Crypto Revival as GBTC Selling Slows

Bitcoin’s market has shown choppy moves 3 weeks following ETF introductions, struggling to establish a bullish footing. Attempts to surpass the $45,000 resistance or maintain a value sub $40,000 support have repeatedly failed.

The initial price increase was countered by withdrawals from the Grayscale Bitcoin Trust, balanced by inflows into other ETFs and purchases ahead of Bitcoin’s halving event in the spring, which is traditionally a bullish event for Bitcoin.

It’s worth noting that the rate of withdrawals from Grayscale’s spot ETF is decreasing, while ETFs from Blackrock and Fidelity continue to attract Bitcoin investments, each gathering roughly $2 billion since launch. Analysis from JP Morgan hints that the selling from GBTC might be mostly over, implying a market shift towards accumulation as the halving approaches.

The balanced funding rates suggest a decline in speculative trading, which means there is plenty of room for additional flows before the market reaches saturation.

Meanwhile, Ethereum has lagged behind, with the ETHBTC ratio falling since its high on January 20. The anticipated ‘Dencun’ upgrade is likely to act as a positive catalyst for ETH, along with speculation about an Ethereum spot ETF. This all suggests potential for price appreciation in coming months.

‘Call Wall’ of Resistance in ETH

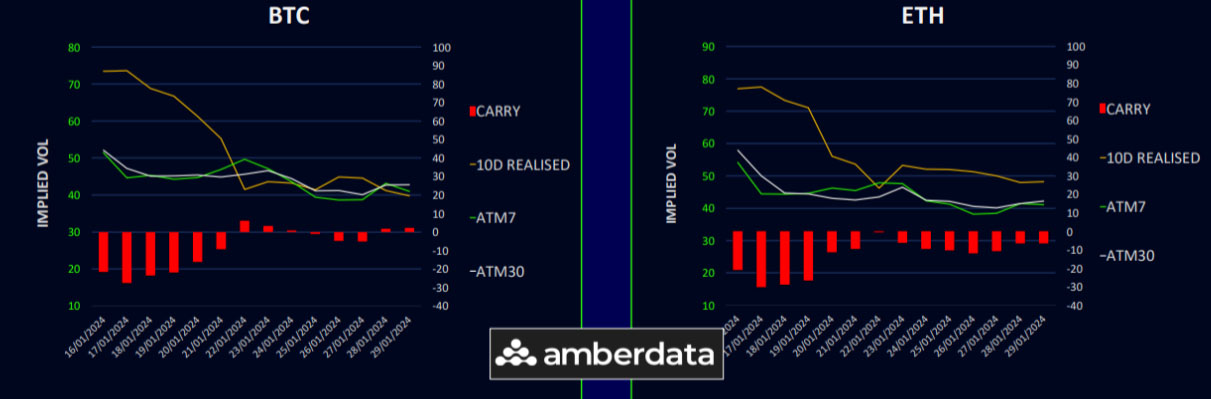

This week, Bitcoin’s 10-day realized volatility decreased to 40% and Ethereum’s to 48%. Weekly implied volatilities (pure gamma) also dropped, particularly for short-term expirations, by 6-7 points vs a more stable 1-month implied. Bitcoin’s volatility carry is slightly positive, while Ethereum’s is significantly negative due to a decline in implied volatilities as massive call selling has been seen, which may cause real difficulties to see further rallies in the near term. This gamma positioning is creating a ‘call wall’ of resistance.

Term Structures Falling Back into Contango

Bitcoin’s term structure has returned to contango as expected with a decline in realized volatility. The most significant change was in weekly volatilities, down by about 4 points. Forward vol premiums are slightly higher for expiries post-April, capturing the halving event.

Ethereum’s term structure is similar with a slight contango, with gamma buckets trading lower due to strong selling pressure that are overwhelming market makers’ books. VEGA is still well offered, even in the back-end expiries which were down 1-2 vols.

Longer Dated Call Switches in ETH/BTC Favoured

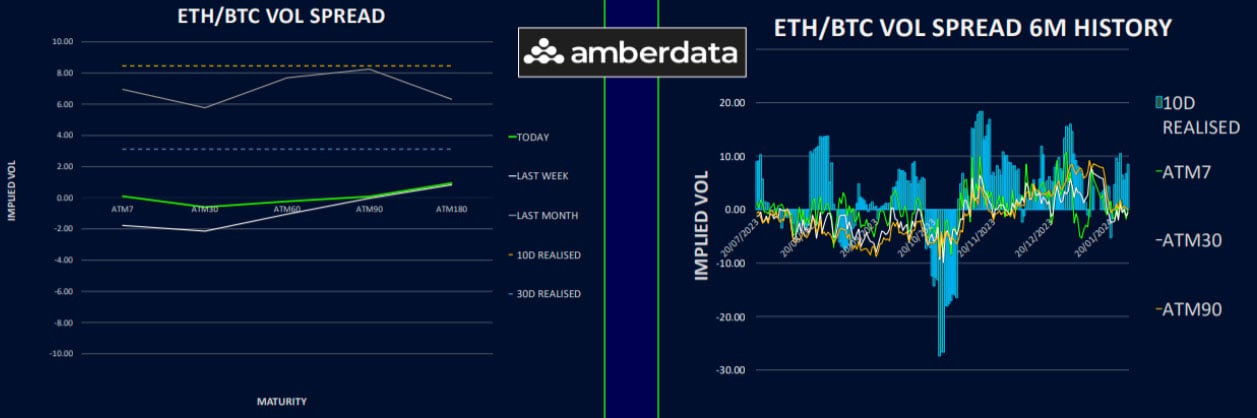

The ETH/BTC volatility spread is mostly stable, with weeklies fluctuating erratically on a daily basis. Ethereum continues to show 8 vols higher realized volatility than Bitcoin.

Owning the spread continues to offer decent value from a realized gamma perspective if one is interested to delta hedge the moves. Watch for sticky long strikes on the upside for ETH, which may cause this realized outperformance to dissipate.

The ETH/BTC spot spread retracted 13% from January highs, suggesting a good entry point for those bullish on Ethereum. Long-dated call switches were recently flagged to our subscribers in order to leverage Ethereum’s potential against Bitcoin.

We are cognizant that the short-term gamma positioning may act as a vol dampener for ETH in the near term though, and so we decided to use far OTM calls with longer expiries.

Skew Flips Back Into Call Premium

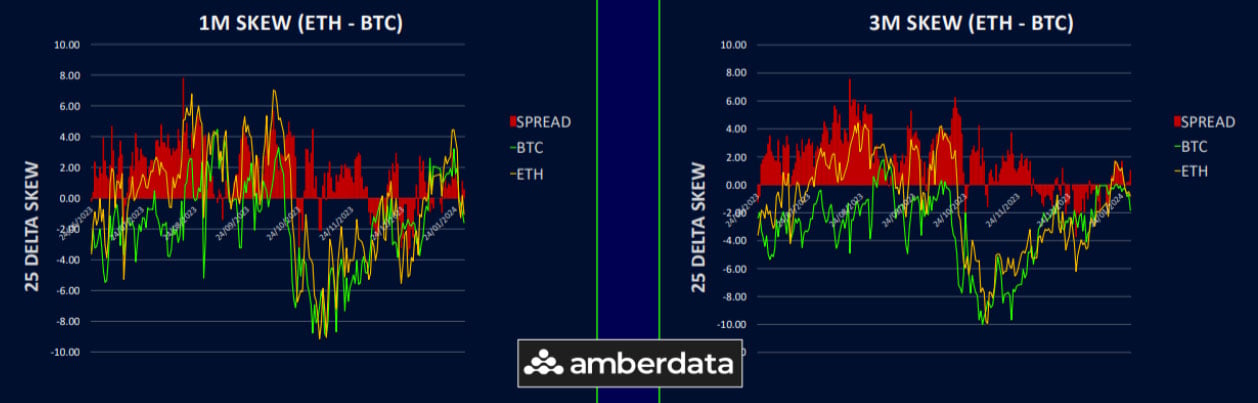

Bitcoin’s skew structure has shifted to call premium after the rally, with the front end seeing a 2 vol premium increasing to 5 vols in longer expiries.

Ethereum shows a similar move but with a more modest 1 vol call premium for up to 3-month expiries as the bullish ETH narrative seems to be getting pushed out in time.

Call overwriting is prevalent in Ethereum flows and may cap call skews, especially in the front-end. In turn, this may potentially keep realized volatility low.

Just remember that once a strong enough fundamental reason takes hold, call sellers may need to cover, and this can reverse the vol dynamics quickly.

Option Flows And Dealer Gamma Positioning

Bitcoin options volumes rose by 10% this week, mainly in calls, with significant interest in March 29 50k and 75k calls. A notable trade was buying April 26, 41k straddles against selling February 23, 37k/45k strangles.

Ethereum’s volumes also increased by 10%, with notable trades in bullish risk reversals and put spreads. Largest volume was on screen selling of 23Feb 2400 & 2500 calls (rolling down short 2700s) from the big overwriter.

Dealer gamma positioning in Bitcoin has neutralized after large 26Jan 42k short strikes expires and fresh sellers of 23Feb options came in last week. Meanwhile, Ethereum’s gamma positioning has significantly increased, indicating a potential challenge for major movements without significant news.

Strategy Compass: Where Does The Opportunity Lie?

Using the recent pop in crypto prices to enter short term some hedges makes sense. Put spread collars tend to work well with vol in the 40s.

For those who don’t have enough ETH exposure already, we really like ETH calls vs BTC calls in Jun24 to Dec24 expiries.

To get full access to Options Insight Research including our proprietary crypto volatility dashboards, options flows, gamma positioning analysis, crypto stocks screener and much more, Visit Options Insights here.

Disclaimer

This article reflects the personal views of its author, not Deribit or its affiliates. Deribit has neither reviewed nor endorsed its content.

Deribit does not offer investment advice or endorsements. The information herein is informational and shouldn’t be seen as financial advice. Always do your own research and consult professionals before investing.

Financial investments carry risks, including capital loss. Neither Deribit nor the article’s author assumes liability for decisions based on this content.

AUTHOR(S)

Imran Lakha is an expert at using institutional options strategies to capitalize on investment opportunities across global macro asset classes. Learn more here.