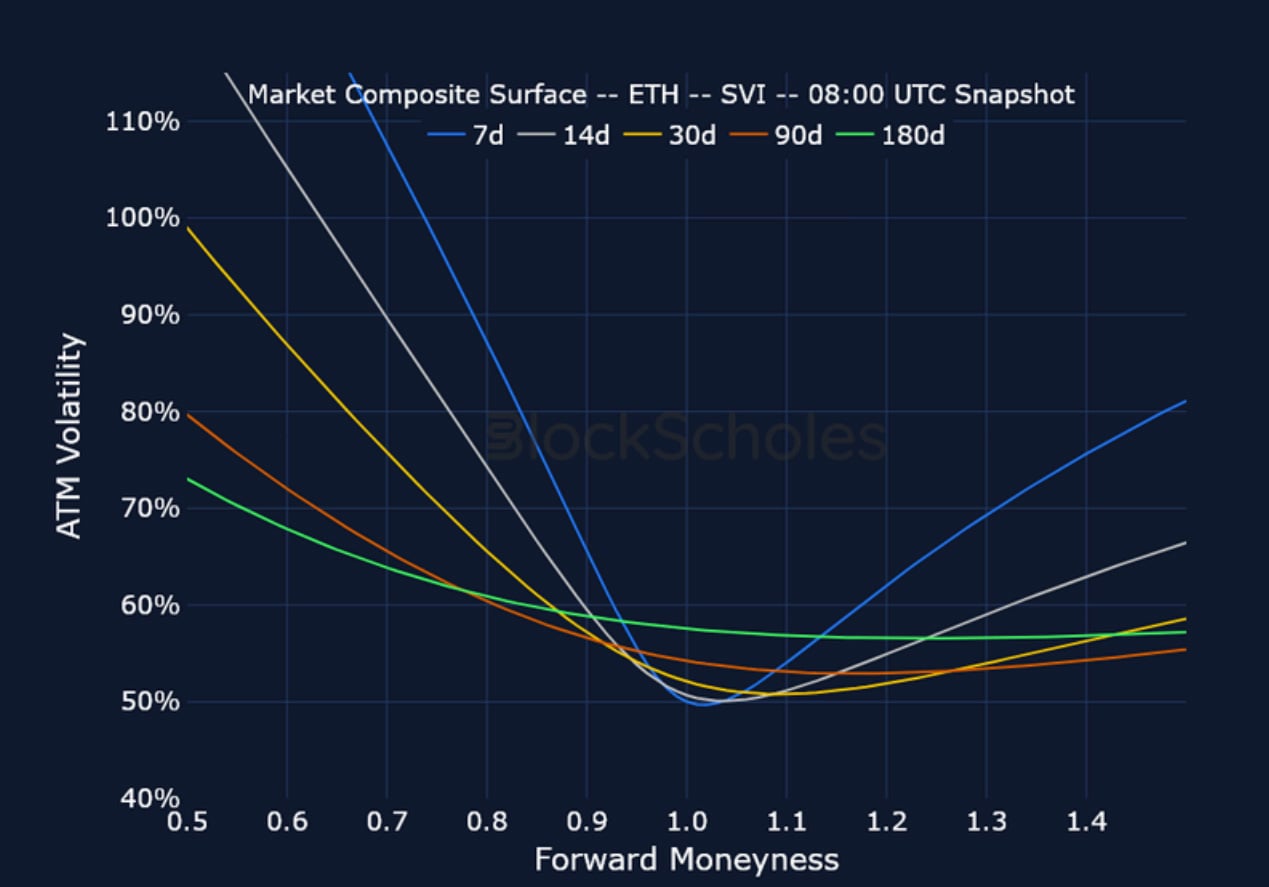

Market Composite Volatility Surface

BTC SVI – 8:00 UTC Snapshot.

ETH SVI – 8:00 UTC Snapshot.

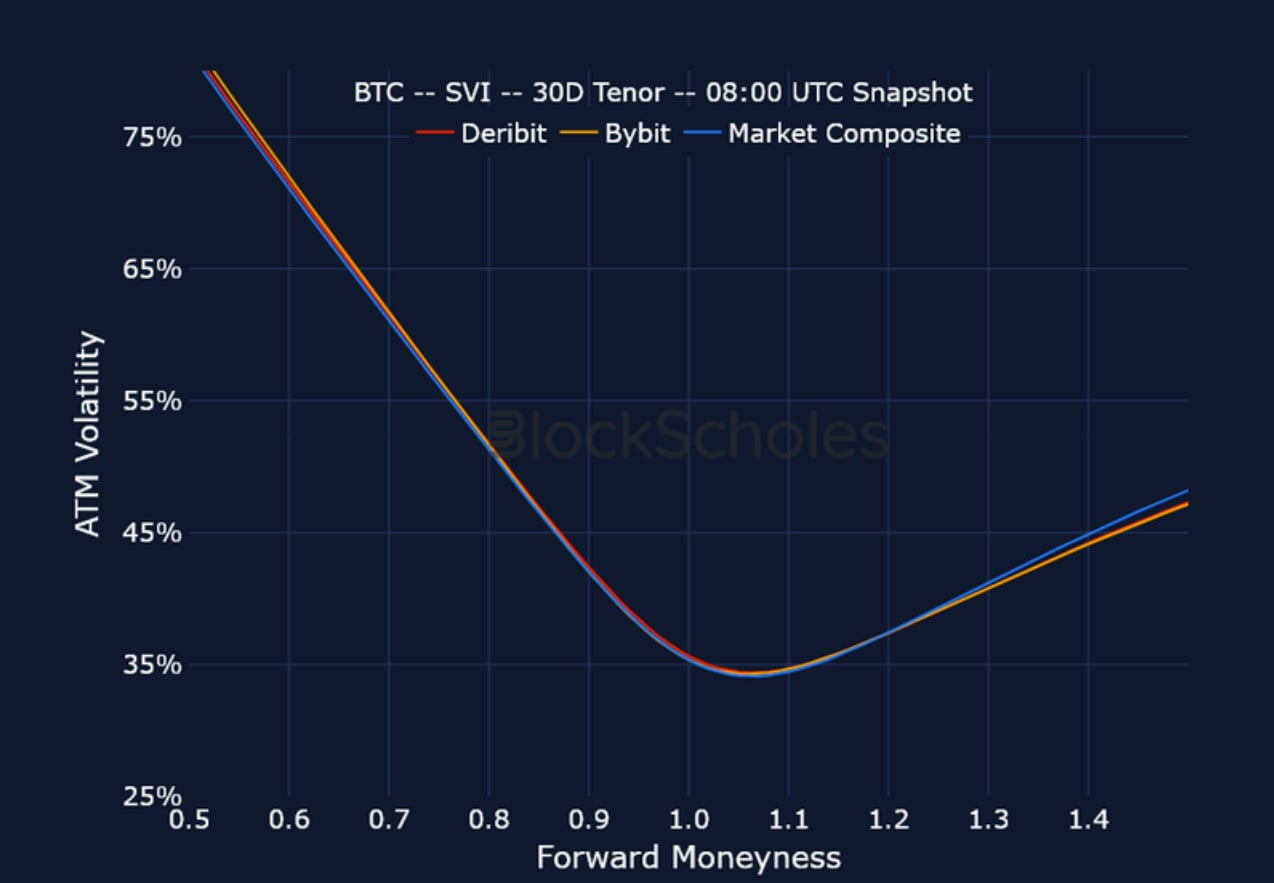

Cross-Exchange Volatility Smiles

BTC SVI, 30D TENOR – 8:00 UTC Snapshot.

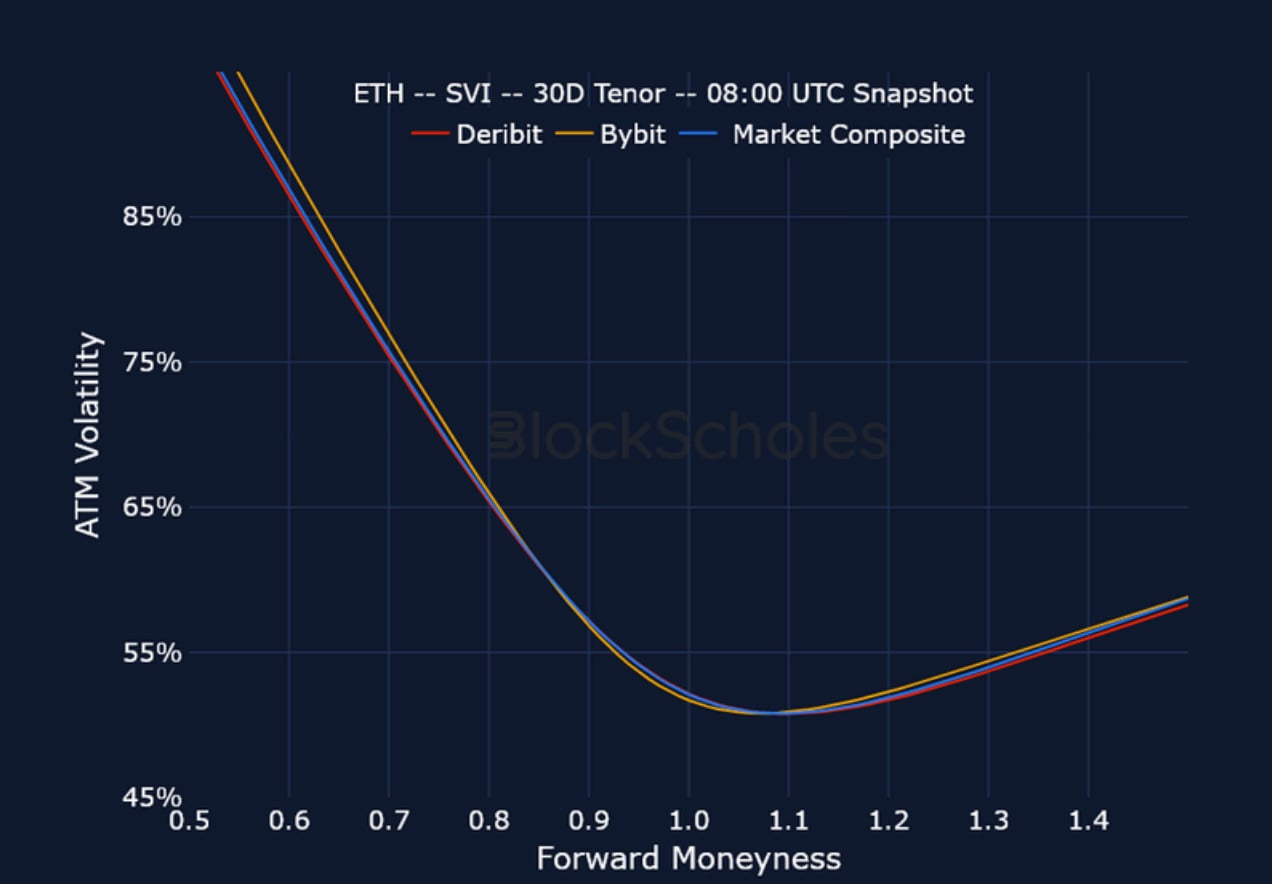

ETH SVI, 30D TENOR – 8:00 UTC Snapshot.

Constant Maturity Volatility Smiles

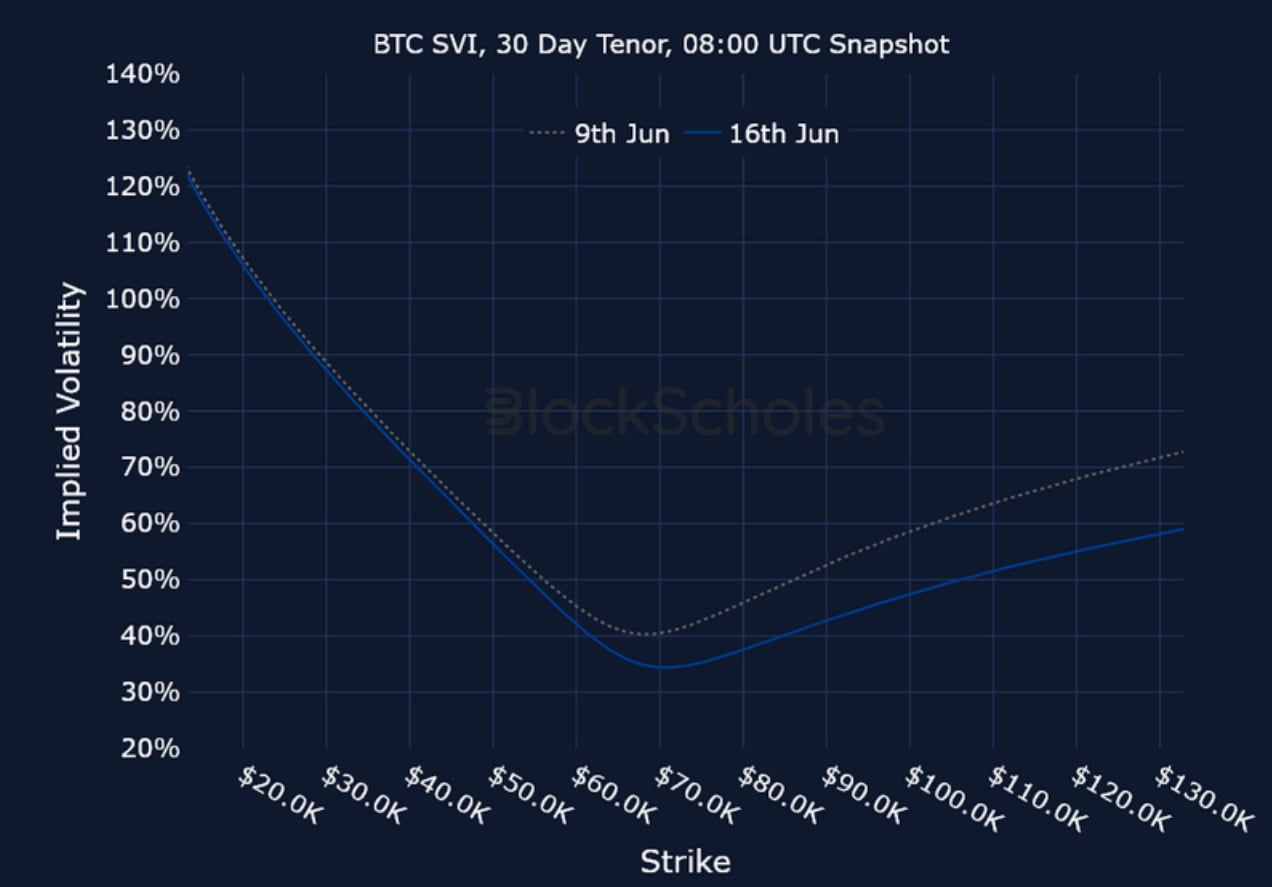

BTC SVI, 30D TENOR – 8:00 UTC Snapshot.

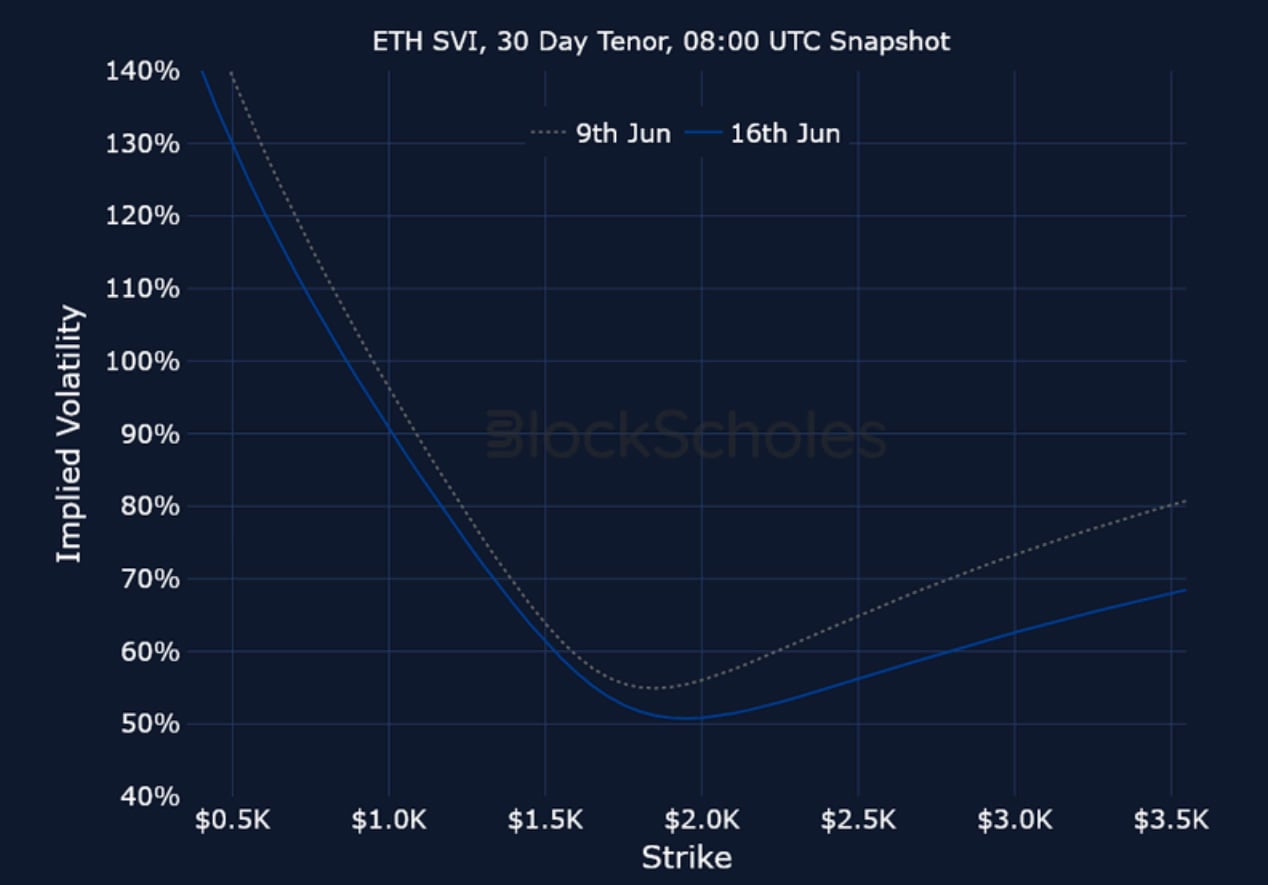

ETH SVI, 30D TENOR – 8:00 UTC Snapshot.

Data Reference

Block Scholes Risk Appetite (BTC/ETH)

Block Scholes’ Risk Appetite index uses a composite spot index price; POST /api/v1/price/index

1-month ATM implied volatility (BTC/ETH)

At-the-money IV at a constant 1-month tenor; forward- looking vol expectations; POST /api/v1/iv/moneyness

Volatility term structure & SVI ATM IV by tenor (BTC/ETH)

SVI-fitted ATM IV across constant tenors (7d / 14d / 30d / 90d / 180d); POST /api/v1/modelparams

25-delta risk reversal / skew (BTC/ETH)

Spread between 25Δ call and 25Δ put IV; a measure of upside vs downside option demand; POST /api/v1/iv/risk-reversal

Market composite volatility surface (BTC/ETH)

BlockScholes composite SVI surface across forward moneyness and tenor, aggregating market-wide options pricing into one clean fitted surface; POST /api/v1/iv/moneyness + POST /api/v1/modelparams

Cross-exchange volatility smiles (BTC/ETH)

Venue-level (Deribit, Bybit) and composite smiles at a fixed tenor, for comparing exchange pricing against the market composite; POST /api/v1/iv/moneyness

Constant-maturity volatility smiles (BTC/ETH)

Like-for-like smile at a fixed tenor across strikes, showing how the smile shifted between dates; POST /api/v1/iv/strike

Disclaimer

This article reflects the personal views of its author, not Deribit or its affiliates. Deribit has neither reviewed nor endorsed its content.

Deribit does not offer investment advice or endorsements. The information herein is informational and shouldn’t be seen as financial advice. Always do your own research and consult professionals before investing.

Financial investments carry risks, including capital loss. Neither Deribit nor the article’s author assumes liability for decisions based on this content.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.