Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

Another move above $100K for BTC’s spot price has come along with a moderately bullish sentiment across all derivatives markets – a re-inversion of the positive futures-implied yields, a healthy funding rate collected by short positions, and a skew towards calls at all tenors. However, we do not see the same level of exuberance in leveraged positions that had marked the first two forays above the key psychological 6-figure mark. Implied volatility levels are lower and term structures remain steep. Futures yields, while positive, are below their post-election highs and trending lower. Ethereum retains its volatility premium over BTC options, owing largely to its higher level of delivered volatility, while sentiment remains slightly less bullish in all metrics.

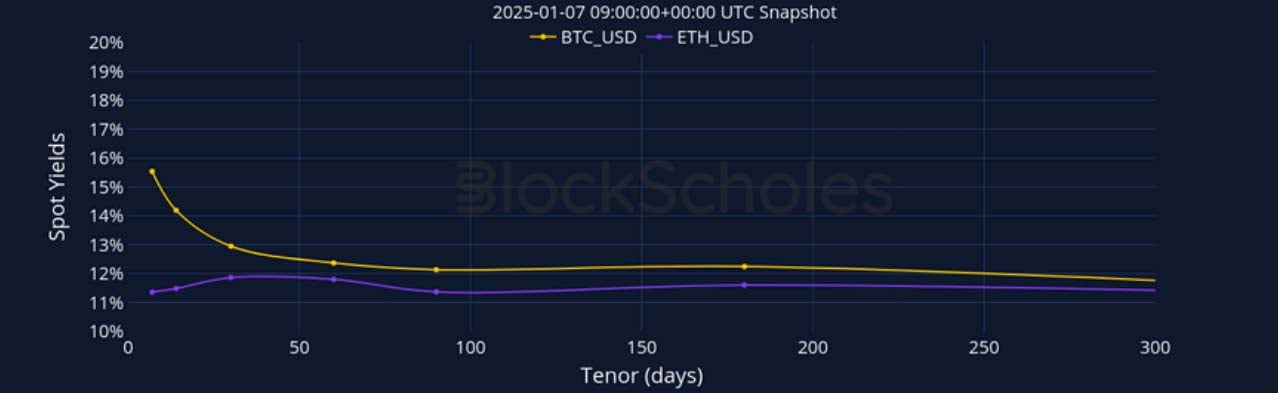

Futures Implied Yield, 1-Month Tenor

ATM Implied Volatility, 1-Month Tenor

Crypto Senti-Meter

BTC Derivatives Sentiment

ETH Derivatives Sentiment

Futures

BTC ANNUALISED YIELDS – After recovering strongly at the turn of the year, BTC’s futures yields trend down and flatter in the following week.

ETH ANNUALISED YIELDS – Yields trend down with a flat term structure, as sideways price action fails to justify the premia of futures prices above spot.

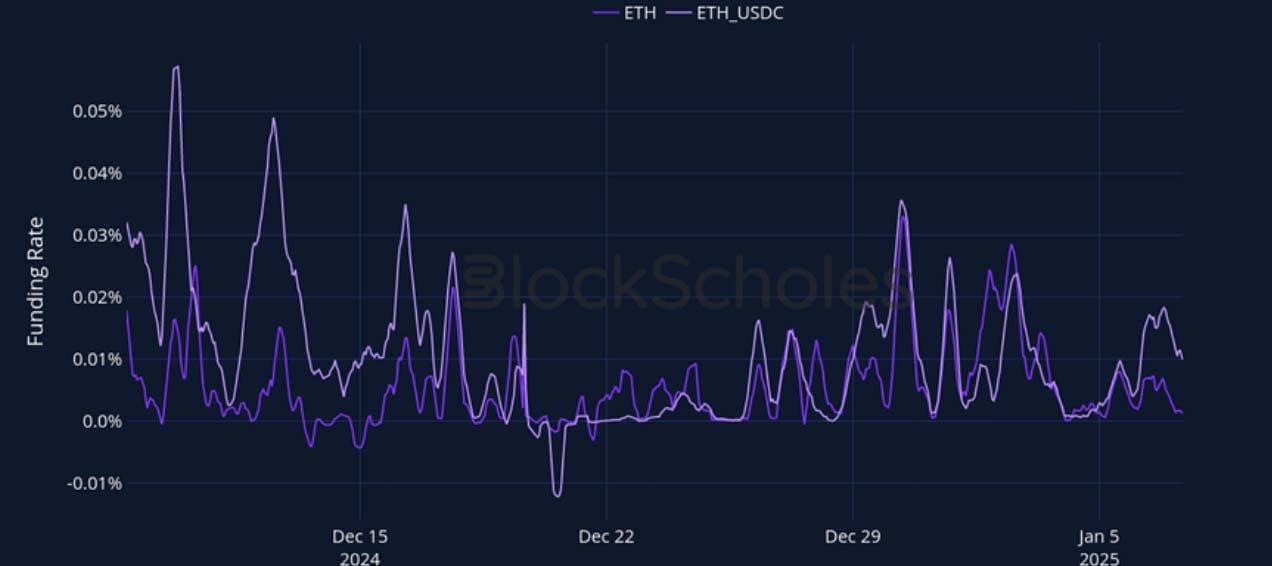

Perpetual Swap Funding Rate

BTC FUNDING RATE – BTC funding rates have reflected a consistent and strong demand for leveraged long positions over the last week.

ETH FUNDING RATE – Last week’s bullishness has been followed by a moderated level of funding rate at the beginning of this one.

BTC Options

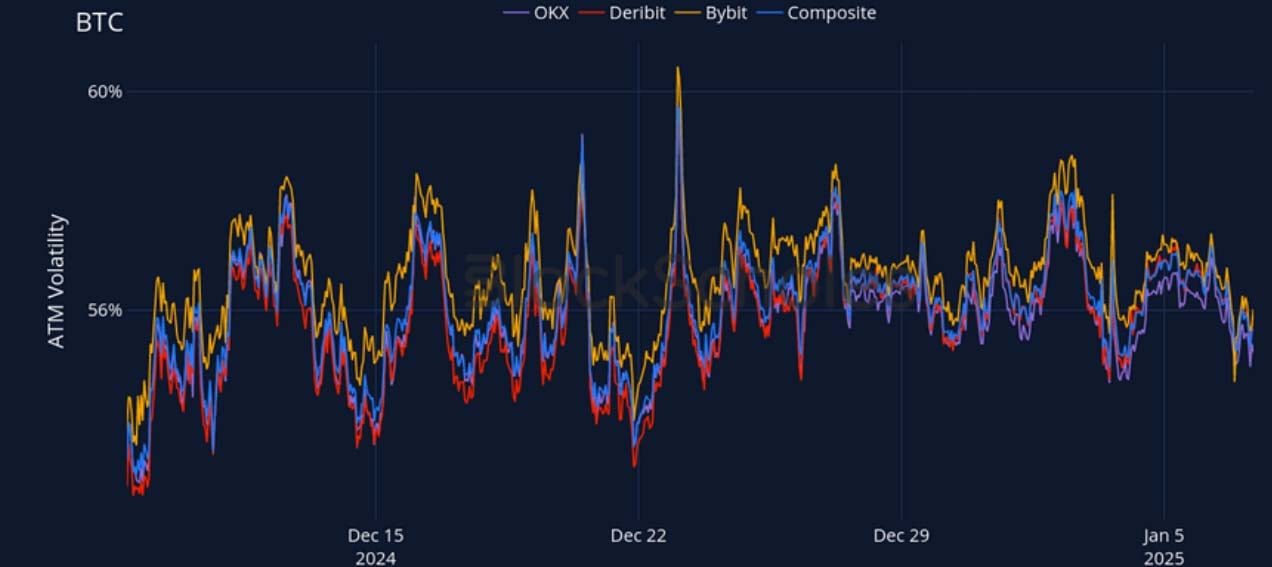

BTC SVI ATM IMPLIED VOLATILITY – Longer-dated volatility is up, while short- tenors trade near their lowest levels of the last month.

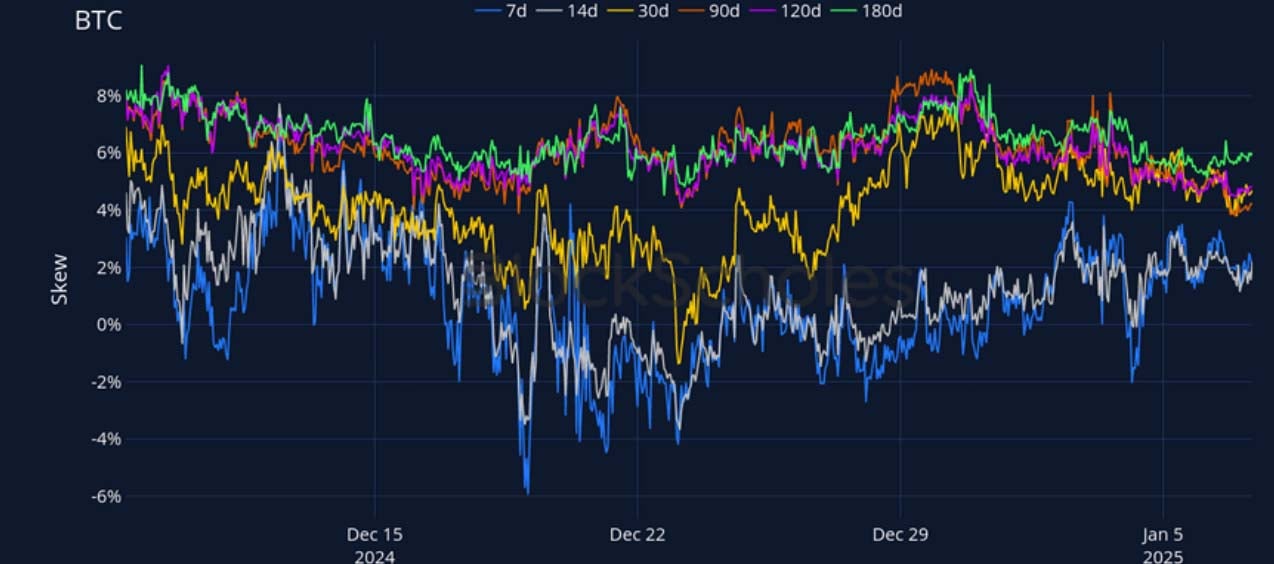

BTC 25-Delta Risk Reversal – Smiles are skewed towards calls at all tenors, but we see a strong divergence between the levels of long and short tenors.

ETH Options

ETH SVI ATM IMPLIED VOLATILITY – The term structure steepness has arisen from a rally in longer-tenor vols while short-tenors have fallen significantly.

ETH 25-Delta Risk Reversal – Short-tenor skews are bullish once again, but retain a gap to the more extreme skew at 3-month tenors and above.

Volatility by Exchange

BTC, 1-MONTH TENOR, SVI CALIBRATION

ETH, 1-MONTH TENOR, SVI CALIBRATION

Put-Call Skew by Exchange

BTC, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

ETH, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

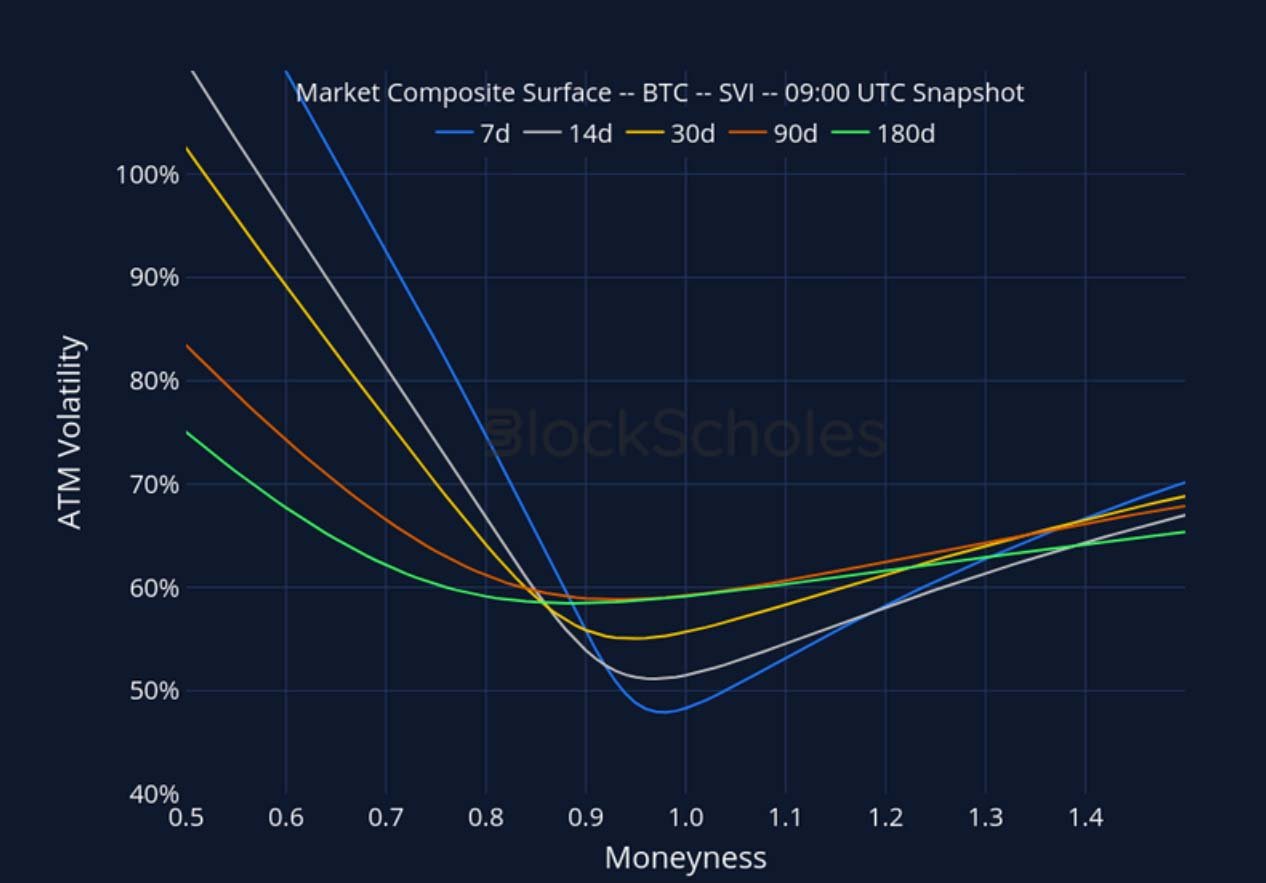

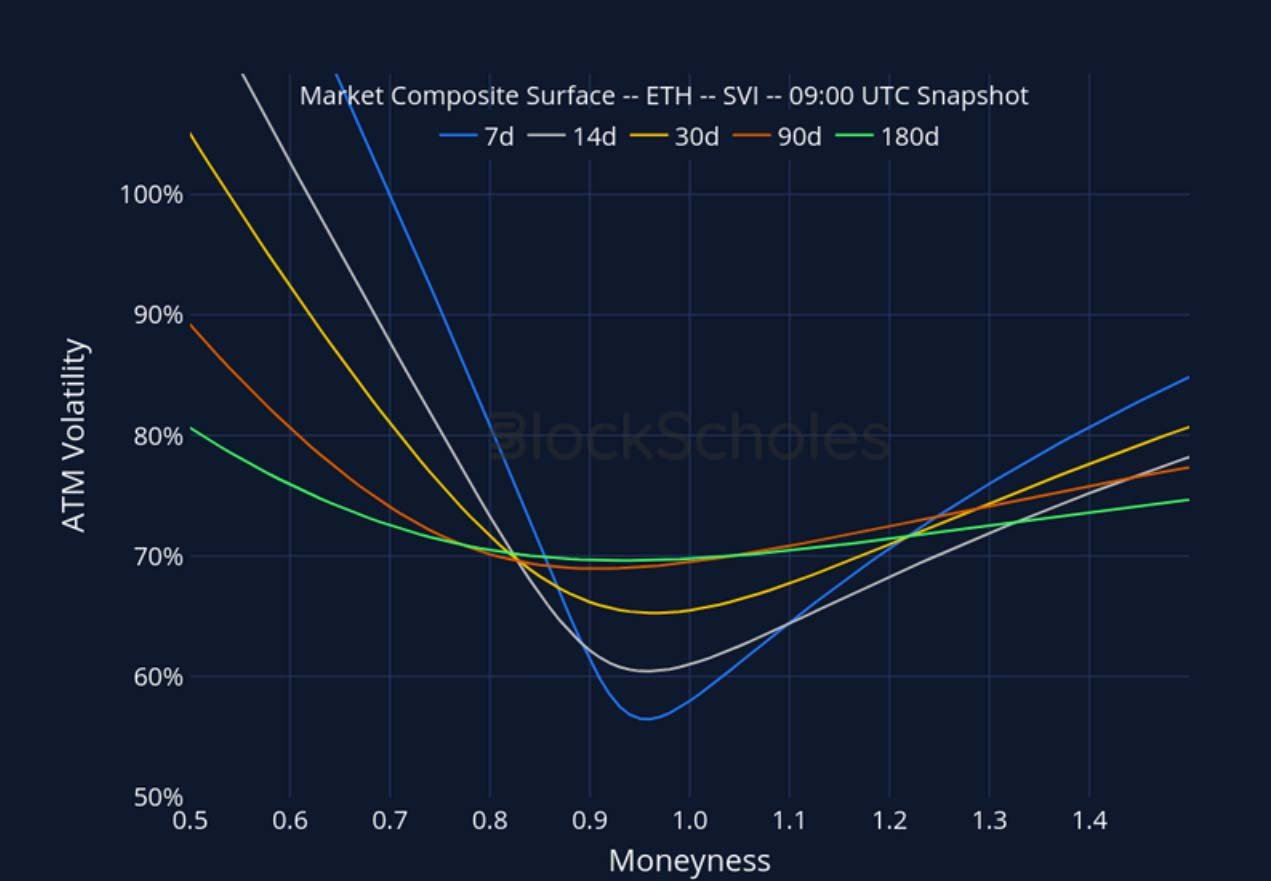

Market Composite Volatility Surface

CeFi COMPOSITE – BTC SVI – 9:00 UTC Snapshot.

CeFi COMPOSITE – ETH SVI – 9:00 UTC Snapshot.

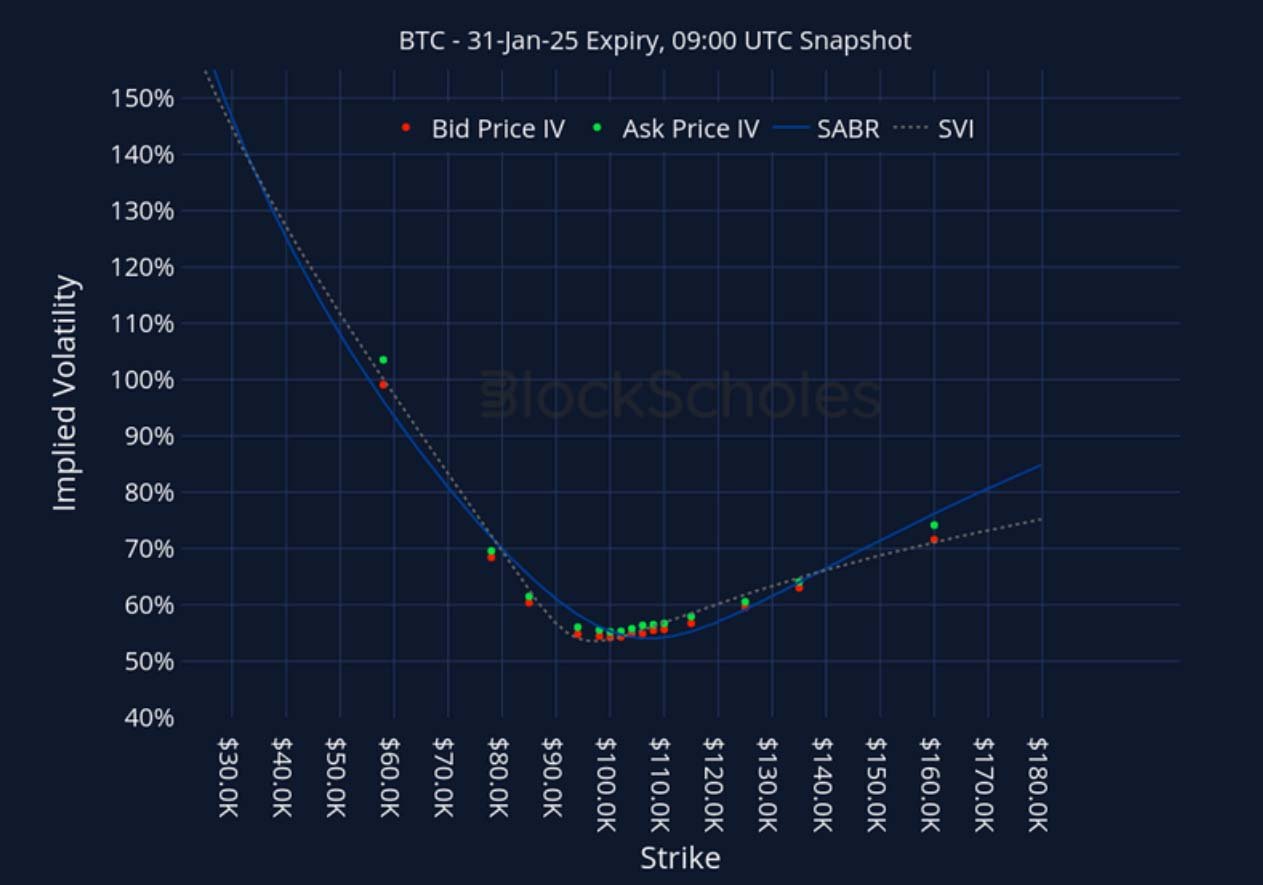

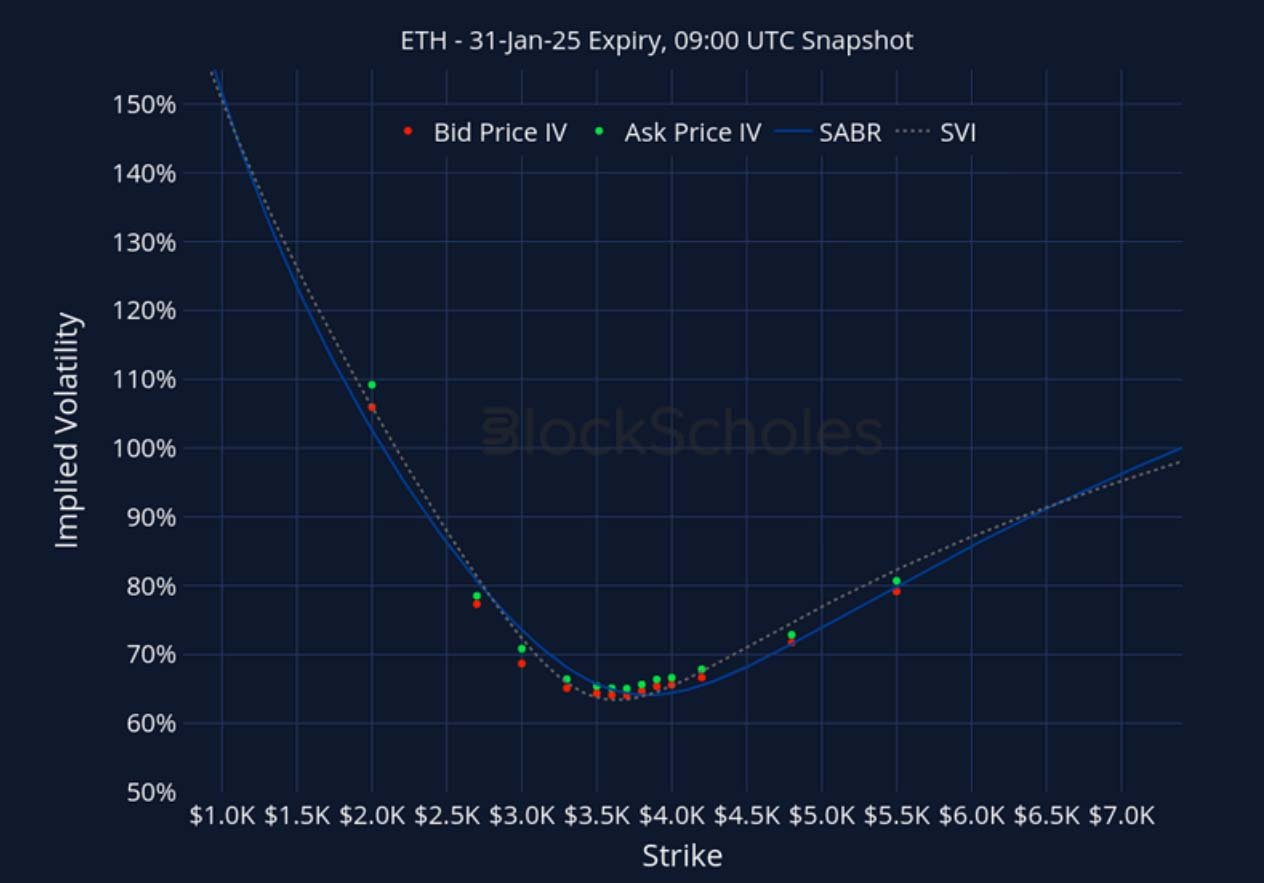

Listed Expiry Volatility Smiles

BTC 31-JAN EXPIRY – 9:00 UTC Snapshot.

ETH 31-JAN EXPIRY – 9:00 UTC Snapshot.

Cross-Exchange Volatility Smiles

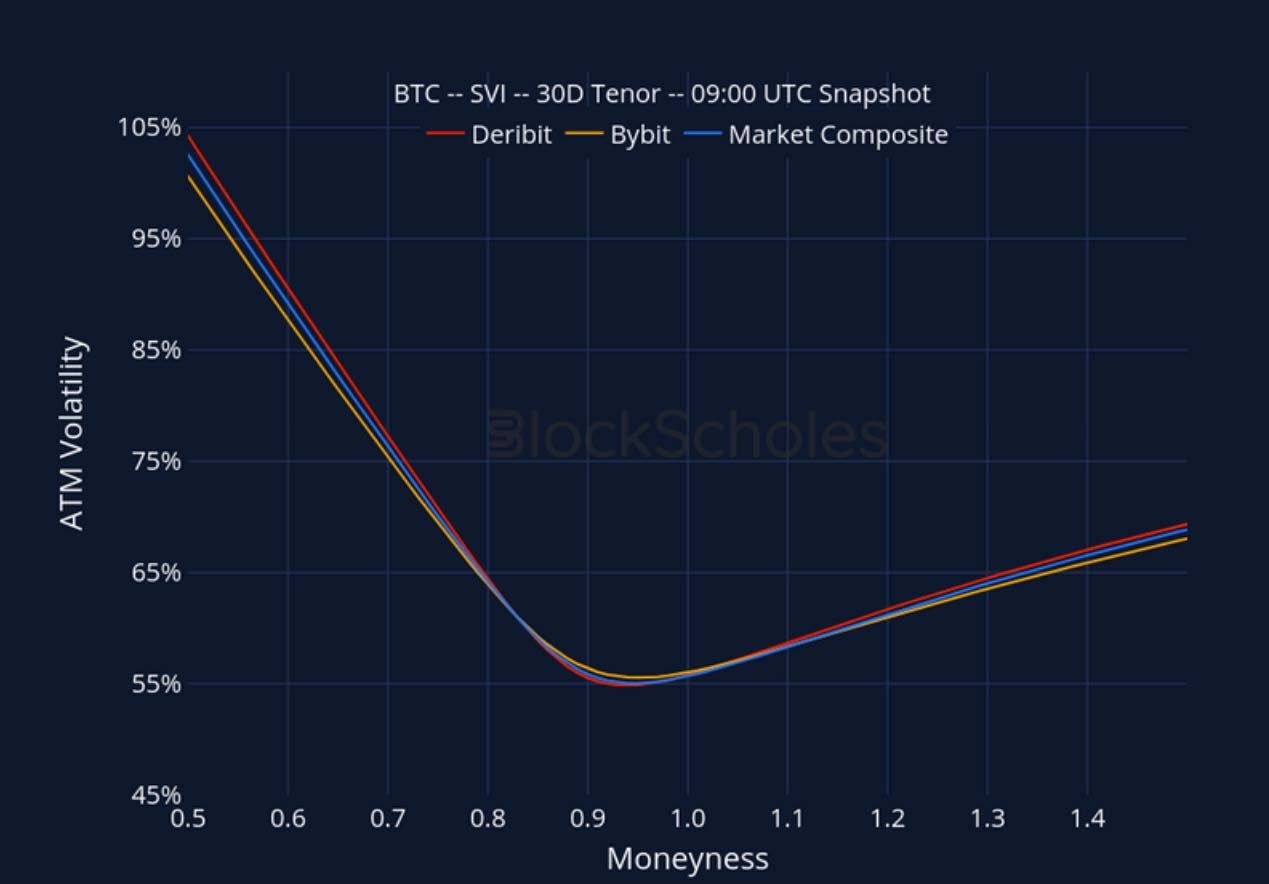

BTC SVI, 30D TENOR – 9:00 UTC Snapshot.

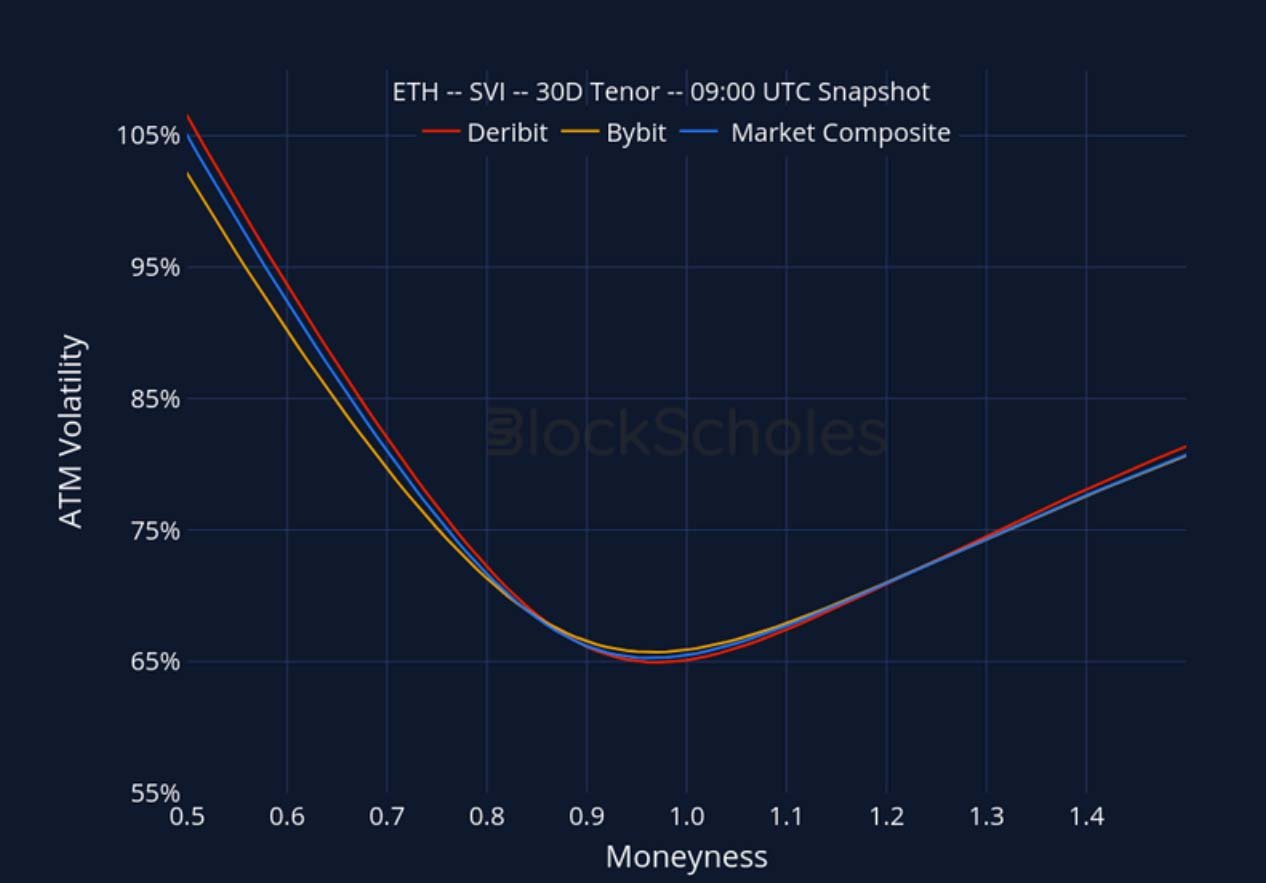

ETH SVI, 30D TENOR – 9:00 UTC Snapshot.

Constant Maturity Volatility Smiles

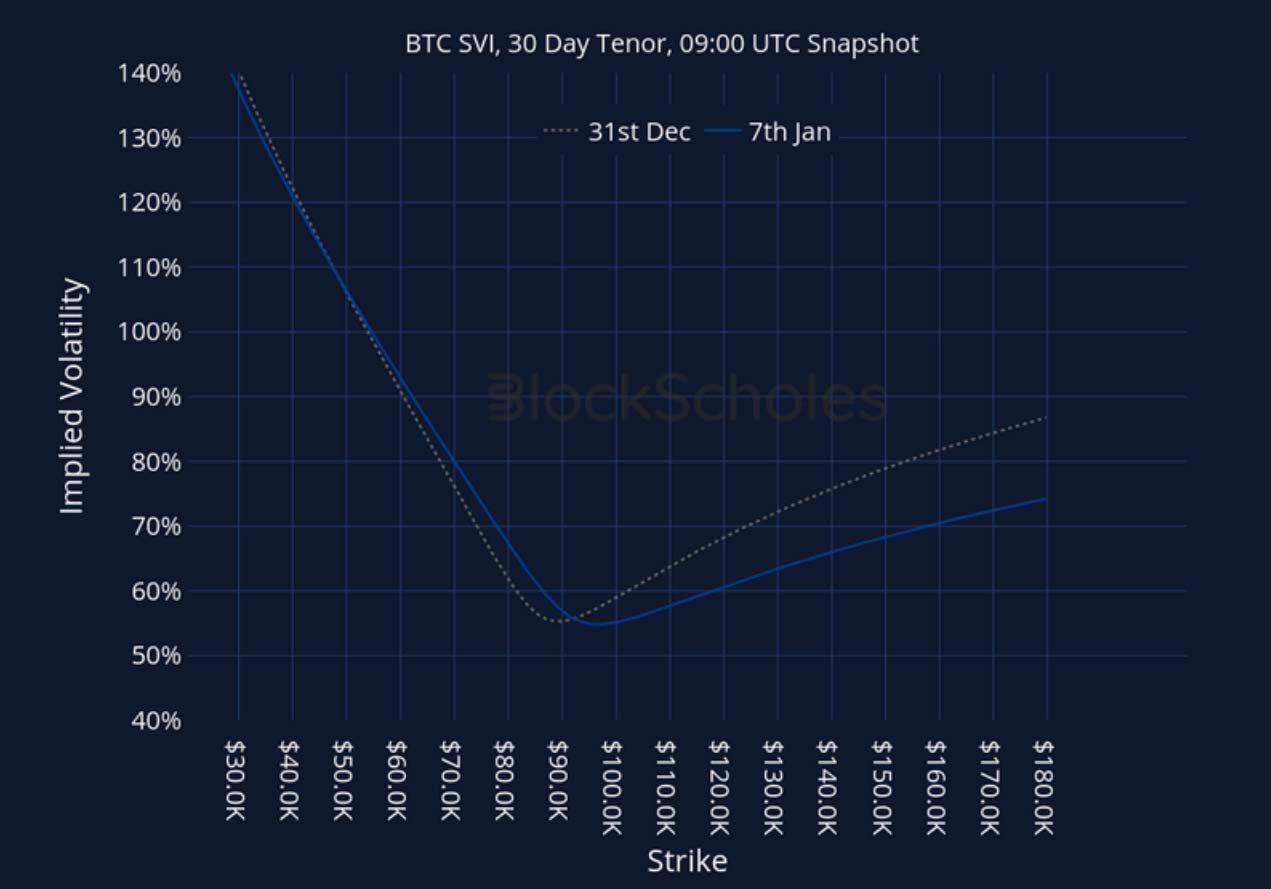

BTC SVI, 30D TENOR – 9:00 UTC Snapshot.

ETH SVI, 30D TENOR – 9:00 UTC Snapshot.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.