Affected by the imminent decision of the Federal Reserve in January and the tensions in Europe, the risk asset market experienced a large-scale pull back. The crypto market was the first to bear the brunt, and the market cap evaporated by more than $500b in 3 days.

The drop was mainly caused by spot selling, which did not lead to large-scale derivatives liquidation and exchange overload, which is relatively friendly to risk response. However, from the perspective of the derivatives market, the overall sentiment of investors in the crypto market has been hit hard.

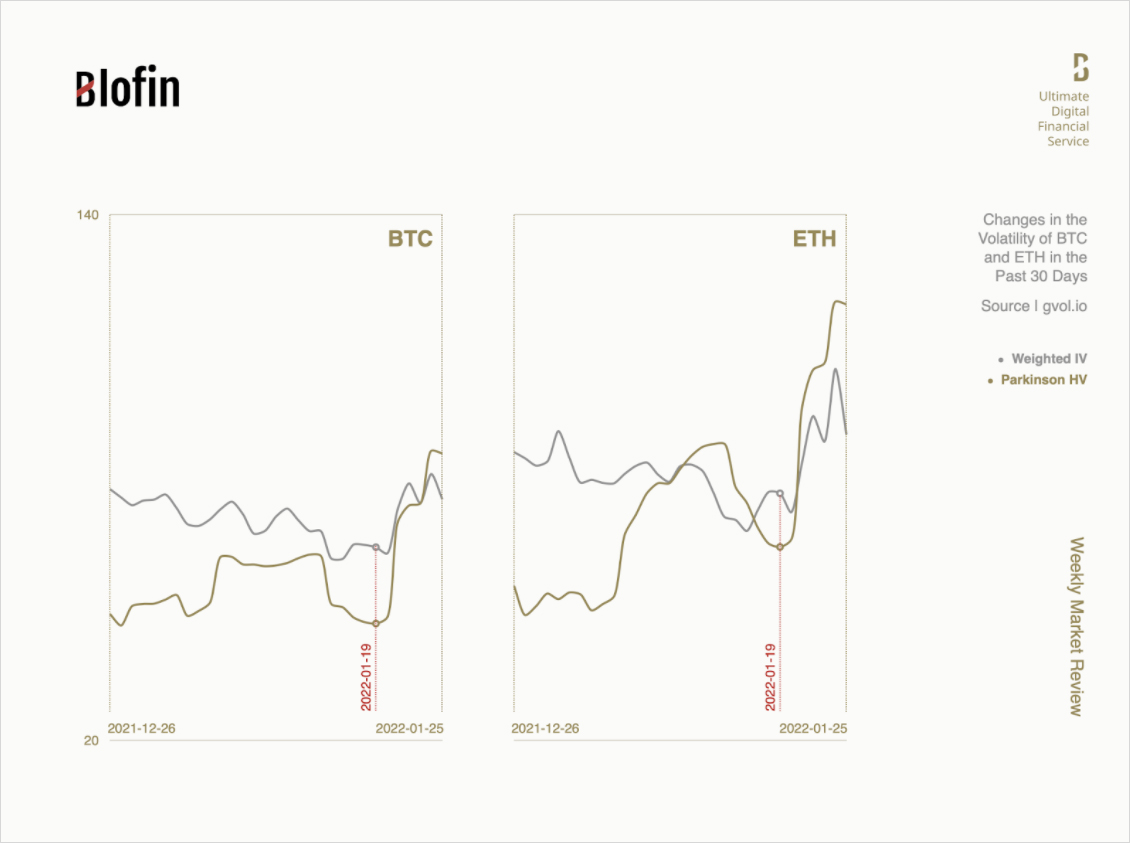

The volatility is likely to last longer than in December due to market volatility caused by spot sell-offs rather than derivatives market turmoil.

High Volatility “Finally” Coming

For the volatility bulls who had been in ambush 1-2 weeks early, they finally had the long-awaited moment. As the Fed’s silent period is coming to an end, since January 20, a large number of investors began to sell cryptos like blowouts, resulting in a large-scale decline in prices.

As of January 25, the prices of BTC and ETH fell by more than 20% and 30% respectively within 100 hours, of which BTC once erased almost the whole year’s gains. The market value of the entire market also shrunk from about $2t to $1.5t, more than a quarter.

Fortunately, as the spot selling dominated the slump, investors did not suffer the double shock of rapid price declines and exchange outages as they did in December. Most hedges were still available, and volatility did not rise as much as before. However, the large-scale purchase of safe-haven tools such as options has increased the open interest of futures and options contracts against the trend in some exchanges.

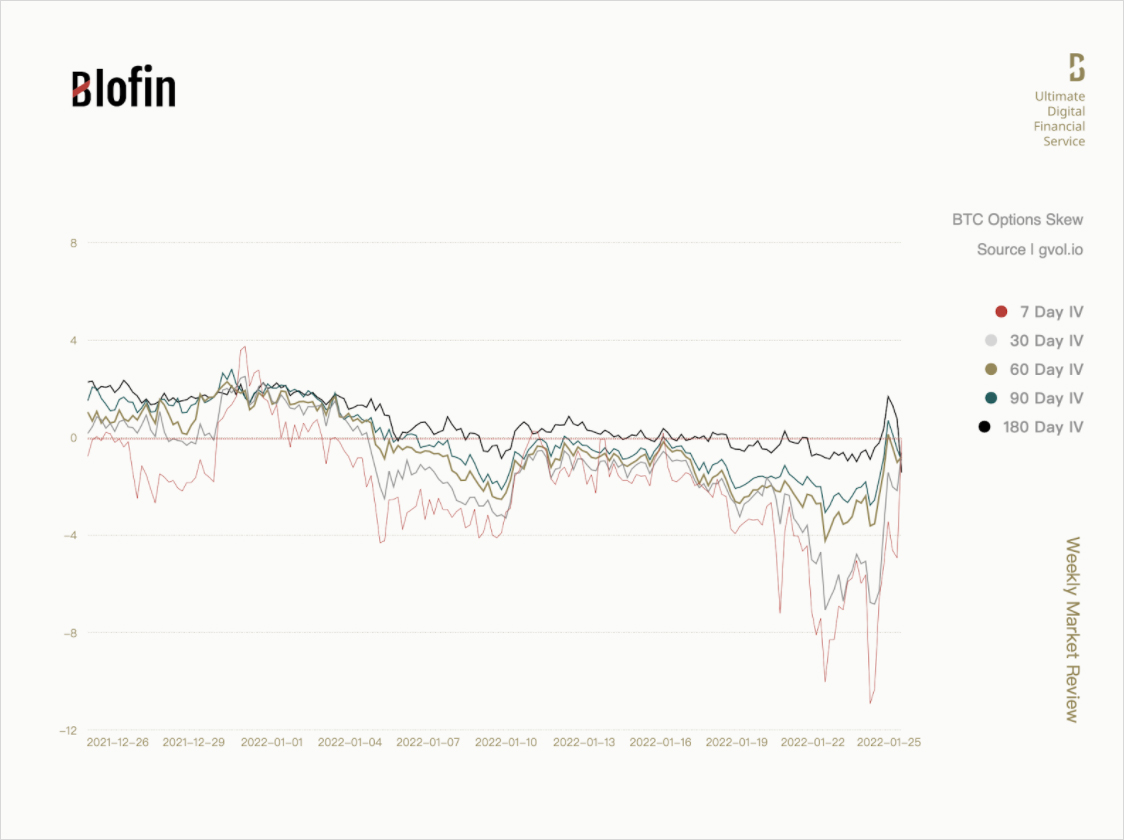

There has been a marked shift in market structure as investors’ safe-haven purchases concentrated in the bearish direction. As of January 25, the put/call ratio for BTC options has exceeded 1, while the put/call ratio for ETH options has also reached around 0.8. The skewness of options has also fallen sharply. The skew of short- and medium-term options has fallen to the lowest level in nearly half a year, the same as in July last year.

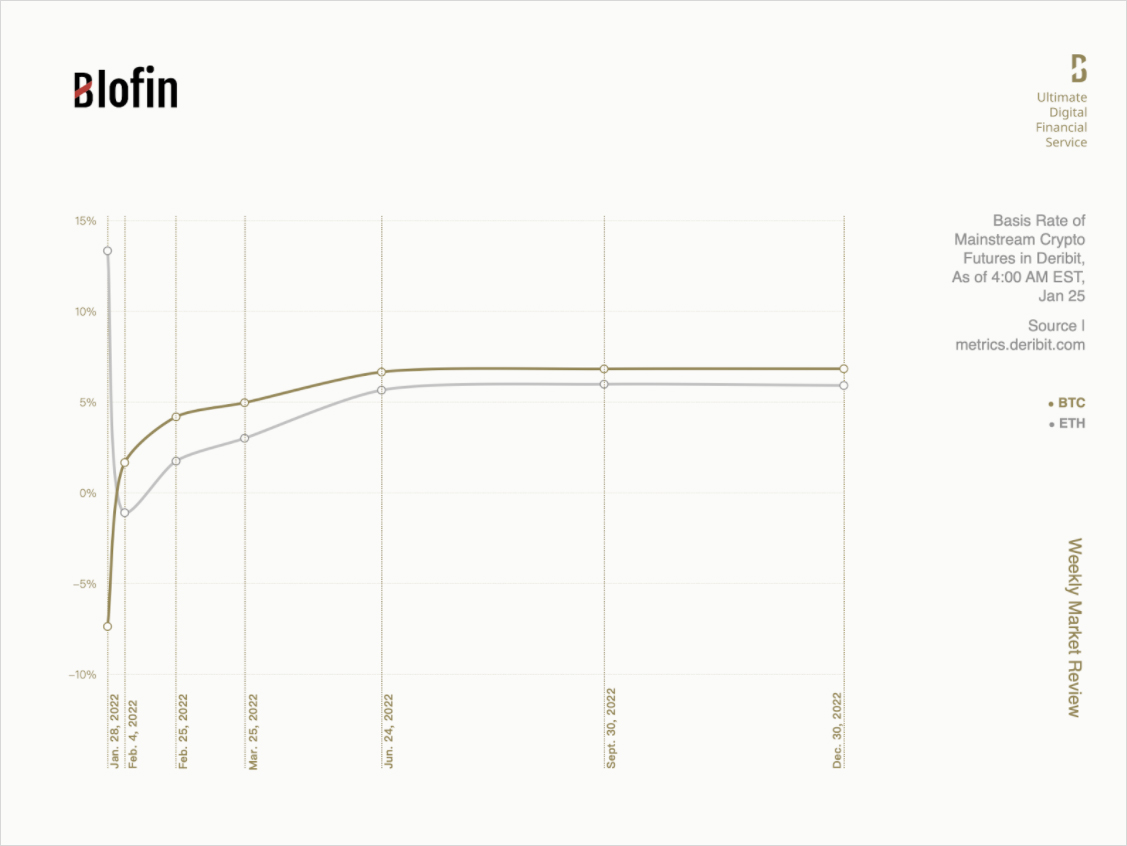

Affected by the massive selling pressure in the spot market, investors in the futures market have further lowered their expectations for future market performance. In the Deribit exchange, the BTC futures’ weekly premium fell below -5%, the forward futures premium fell to around 7%, and the overall curve moved down significantly compared to last week. For ETH futures, although the near-end of the premium curve has moved down relatively less compared to BTC futures, its forward futures premium has fallen below 6%, and the overall investor confidence is lacking.

Oversold, or Just the Beginning?

For now, the crypto market seems to have begun to recover slightly from the panic caused by the sell-off.

The initial tightening of liquidity in the capital market seems to have priced in: the interest rate market expects the Fed to eventually raise interest rates four times due to the slowdown in economic recovery and the US mid-term elections. Under the influence of high inflation pressure, the RBA may raise interest rates once in the middle of the year, and the European Central Bank will raise interest rates once at the end of the year. This information has already been reflected in risky asset markets.

However, the big unknown is what the Fed will conclude at its January meeting. Previous inferences on measures of tightening liquidity were mainly raising interest rates and stopping relatively moderate asset purchases. However, recent news has shown that the Fed may further adopt selling assets held to speed up the recovery of recovery liquidity. If the Fed hints that it will enter the market in person as a bear, it will have a more severe impact on the risk asset market, and the effect on secondary risk assets such as cryptos may be even more significant.

At the same time, investors also divided on the recent market trends. On the one hand, many individual investors are pessimistic: AAII Investor Sentiment Survey data shows that capital market pessimism has risen to the highest level since September 2020. However, many investors choose to buy dips at this time. They believe that the current crypto market is oversold, and the stock market’s poor performance may push the Federal Reserve to adopt relatively reasonable measures in January to reduce the impact on the capital market.

Given the rising uncertainty in the market, it is difficult to tell where asset prices will go in the future. Whether it is the beginning of a continuous decline or just a short-term oversold, before the Fed’s January interest rate decision officially landed, there is no doubt that a series of behaviors by investors due to different views will further push up the price change, which will drive volatility to continue to rise thereby. However, it is worth noting that the rise in market volatility this time is fundamentally different from that in December.

In December, market views did not change widely, so the volatility caused by the derivatives market was relatively short-lived. However, the volatility was mainly driven by the spot market this time. The high volatility caused by investors around the spot buying and selling is usually more persistent (Refer to the situation at the beginning of last year). Due to the maturity of the crypto market and changes in macro factors, it is difficult for volatility to rise to the same level as in early 2021.

This week, the Bank of Canada and the Federal Reserve will announce interest rate decisions one after another, and the crypto market is about to face the first large-scale shock since the New Year in 2022. The directional strategy is still not a more rational choice in the short term. Considering the likely dovish attitude of the Fed, it seems more appropriate to maintain some short-term exposure to gamma and vega. While gaining volatility gains, investors can also obtain additional gains through methods such as gamma scalping.