Following the news of the SEC’s intent to sue Paxos for their selling of unregistered securities, BUSD’s market value briefly de-pegged from its $1 face value.

Evidence for this was seen onchain in the increased supply of BUSD in decentralised exchanges and in a flow of BUSD redemptions directly with its issuer. However, the market appears to have stabilised, having digested that there is not yet reason to believe that Paxos will fail to honour redemptions. This event, however, may hold implications for other stablecoins with similar reservebacked peg mechanisms.

SEC Wells Notice

- Paxos Trust Company controls the minting and redemption of Binance’s native stablecoin, BUSD.

- Earlier this week, the SEC notified Paxos of their intent to sue, claiming that their issuance of BUSD constitutes the unregistered sales of a security.

- As a result, Paxos have halted the issuance of new BUSD tokens, but will continue to process redemptions of existing BUSD supply.

- Note that Paxos is a distinct legal entity company to Binance, who are not being sued by the SEC.

- The decision follows a similar notice served to Kraken, whose staking-as-a-service program was similarly targeted by the SEC’s claims of unregistered securities trading.

Traders Offload BUSD

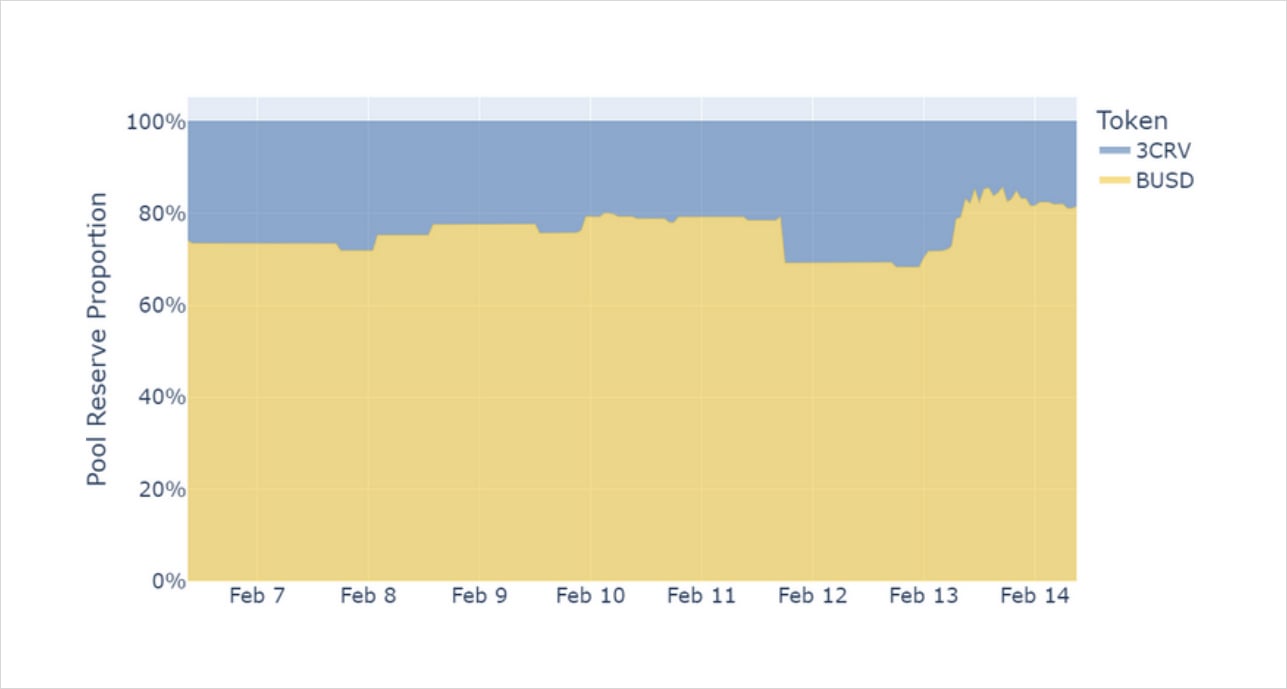

Figure 1 Hourly proportion of 3CRV (pale blue) and BUSD (pale yellow) tokens in the BUSD3CRV Curve Finance pool. Source: Block Scholes

- In the hours following the SEC’s announcement, BUSD was swapped for other stablecoin tokens, such as USDC or USDT.

- That selling caused a brief but significant depeg in the tokens value against the dollar, before recovering to near $0.9999 at the time of writing.

- This is evidenced by Figure 1, which shows the composition of the BUSD/3CRV pool on Curve Finance’s DEX platform.

- This protocol allows users to swap crypto-currency tokens in a decentralised manner, with the price determined by the ratio of assets in the pool.

- The chart shows a significant increase in the proportion of BUSD in the pool during the early hours of Feb 13th as the SEC announced their decision.

- An increase in BUSD in the pool indicates that their was an excess of traders eager to sell BUSD to the protocol and buy 3CRV (a token that “averages” the price of three other major stablecoins USDC, USDT, and DAI) from it.

- However, that selling stabilised soon after as other traders were willing to buy BUSD below its pegprice of $1.

Will this lead to a Depeg?

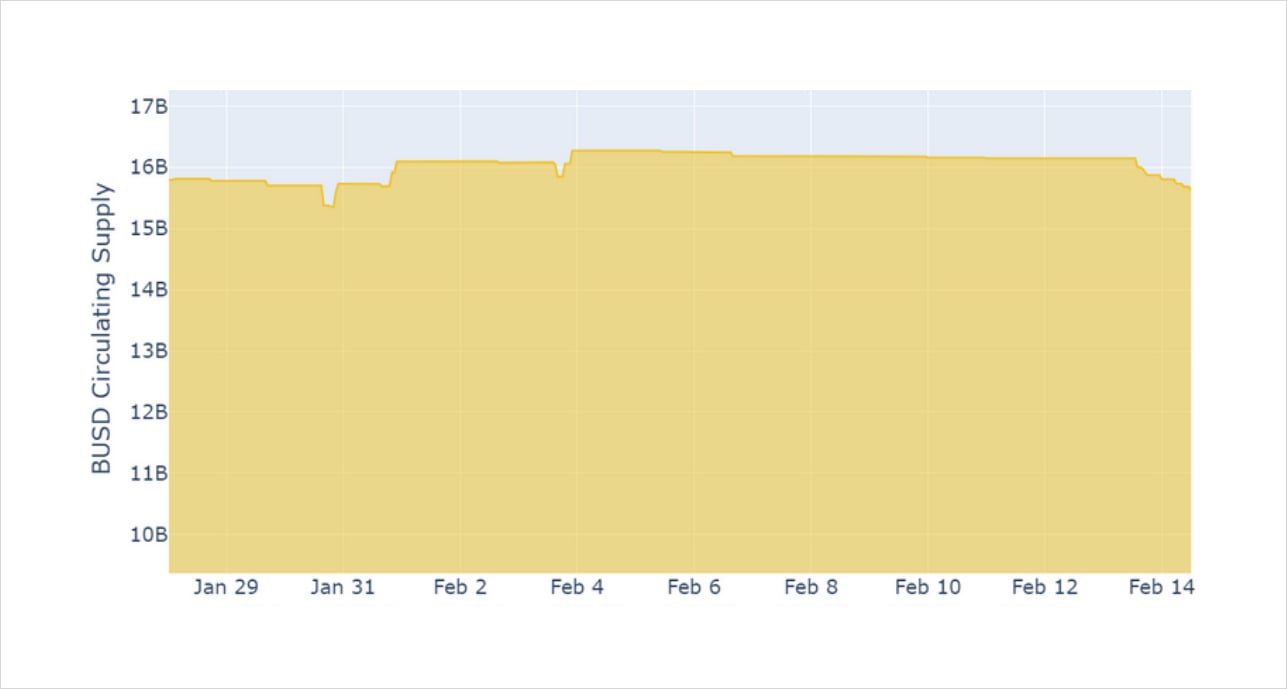

Figure 2 Hourly circulating supply of BUSD on the Ethereum mainnet since 28th Jan 23. Note that the y axis begins at 10B tokens of BUSD Supply. Source: Block Scholes

- The small flow out of BUSD was also visible in direct redemptions of BUSD with Paxos.

- Figure 2 shows the circulating supply of BUSD, along with its downturn beginning on the 13th Feb.

- Onchain BUSD supply will continue to decrease monotonically as users continue to redeem outstanding tokens without new issuance.

- The relatively small amount redeemed over the past few days indicates that traders are not too concerned about their ability to reclaim fiat currency.

- This is understandable to us. The indictment by the SEC does not directly concern the health of Paxos’s reserve balance: they have not failed to meet redemption obligations, but have merely failed to prove their ability to do so to the SEC.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.