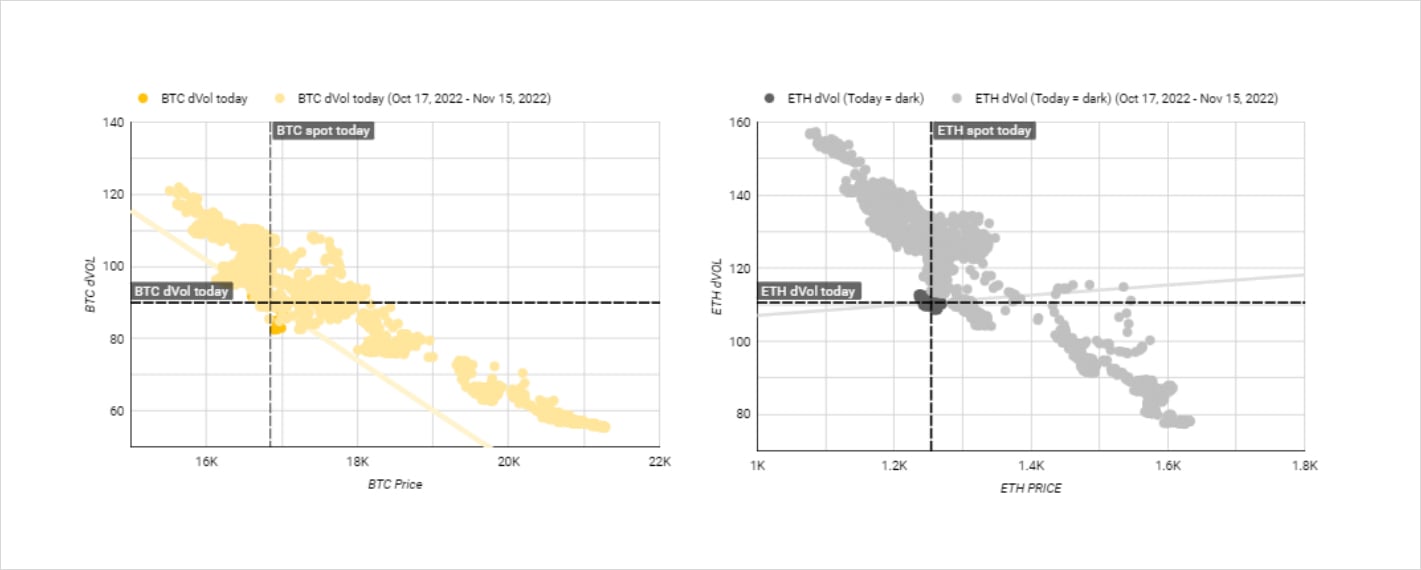

After an explosive week and a half with massive vol of vol, we are starting to see the first signs of softness in the crypto options volatility surface with dVol at the low end of range for current spot.

The repricing is a reflection of at-the-money vols and skew risk premium being priced out of the curve (dVol takes into account skew, see detail regarding methodology here, as well as spot honing into a 5% range in BTC and 8% range in ETH.

BTC and ETH dVol dSpot

Source: Deribit, Coinhako Research

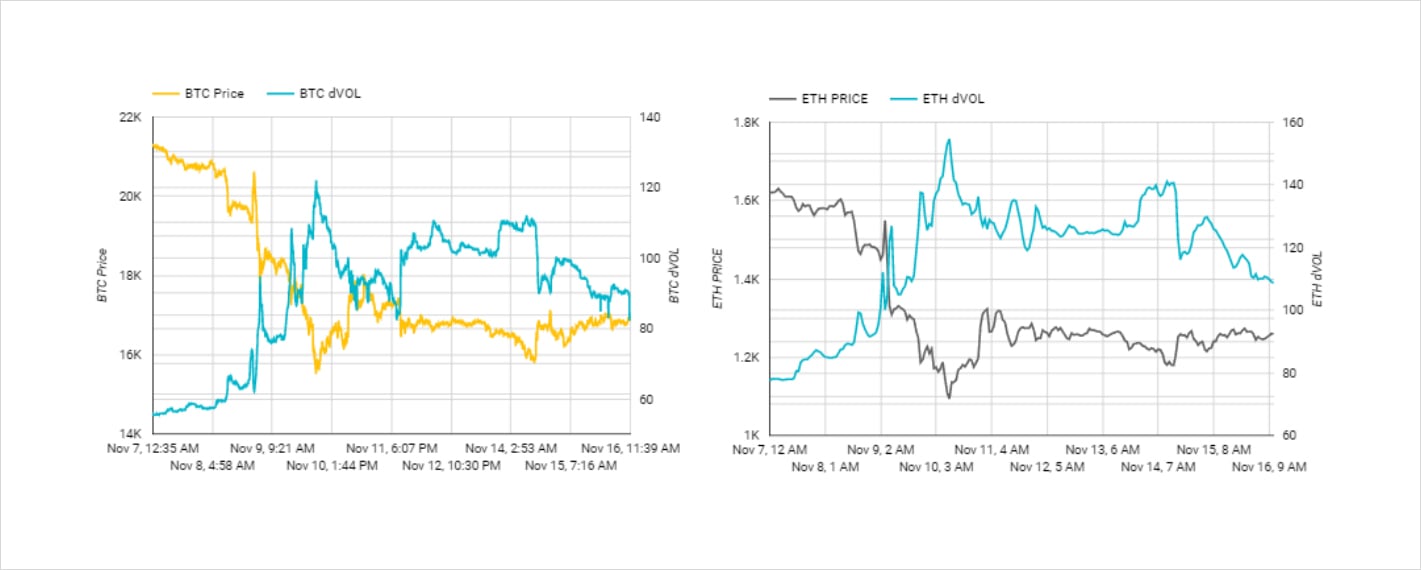

BTC and ETH dVol dTime

Source: Deribit, Coinhako Research

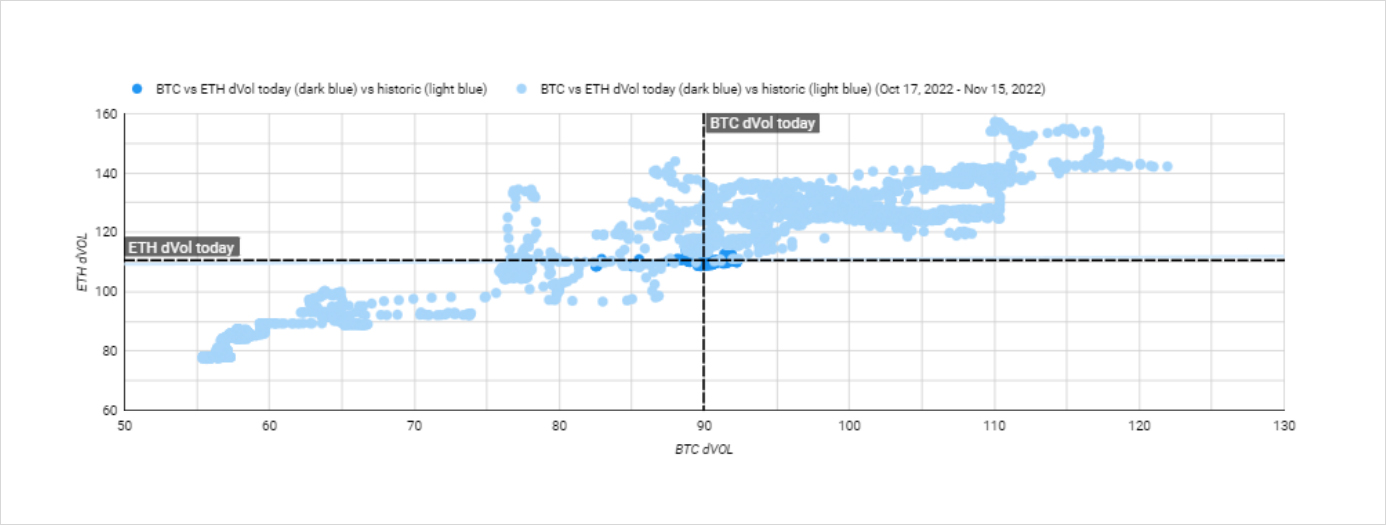

Another interesting development along the same lines is the ETH vs BTC dVol spread compressing back to the 20 vol level, where it has typically settled at post the ETH merge. This spread blew out to close to 60 vols as BTC skew and ATM vols lagged the ETH move.

BTC vs ETH dVol Spread

Source: Deribit, Coinhako Research

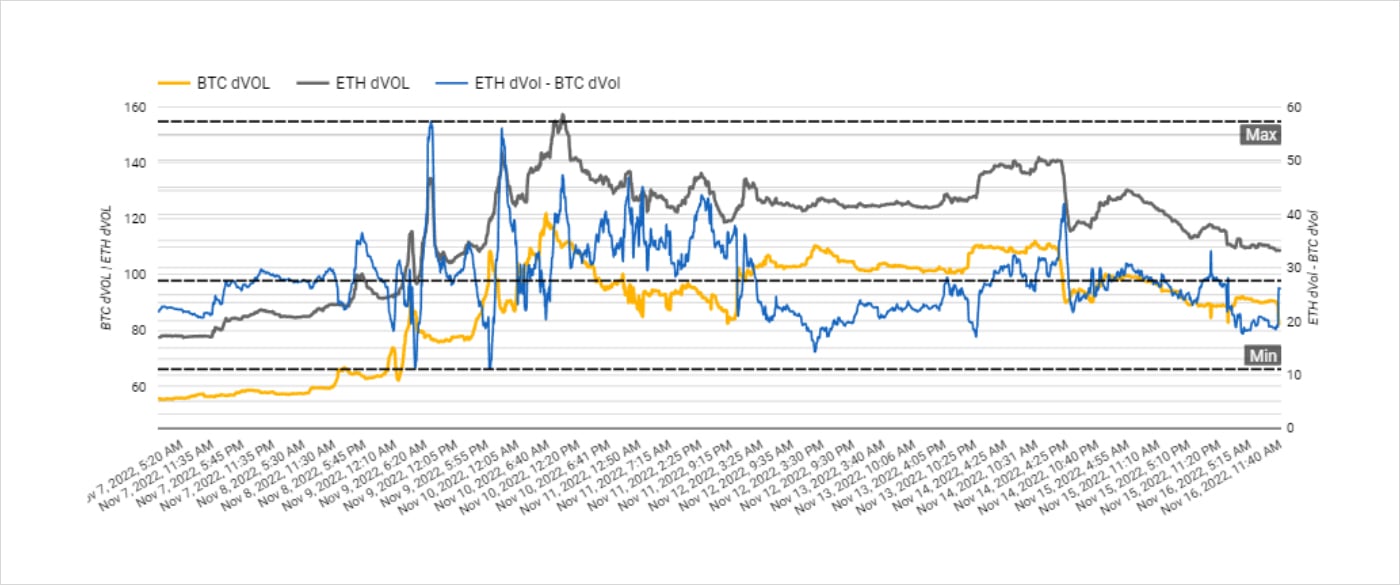

BTC vs ETH dVol Spread Timeline

Source: Deribit, Coinhako Research

With risk premium at the local lows since the FTX driven crisis began, the question is whether this is a dip to buy or a “yours” to catch the rest of the mean reversion in vols. The challenge in any sort of crypto back test is lack of data, fortunately 2022 has two past crises to give us an idea of how long it takes for the vol surface to normalize. The challenge with this particular crisis is it is the largest yet with the most contagion, so at a minimum the vol surface should remain elevated for at least as long as the past blow ups.

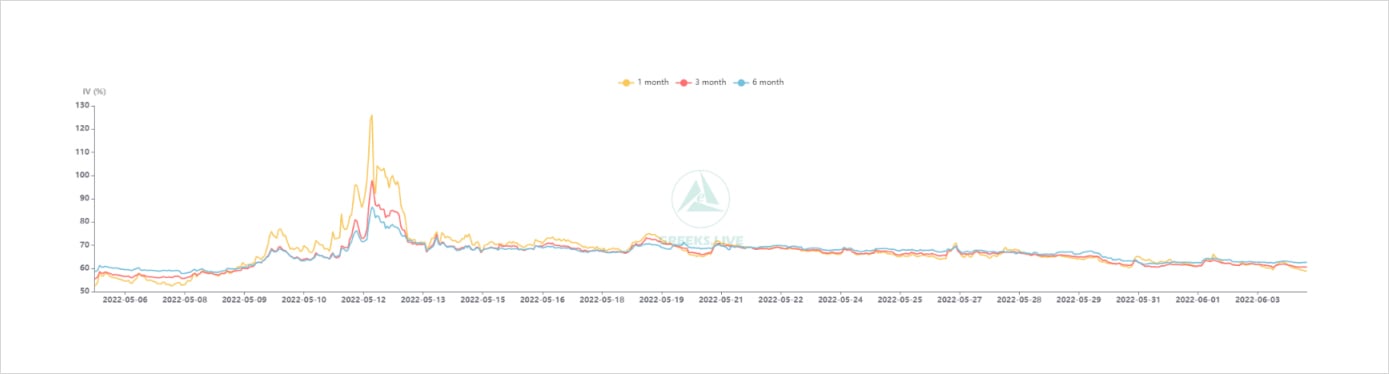

Looking back to Terra/Luna, the 1m ATM high was ~130 vols on May 12th with the curve reverting relatively quickly to the 70 1m IV level and trending lower minus a few minor pops.

BTC ATM IV – 8 May to 9 June

Source: Greeks.live, Deribit, Coinhako Research

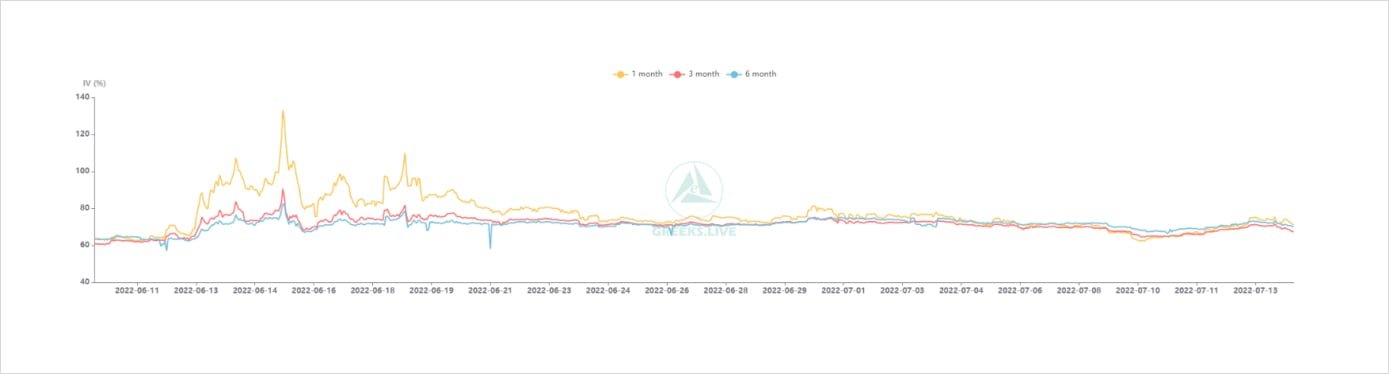

During the 3AC blow up, which in many ways is more similar to the FTX Alameda situation we find ourselves in but on a much smaller scale, the high in 1m vols was a similar ~130 vols reached on June 15th. In this case it was a much more prolonged period of high vol of vol with two spikes from a 70 1m IV to a 100 1m IV before settling nearly 10 days later.

BTC ATM IV – 10 June to 13 July

Source: Greeks.live, Deribit, Coinhako Research

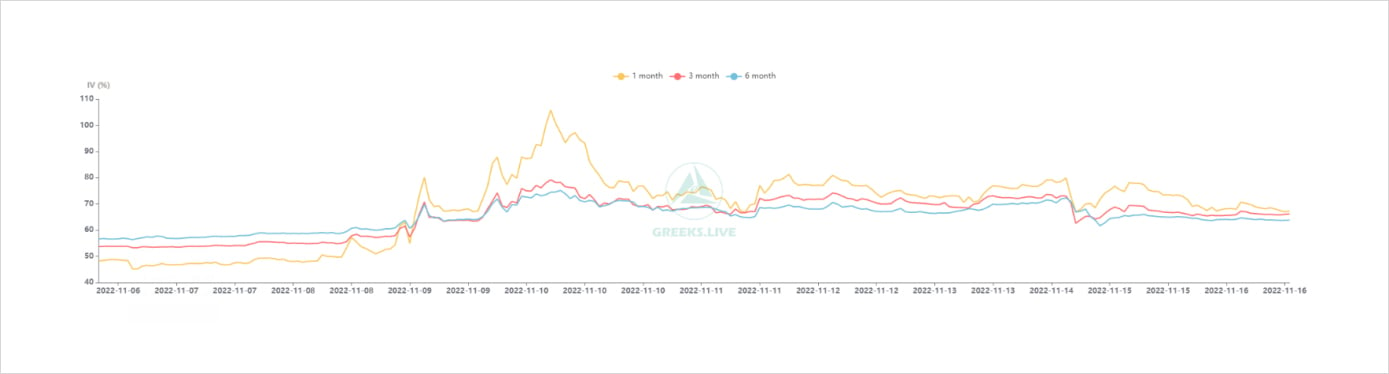

Looking at the FTX Alameda blowup and subsequent move in BTC IV, the 1m IV high peaked at a much lower level of 105 vols and we’ve seen two subsequent bounces from the 65 IV level to the 80 IV level in the 1 month tenor.

BTC ATM IV – 6 Nov to 16 Nov

Source: Greeks.live, Deribit, Coinhako Research

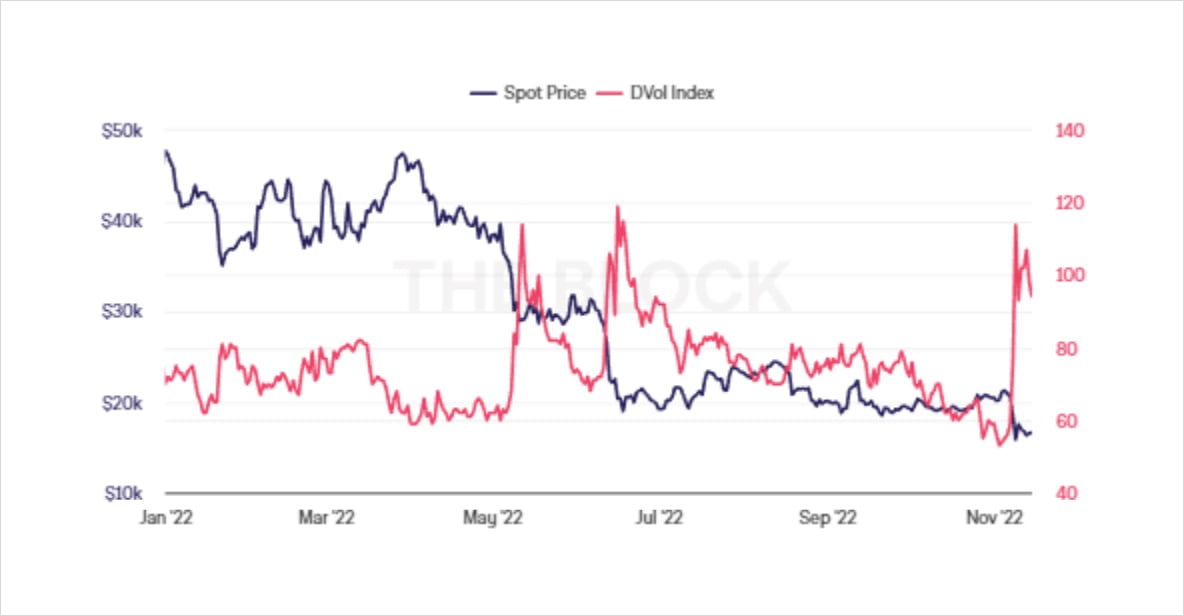

The above charts are at-the-money vols. If we look at dVol over the course of the year, the FTX Alameda spike looks more similar to the previous two crises, as the market has begun to price these risk events more in the skew than the ATM vols space which is logical given the nature of the spot price action over these events.

BTC dVol dSpot YtD

Source: The Block, AMBERDATA, Deribit, Coinhako Research

What becomes clear looking at the timeline of the previous blow ups is that this is very early in an event with much more contagion. Therefore the repricing in vols we’ve seen today with dVol going from 90 to 82 over the course of the session while 1 month ATM vols are back to a 65 IV we think is premature. This crisis isn’t existential to the crypto asset class and will pass, but it will take time so in the near term it would be prudent to buy vols on dips in the near term.

Disclaimer

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to Coinhako. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of Coinhako.