Last week the market had a plethora of events to digest, amongst those being the FOMC decision on rates (and subsequent meeting minutes), big tech earnings from companies like Apple, Google, and Amazon, and the unexpected results from the NFP data.

The recent rally that had started in the middle of January had been relatively BTC dominant, with outsized gains in BTC and a noticeable lag in price action seen in the altcoins and ETH. Call skew had been pronounced in BTC while ETH skew did not express the same elevated premium noticed in the BTC options market. Interestingly, after seemingly hitting a bottom, the ETH/BTC ratio had shown a moderate reversal toward the upside during the latter part of the week as we saw a rally in ETH and a variety of alts.

The weekend brought a steady deterioration in both volume and price action compared to weekends of the past. The Asian market opened with a slight reversal in the declining price as a small rally up from lows of ~$22,750 and ~$1,600 started to materialize.

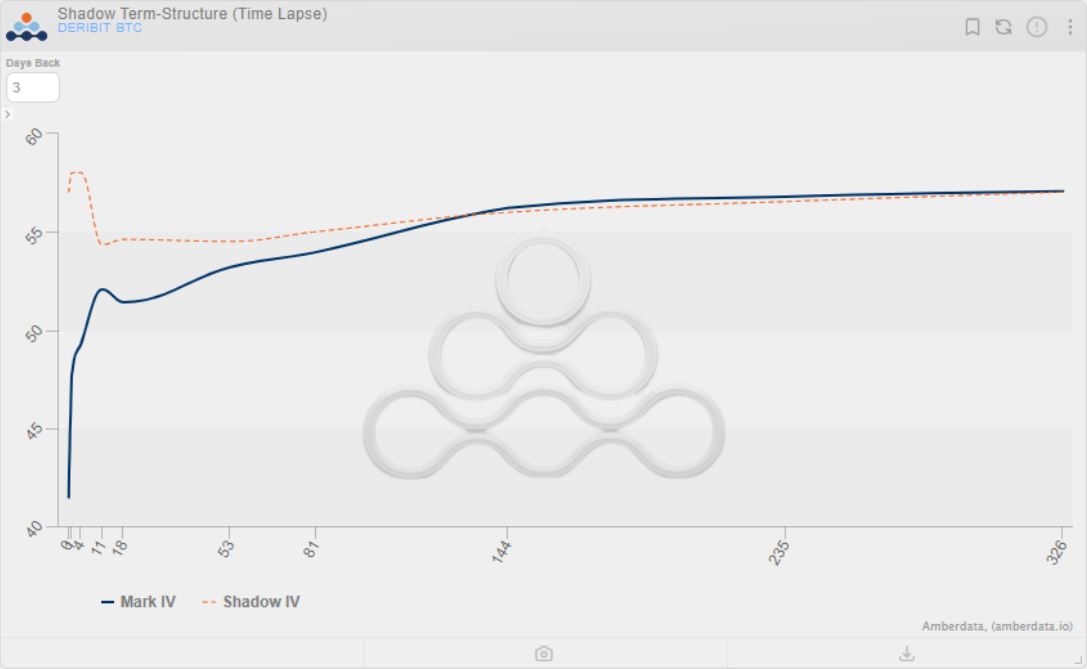

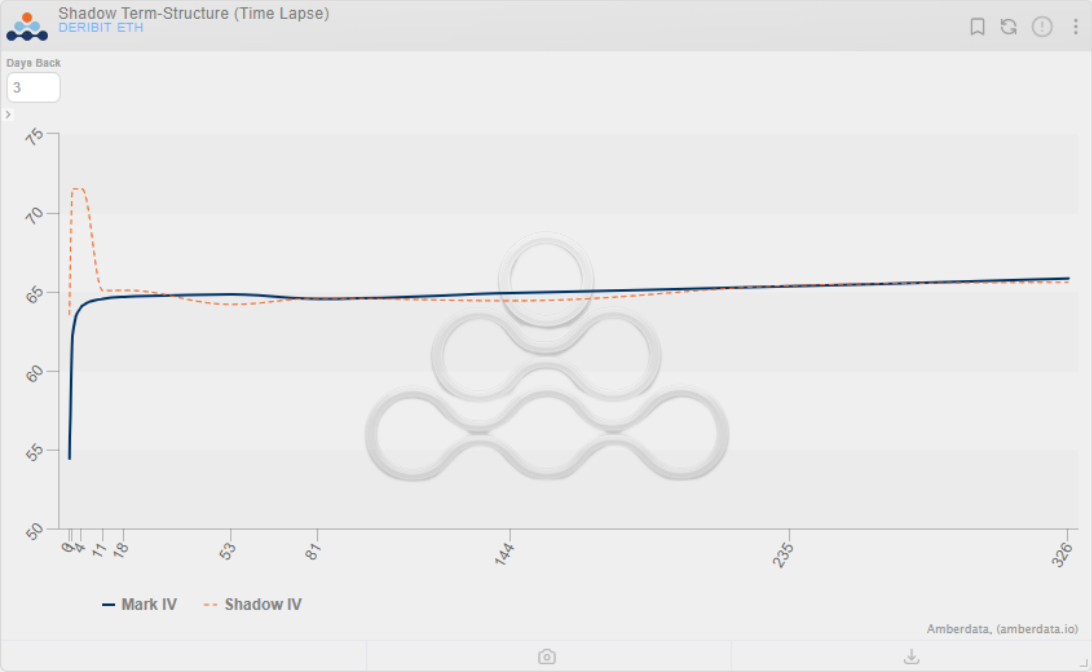

Term Structure for BTC and ETH

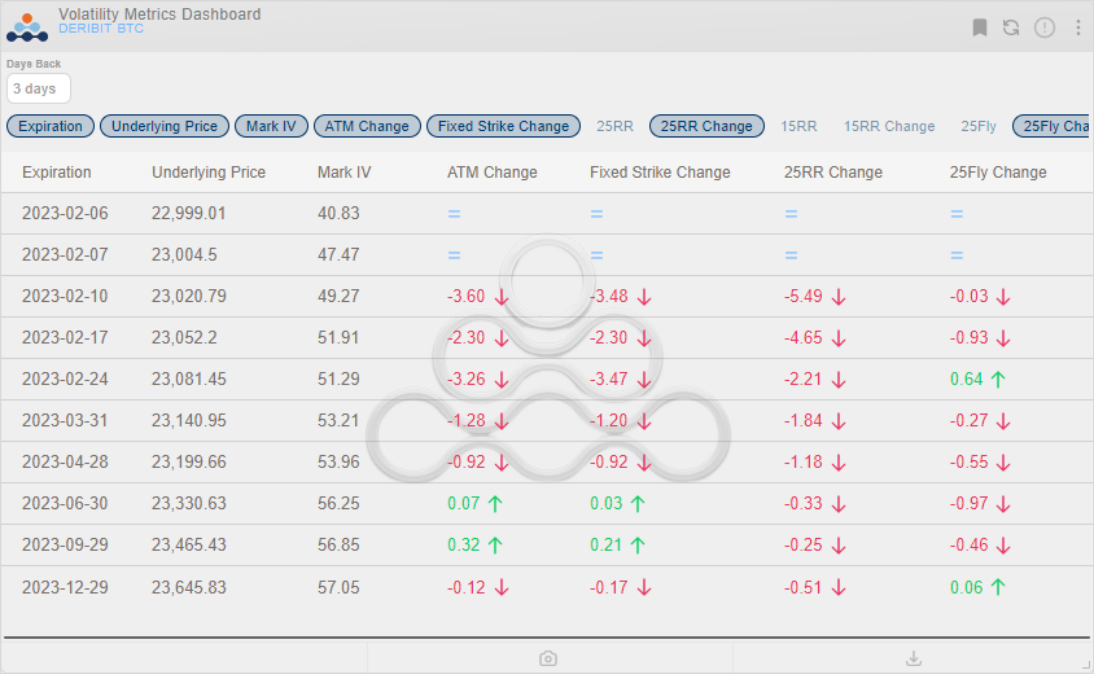

As the market has taken time to comprehend the events of last week and price continues to consolidate in the current range, implied vols in the front end of the curve have waned and longer dated term structure has stayed relatively sticky. ATM strikes in the February 24 th expiry have fallen around 3 vols to a mark IV of 51.4 while longer dated tenors such as the June 30 th and September 29 th expiries saw a very slight increase of around 0.15-0.25 points with mark IV’s of 56.2 and 56.8 respectively

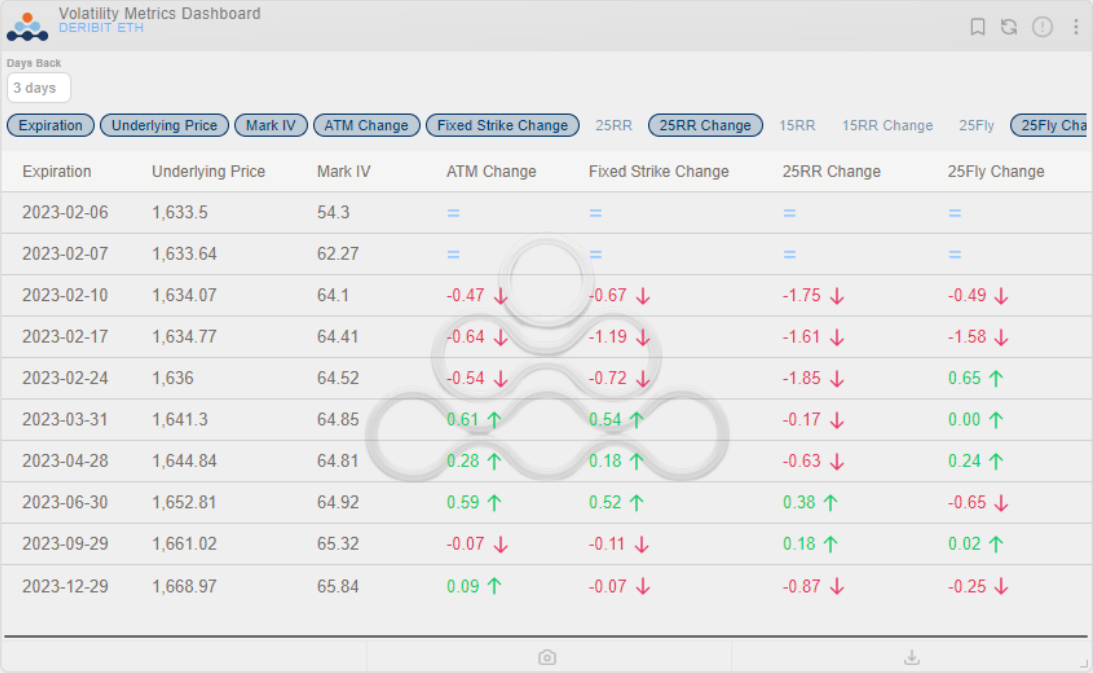

In ETH, a very flat term structure has taken shape as both longer-dated expiries and short-dated tenors trade relatively flat. This flat term structure seen throughout the curve may have something to do with the short-dated outright vol buyers across a wide range of strikes, with outright call purchases being popular over the past two days.

Skew for BTC and ETH

BTC now shows monthly and weekly expiry skew reverting back to the previously typical “puts at a premium”. After Wednesday we saw the slow deterioration of the longer-dated skew approaching a similar reversion, but these tenors still trade with a very slight premium favoring the 25 delta calls. Skew as measured by the 25RR in for the February 10 th expiry saw almost a 5.5 IV decline as the short-dated demand for upside gamma was not met with the same rigor as seen in ETH flows.

ETH skew still trades persistently in the negatives as OTM 25 delta puts command a premium across all tenors. While skew in a variety of the tenors has stayed relatively flat during the week, the main decay was seen during the latter of Saturday’s trading session with weekly skew shifting down approximately 4 IVs. ETH played catch-up during the week as seen in the ETH/BTC ratio’s rally. Volatility across all tenors stayed relatively sticky at the current levels as the battle between short-term speculators and rally skeptics continues.

Liquidations and OI

Longs toward the end of the week, specifically Sunday, were under fire as ETH looked to test $1,600 and BTC approached $22,750. As anticipation of a sharp rally has cooled off, and BTC short-term skew has signaled a faltering pursuit of upside speculation, Sunday saw a steady flow of shorts entering the market after the failure to hold $23,000 support.

This conclusion is made as I’ve seen an increase in aggregated open interest while CVD in BTC stays relatively flat. This can be interpreted in multiple ways, whether that be the potential for future short liquidations were we to break toward the upside, or also could be viewed as a bearish trade with shorts rushing to open positions during this expressed weakness.

Noticeable Flows Throughout the Week

Trades done on Deribit screens saw a prevalent demand of short-dated topside across a wide variety of strikes, all out of the money currently, with the 27K strike calls being the most ambitious. Blocks of BTC options executed through Paradigm saw some longer-dated upside speculation take place as outright 32K calls expiring March 31 st were purchased, along with a few 25/30K debit spreads.

For more detailed insight into block trades executed through Paradigm, take a look at their recent tweet.

A Look Ahead

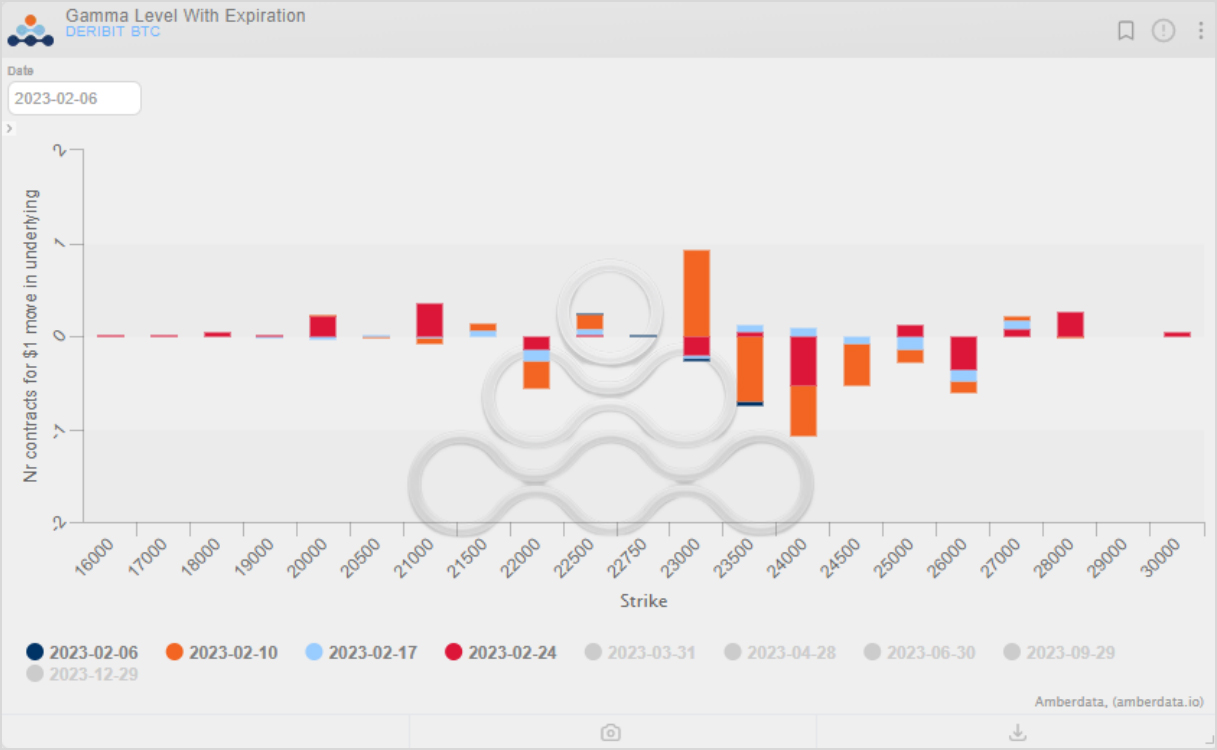

I’ve noted ETH’s relatively flat term structure, potential short positions opened on Sunday, reversals in the upside skew bias seen in BTC, and a few interesting block trades heading into the upcoming week. As seen in some of the speculated dealer gamma positioning charted by AmberData, $23,000 is likely to act as a magnet this week until this upcoming weekly expiry rolls off or we see some organic buyer flows start to trickle back into the markets. Additionally, keeping an eye on the ETH/BTC ratio and any strength in some of the altcoins is important as well.

AUTHOR(S)

Chris Newhouse is an OTC Trader at GSR, a crypto native market-maker that specializes in providing liquidity across spot and derivatives markets.