Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

Implied volatility remains low, with ETH’s the lower of the two majors. We observe a divergence in the sentiment expressed in the delta-one markets of both assets, with BTC future implied yields and perpetual swap funding rates strongly positive whilst ETH’s venture further negative. However, the trends in their volatility smile have both been towards a more neutral pricing, having both expressed a higher implied volatility for OTM puts than calls over the past month.

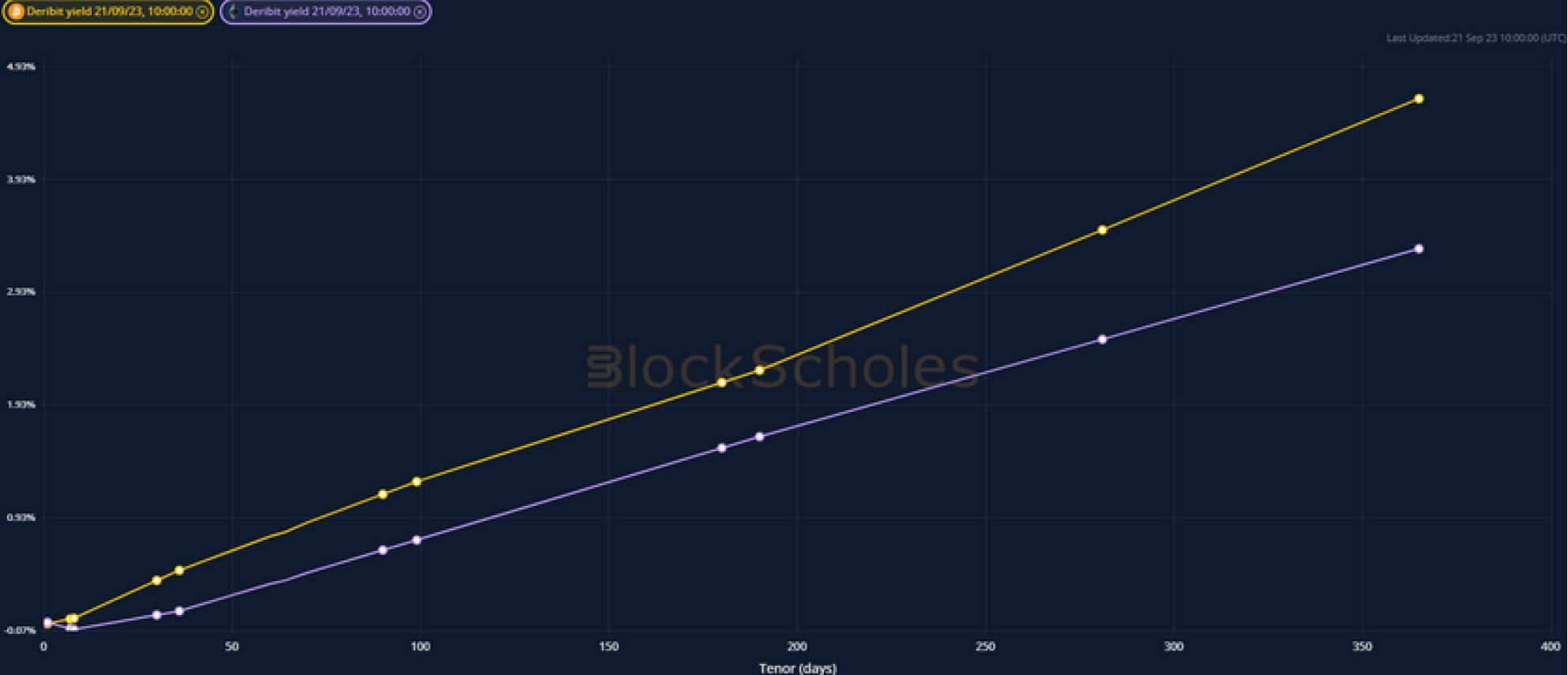

Futures implied yield term structure.

Volatility Surface Metrics.

*All data in tables recorded at a 10:00 UTC snapshot unless otherwise stated.

Futures

BTC ANNUALISED YIELDS – futures trade 2% above spot at an annualised rate for all tenors, as they have consistently over the last month.

ETH ANNUALISED YIELDS – have continued a significant and decisive trend below zero at a 1 week tenor.

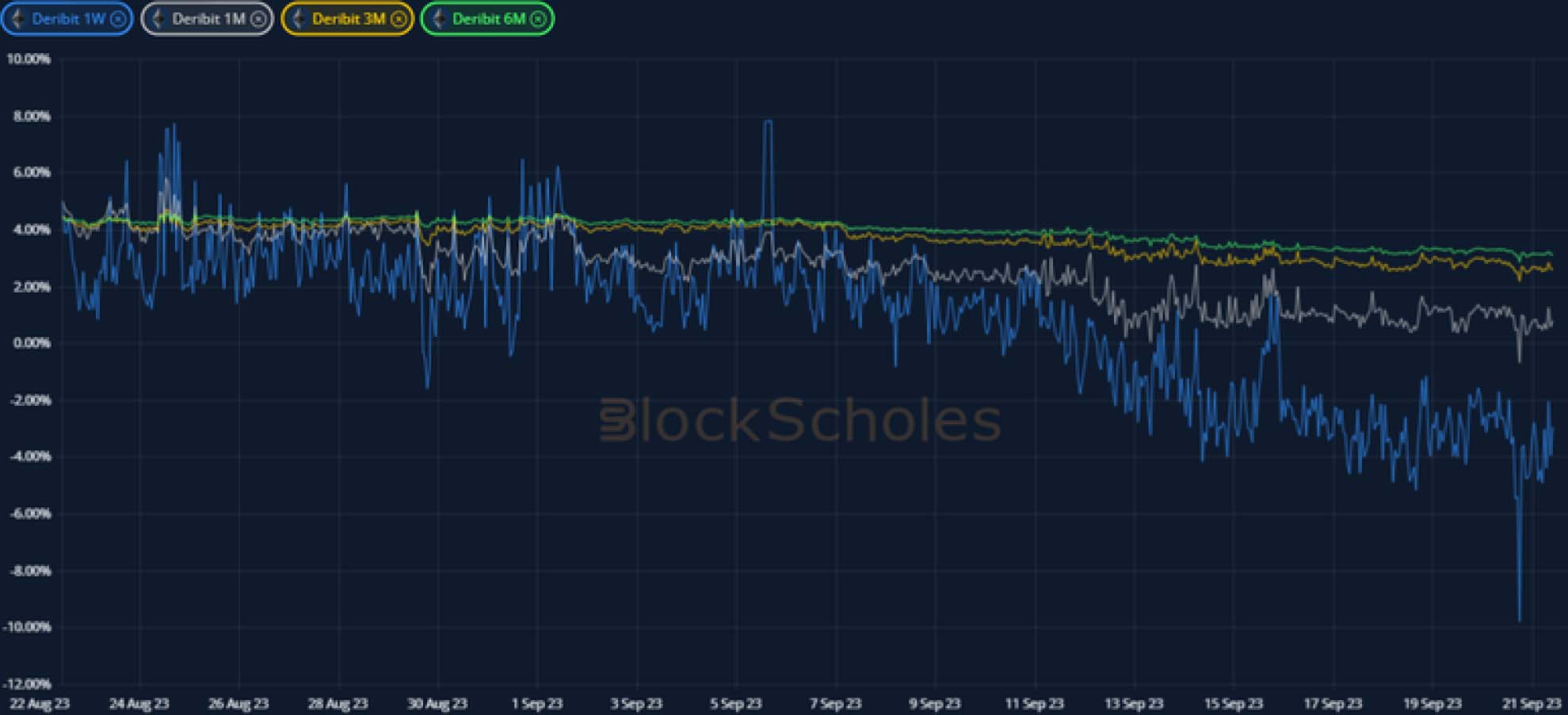

Perpetual Swap Funding Rate

BTC FUNDING RATE – has been consistently positive over the past two weeks, but still much lower than the levels we saw in early August.

ETH FUNDING RATE – has traded negative over the past week in contrast to BTC’s and expresses a similar demand for short exposure to its futures.

BTC Options

BTC SABR ATM IMPLIED VOLATILITY – has risen slightly at longer dated tenors, widening the spread to the 1 week tenor to nearly 20 points.

BTC 25-Delta Risk Reversal – is strongly in favour of calls at a 6 month tenor, whilst short dated options express a slight tilt towards OTM puts.

ETH Options

ETH SABR ATM IMPLIED VOLATILITY – trades in a wide spread across the term structure, between 25% and 45% – noticeably lower than BTC’s vol.

ETH 25-Delta Risk Reversal – has trended towards a more neutral vol smile, with shorter tenors expressing a slightly stronger tilt towards puts.

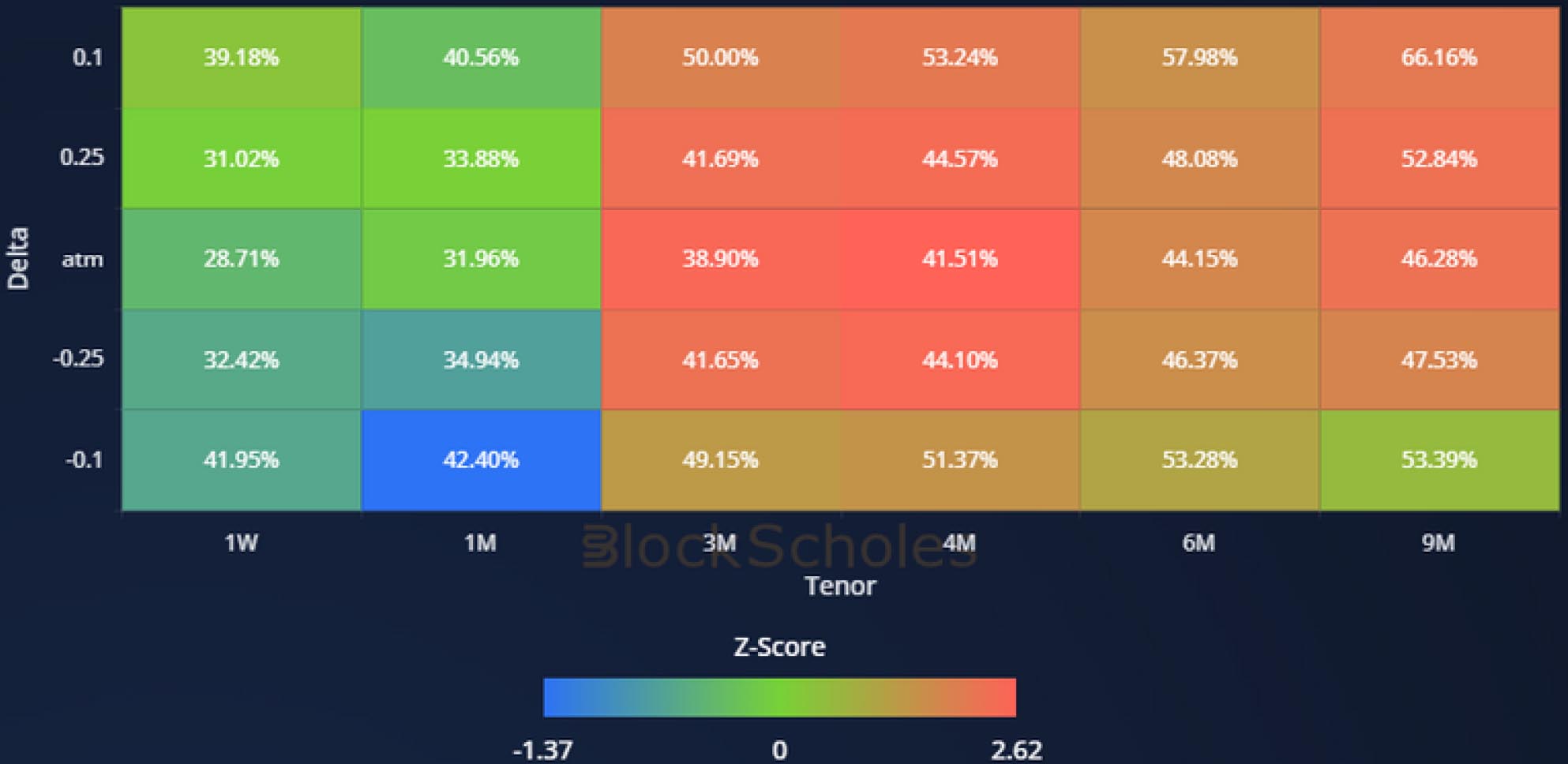

Volatility Surface

BTC IMPLIED VOL SURFACE – longer dated OTM calls have outperformed their recent history the strongest, with a pickup in implied vol across the surface.

ETH IMPLIED VOL SURFACE – shorter dated vols have not risen as much as smiles at 3M and 4M tenors, whilst 1M OTM puts report a fall in vols.

Z-Score calculated with respect to the distribution of implied volatility of an option at a given delta and tenor over the previous 30-days of hourly data, timestamp 10:00 UTC, SABR smile calibration.

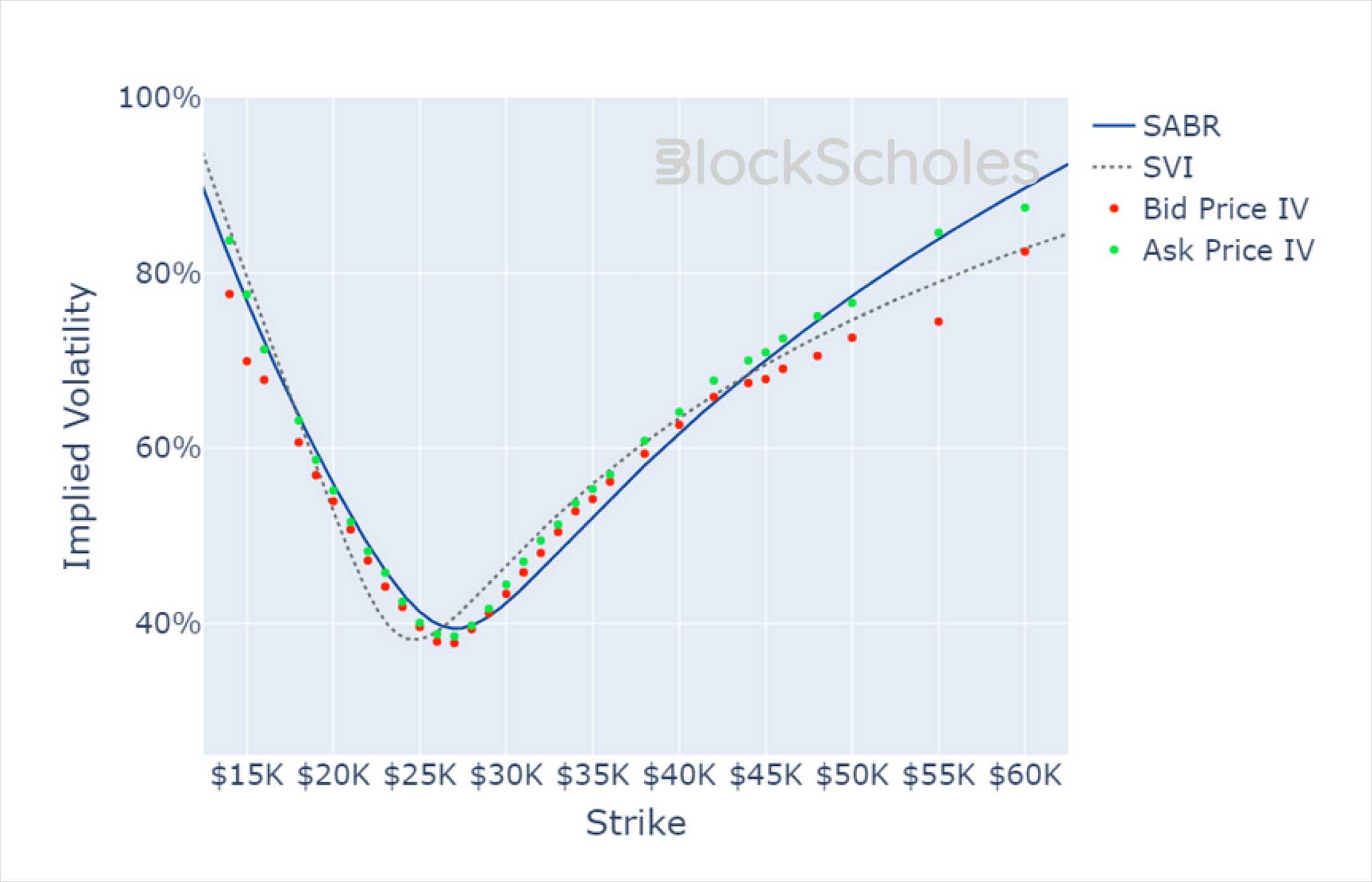

Volatility Smiles

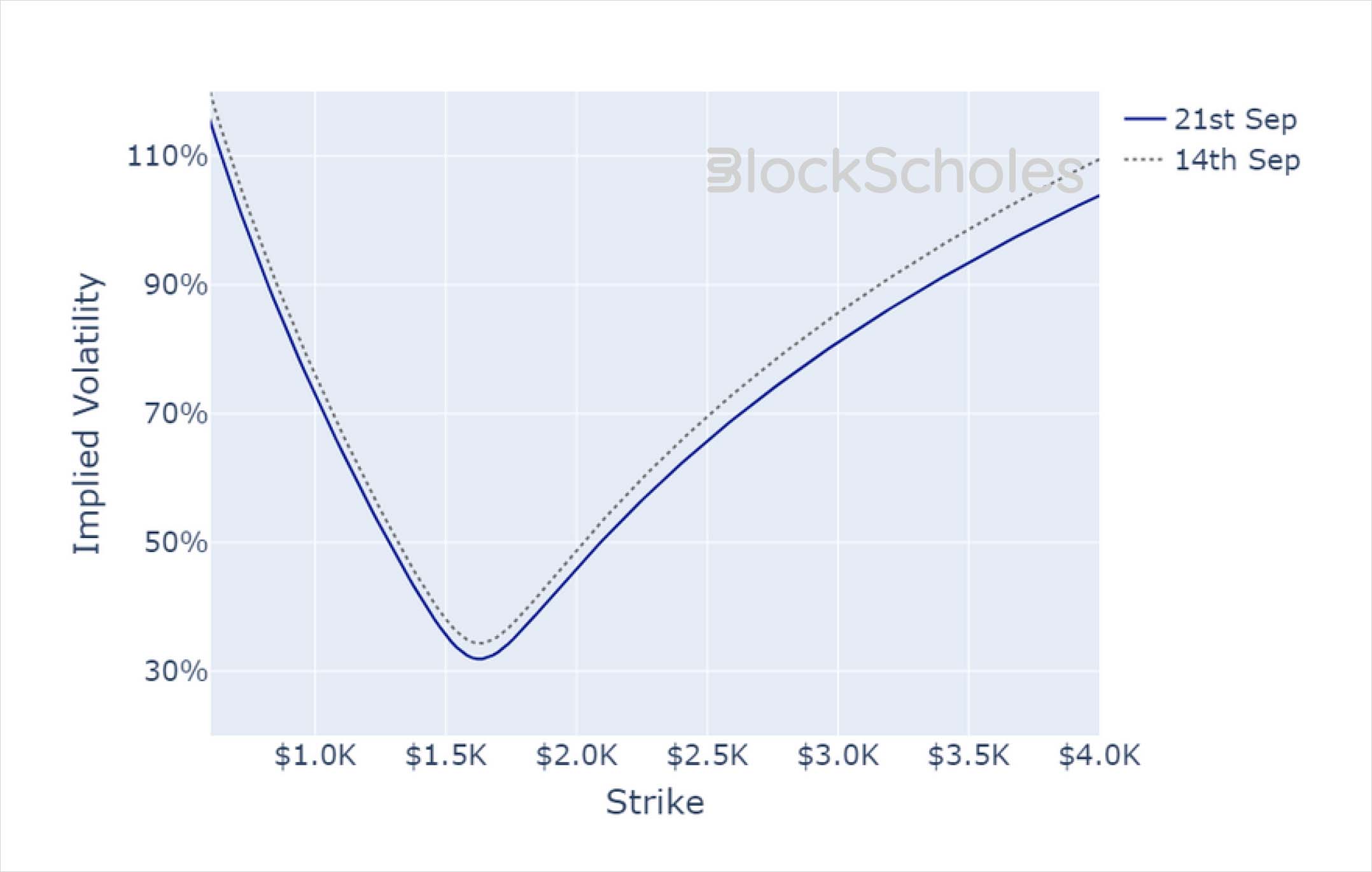

BTC SMILE CALIBRATIONS – 27 – Oct-2023 Expiry, 10:00 UTC Snapshot.

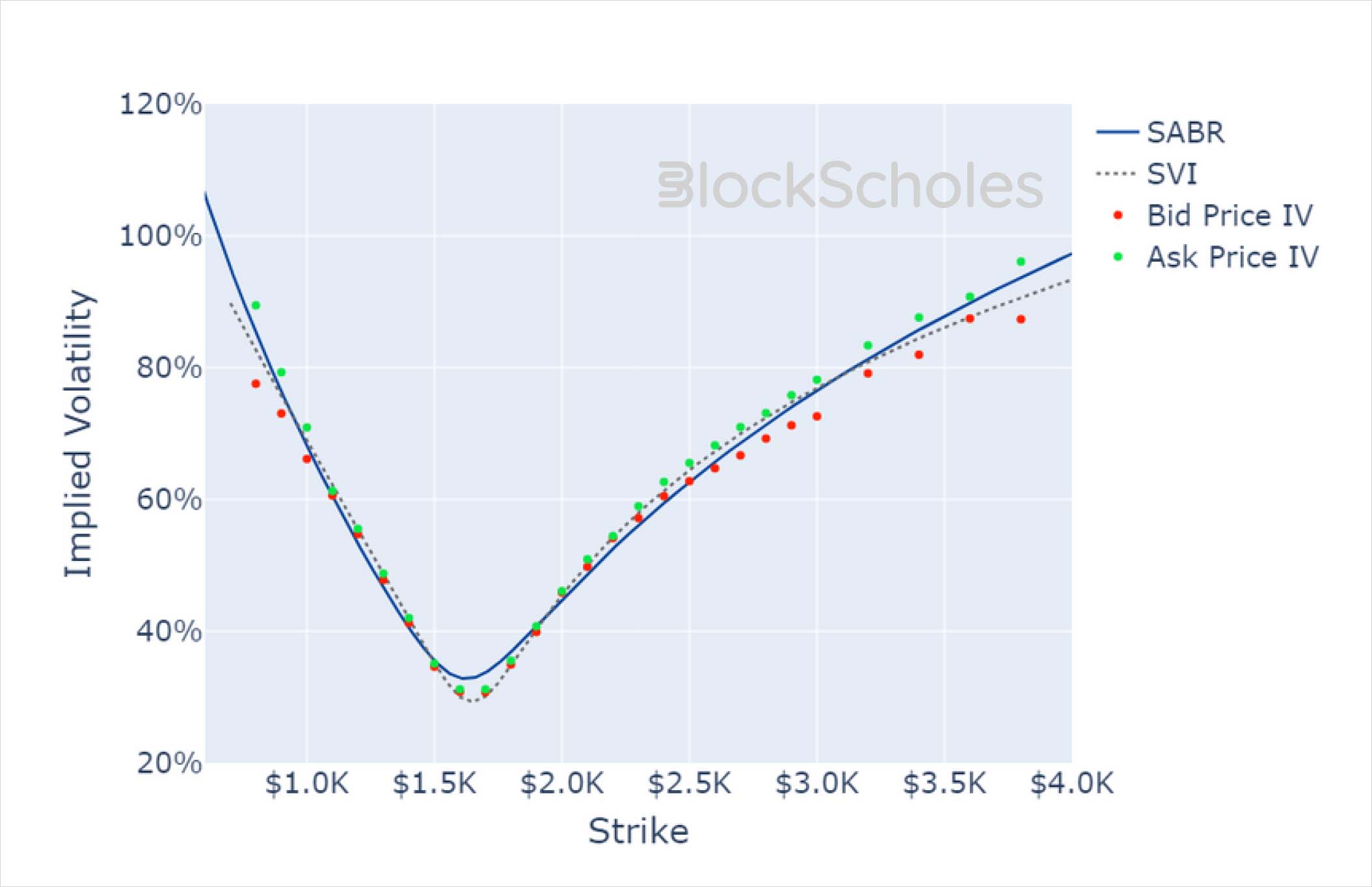

ETH SMILE CALIBRATIONS – 27 – Oct-2023 Expiry, 10:00 UTC Snapshot.

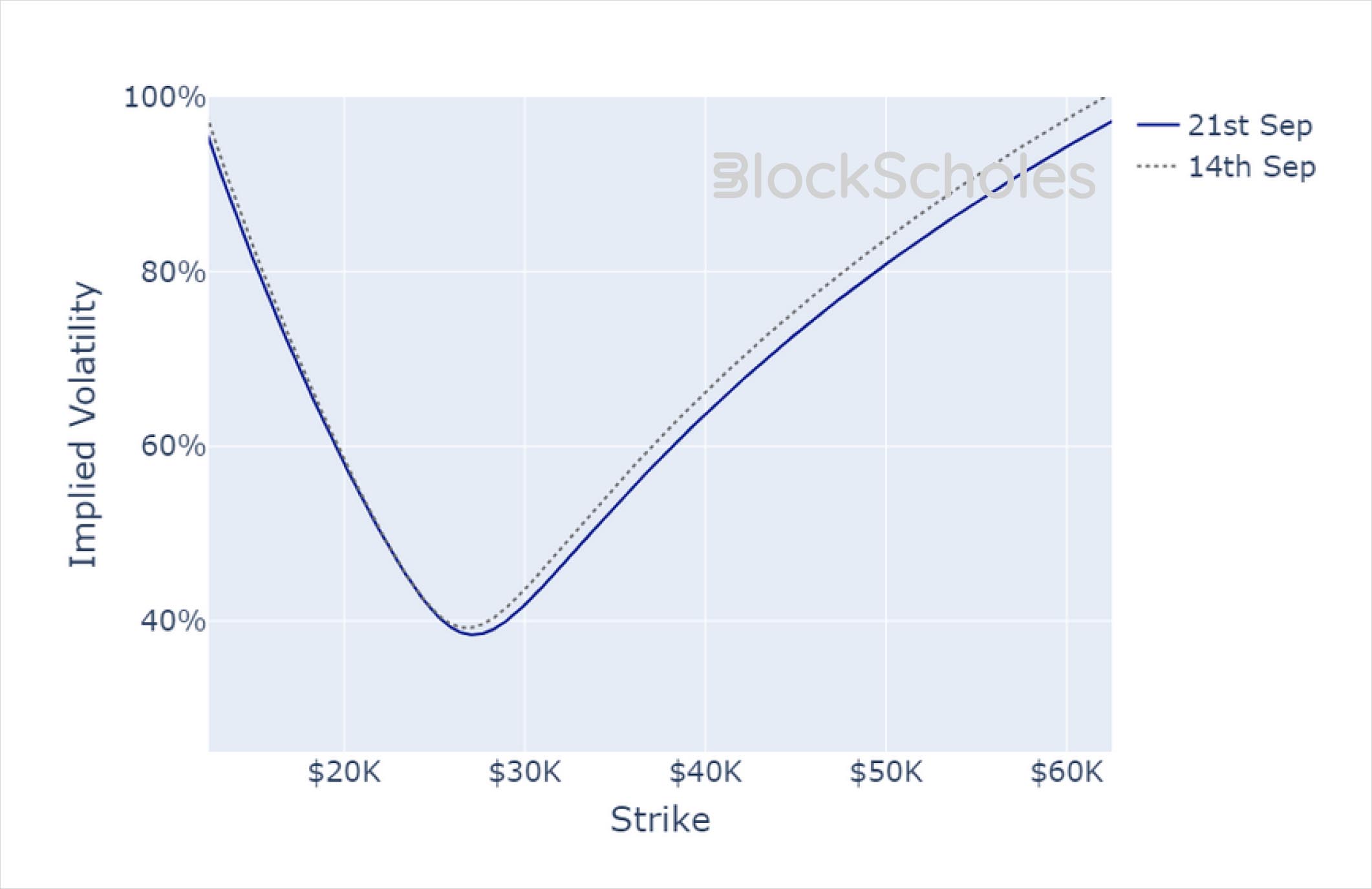

Historical SABR Volatility Smiles

BTC SABR CALIBRATION – 30 Day Tenor, 10:00 UTC Snapshot.

ETH SABR CALIBRATION – 30 Day Tenor, 10:00 UTC Snapshot.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.