Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

As the 12th of January crawls closer along the term structure, we see the first signs that vol markets are anticipating different responses between BTC and ETH. While the kink has moved closer and grown strong on BTC’s term structure of ATM implied volatility, ETH’s mid-Jan kink has largely resolved as a result of a rise in the 1W vol level. We see a similar departure in the skew of ETH’s vol smiles, which have slightly towards OTM calls in contrast to the spread seen in the skew of BTC smiles. However, there is little to separate the futures markets of both majors as perpetual swap funding rates explode positively and future-implied yields rise to their highest levels since July 2022.

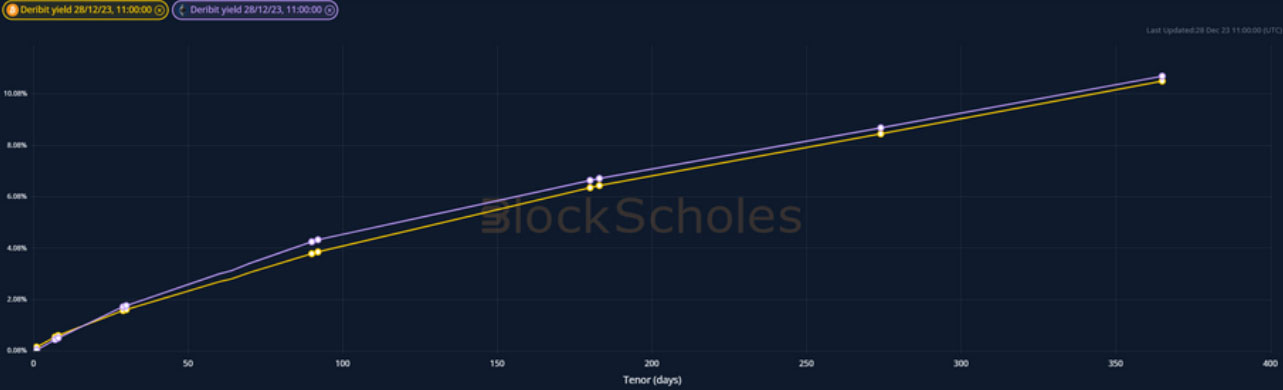

Futures Implied Yield, 1-Month Tenor

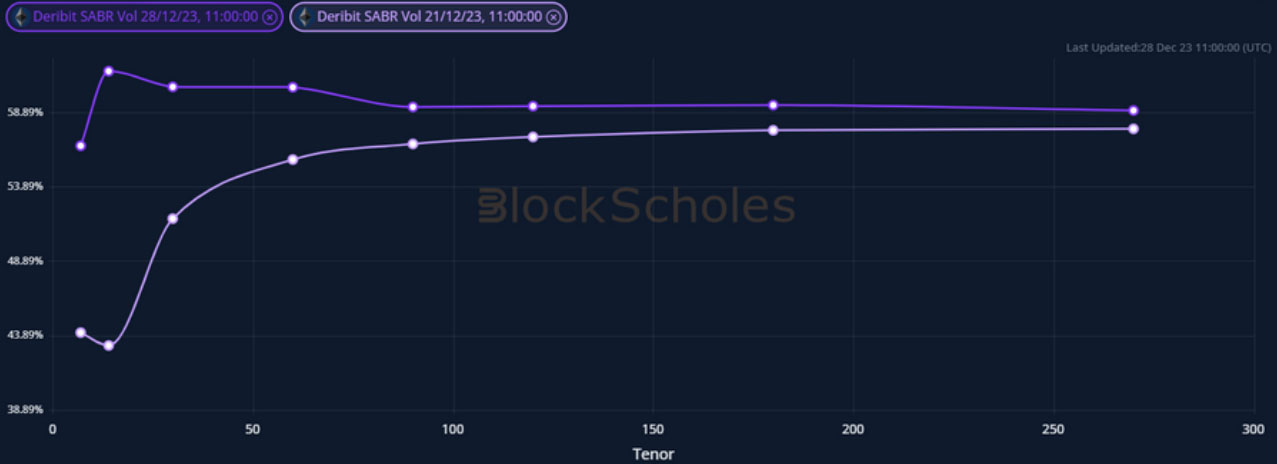

ATM Implied Volatility, 1-Month Tenor

*All data in tables recorded at a 10:00 UTC snapshot unless otherwise stated.

Futures

BTC ANNUALISED YIELDS – have reached above 30% at short-dated tenors for the first time since July 2022.

ETH ANNUALISED YIELDS – follow BTC’s into the mid-30s, reaching their highest levels in 18 months.

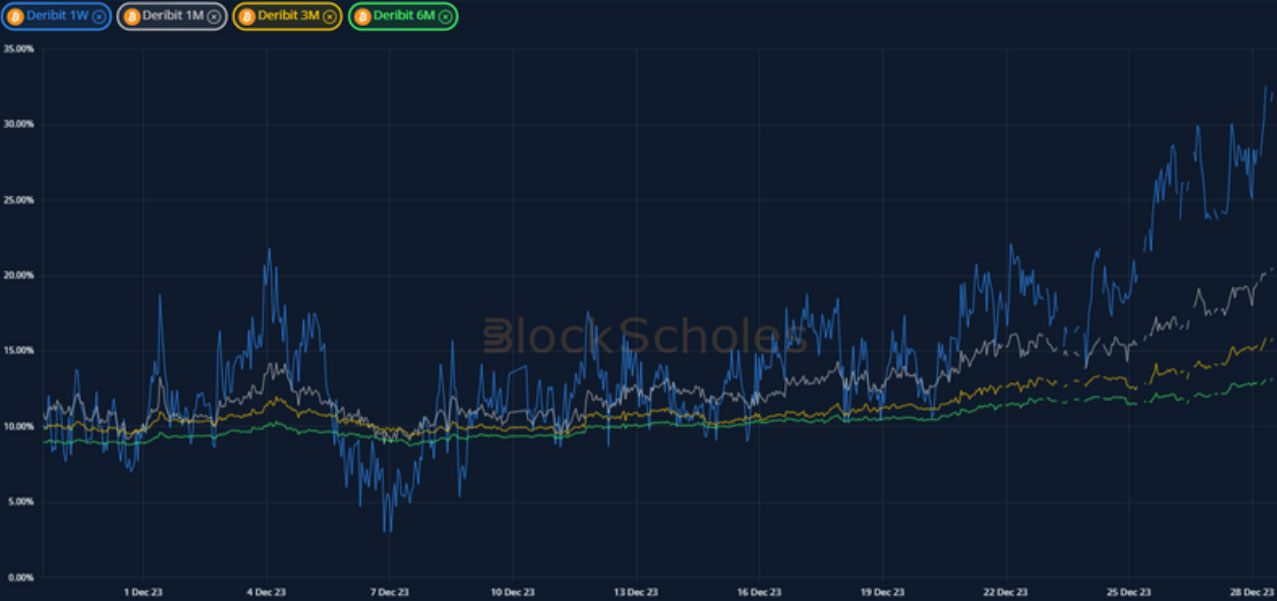

Perpetual Swap Funding Rate

BTC FUNDING RATE – rises to its highest levels in the last month, continuing an extended period of demand for leveraged long exposure.

ETH FUNDING RATE – rises to express similarly strong levels of demand for leveraged long exposure into the new year.

BTC Options

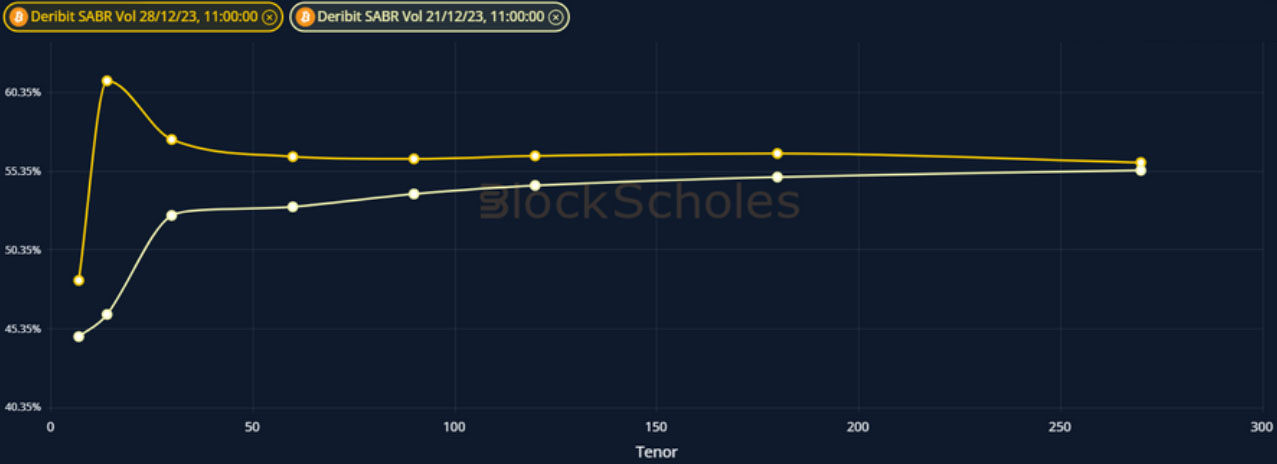

BTC SABR ATM IMPLIED VOLATILITY – the volatility of 1W tenor options rises as the expected Jan 12th ETF date moves across the term structure.

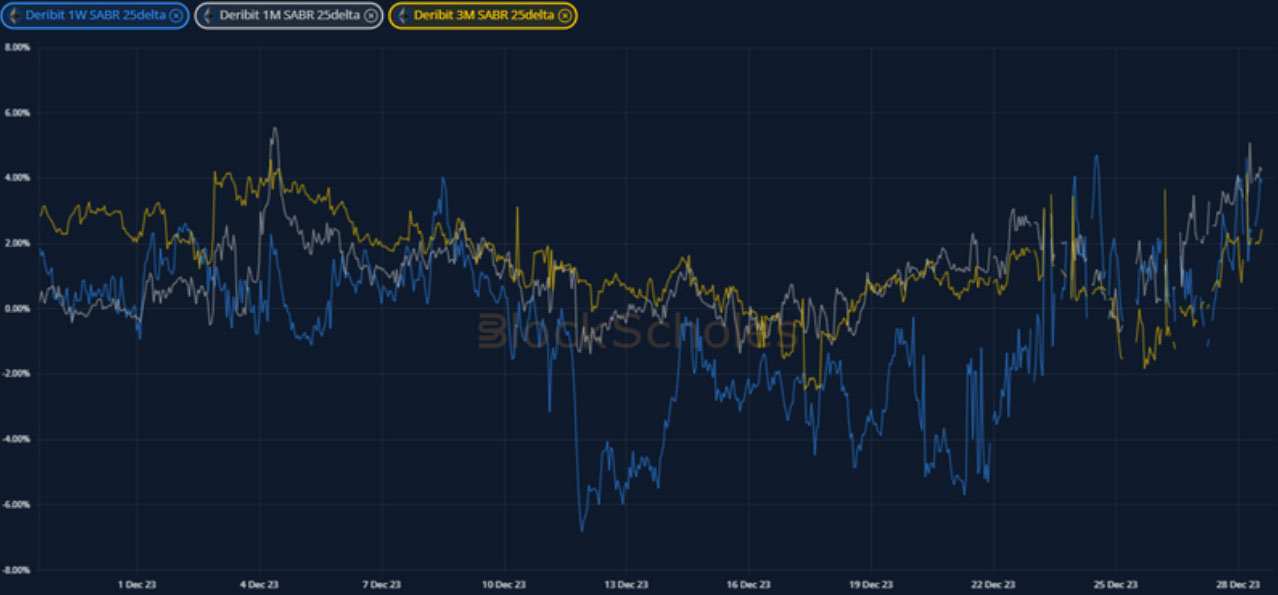

BTC 25-Delta Risk Reversal – short-dated smiles skew slightly towards OTM puts, widening the spread to the bullish sentiment in longer tenors.

ETH Options

ETH SABR ATM IMPLIED VOLATILITY – the mid-Jan kink has resolved with the 1W tenor implied vol rising to match vol levels at longer-dated tenors.

ETH 25-Delta Risk Reversal – smiles at all tenors have skewed towards OTM calls, in contrast to the spread seen in the skew of BTC smiles.

Volatility Surface

BTC IMPLIED VOL SURFACE – while the whole surface shows an increase in volatility, it is 3M OTM puts that have risen the fastest.

ETH IMPLIED VOL SURFACE – in contrast, ETH’s surface shows the strongest increase in volatility at short-dated upside strikes.

Z-Score calculated with respect to the distribution of implied volatility of an option at a given delta and tenor over the previous 30-days of hourly data, timestamp 10:00 UTC, SABR smile calibration.

Volatility Smiles

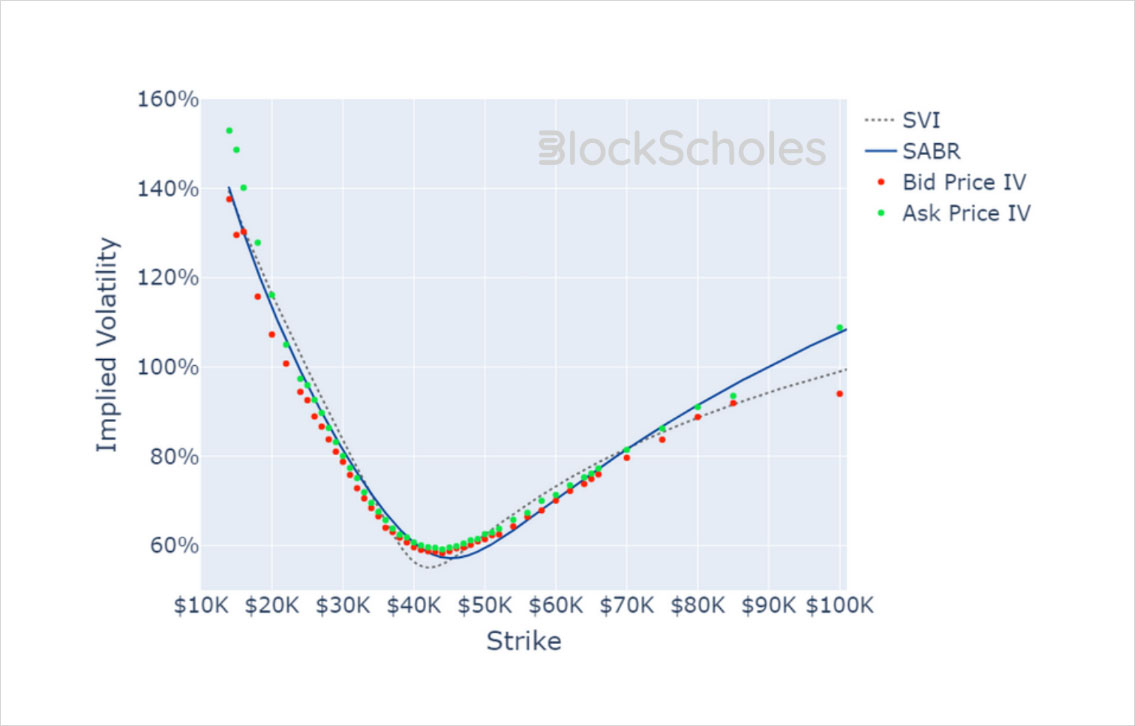

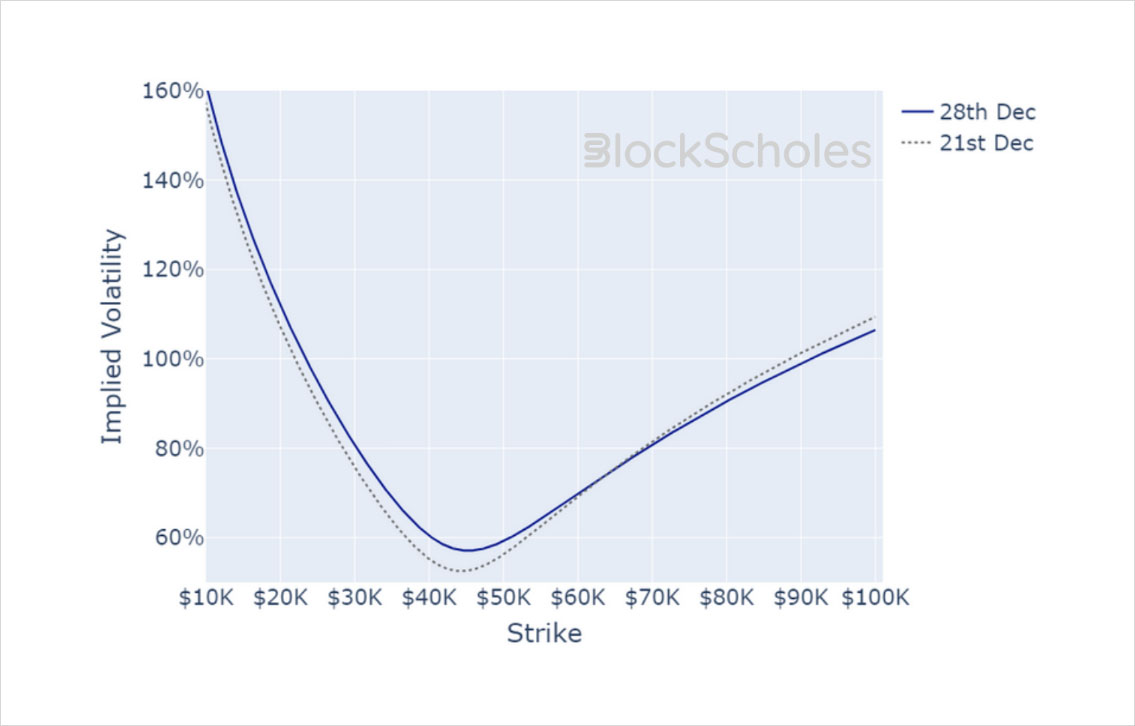

BTC SMILE CALIBRATIONS – 26-Jan-2024 Expiry, 11:00 UTC Snapshot.

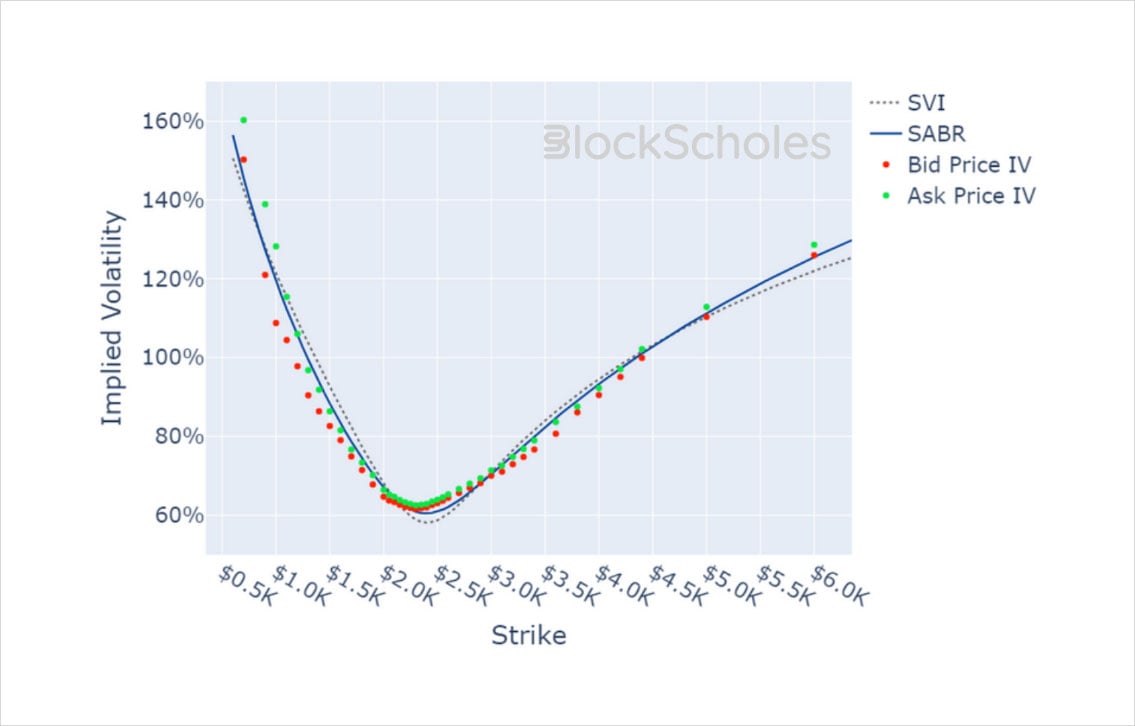

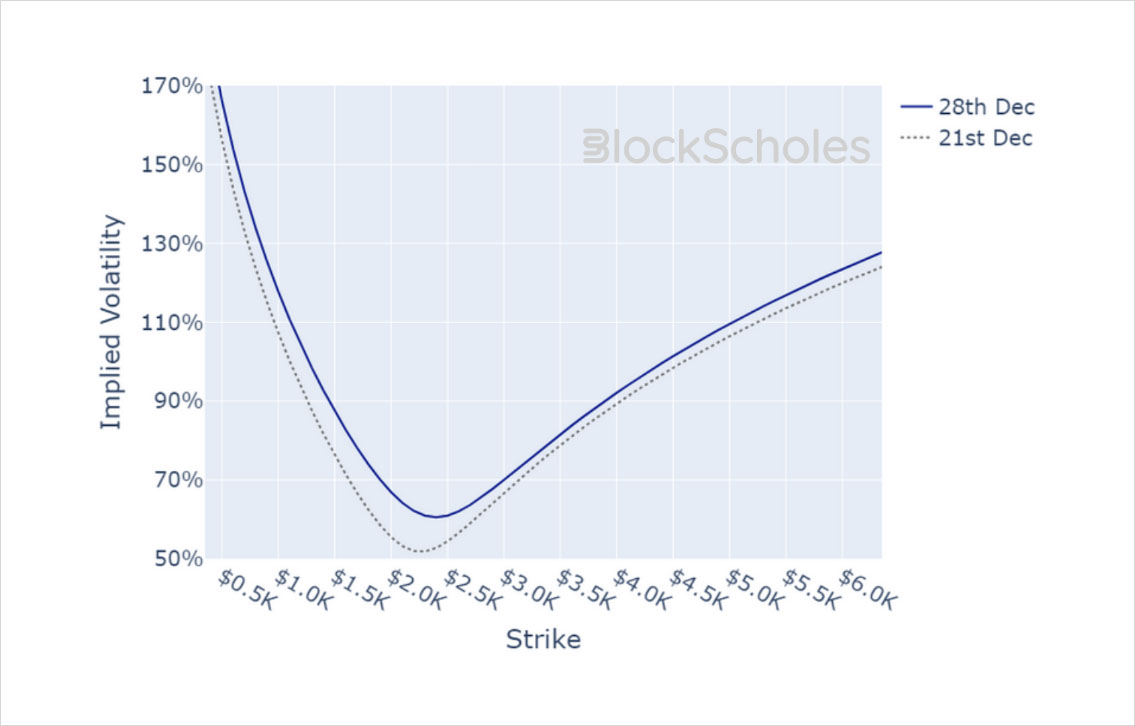

ETH SMILE CALIBRATIONS – 26-Jan-2024 Expiry, 11:00 UTC Snapshot.

Historical SABR Volatility Smiles

BTC SABR CALIBRATION – 30 Day Tenor, 10:00 UTC Snapshot.

ETH SABR CALIBRATION – 30 Day Tenor, 10:00 UTC Snapshot.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.