Hedge sentiment from Eastern Europe is the main reason for the short-term prices and volatility rise, while the “event shock” effect dominates this week’s price changes.

The statements of several Federal Reserve officials did not exceed market expectations and had little impact on the performance of the crypto asset market.

The liquidity squeeze at the macro level continues, and the future performance of crypto assets will still be limited. However, the new understanding of crypto-assets triggered by the war may become a new impetus to support the cryptos.

The Bear Encounters the Counter Cycle

The war in Eastern Europe has significantly impacted capital markets, with investors selling their risky assets and putting their funds into safe-haven assets such as precious metals and crude oil. As more sensitive secondary assets to liquidity, crypto assets have suffered a large-scale sell-off in a short time, causing the same level of volatility as before and after the Fed’s FOMC meeting in January, and the market cap has also shrunk to less than $1.6 trillion.

Subsequent events caught investors in the derivatives market a little off guard: due to the war and the impact of European and American sanctions, Russia sharply tightened foreign exchange restrictions. At the same time, as part of the sanctions, Russia’s connection with the SWIFT network was partially disconnected, causing investors in Eastern Europe to transfer funds to the crypto network, pushing the prices of BTC and ETH back to about $45,000 and $3,000 respectively. However, due to the limited scale of buying, the price of crypto assets began to decline again gradually after a short recovery.

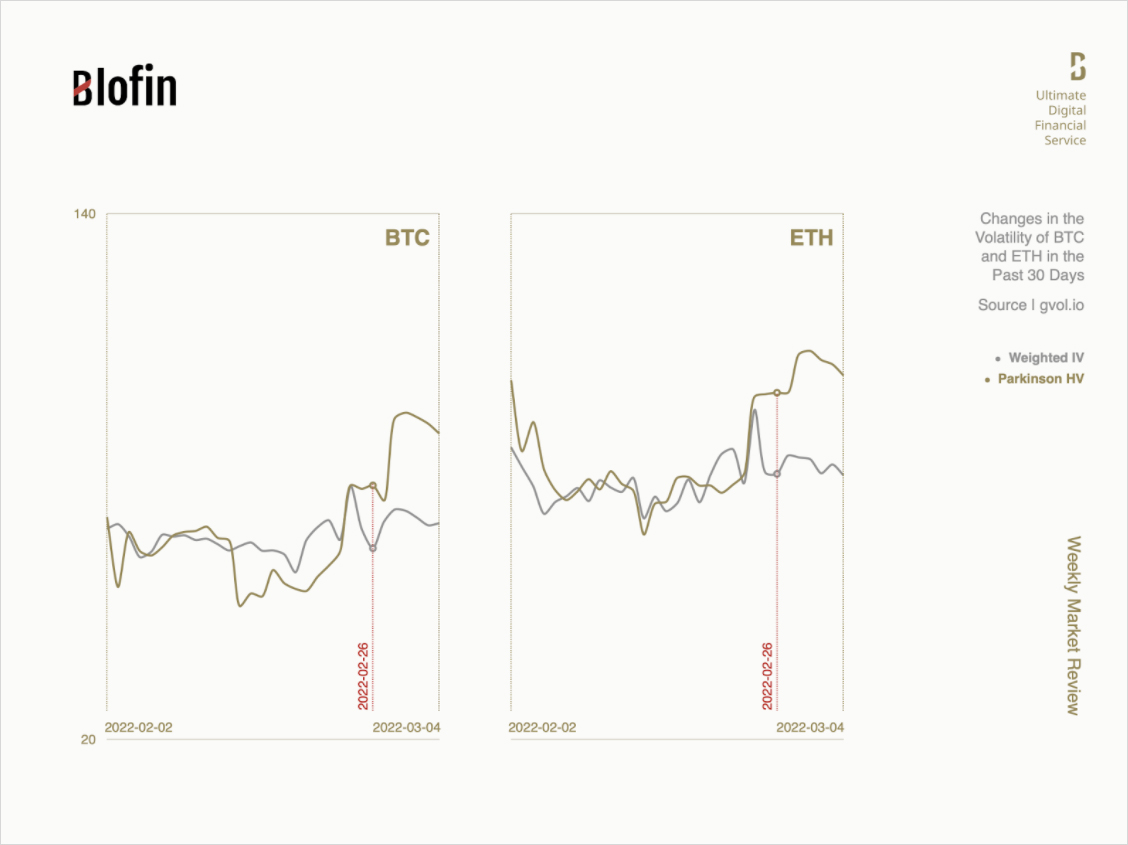

From a volatility perspective, we can see more interesting facts. Unlike events such as the FOMC meetings, which can affect the overall market expectations, the impact of local wars and subsequent series of events on the market has shown significant “shortwave” characteristics: the volatility of options near the expiration date jumps up and down rapidly, while the volatility of options farther away from the expiration date remains relatively stable. As we often encounter when traveling by ship, the wind stirs up the water surface while the underwater water is still calm.

However, the recent “waves” in the crypto market may have made experienced volatility traders vomit. According to block trading data, many traders who sell volatility seem to be trying to deal with rapid fluctuations through frequent risk reversal operations, but they still suffer some losses. In contrast, investors who adopt gamma strategies have made a lot of profits due to wide swings in prices.

In the recent drama, it seems that the actions of the Federal Reserve are no longer so necessary. The speech of Fed chairman Powell on Mar 2 did not trigger a new round of turmoil in the crypto market. The interest rate swap market had already digested the possibility of the Federal Reserve raising interest rates six times in February. The crypto market has also been ready. Some optimistic investors even believe that the underperformance of the crypto market is “temporary”.

However, trading data in the options and futures market show that this is not the case.

What Has “The Countercyclical Events” Changed?

What is certain is that although the short-term recovery has re-established the confidence of bulls in the crypto market and brought the funding rate back to positive for a time, the crypto derivatives market is still dominated by bearish sentiment.

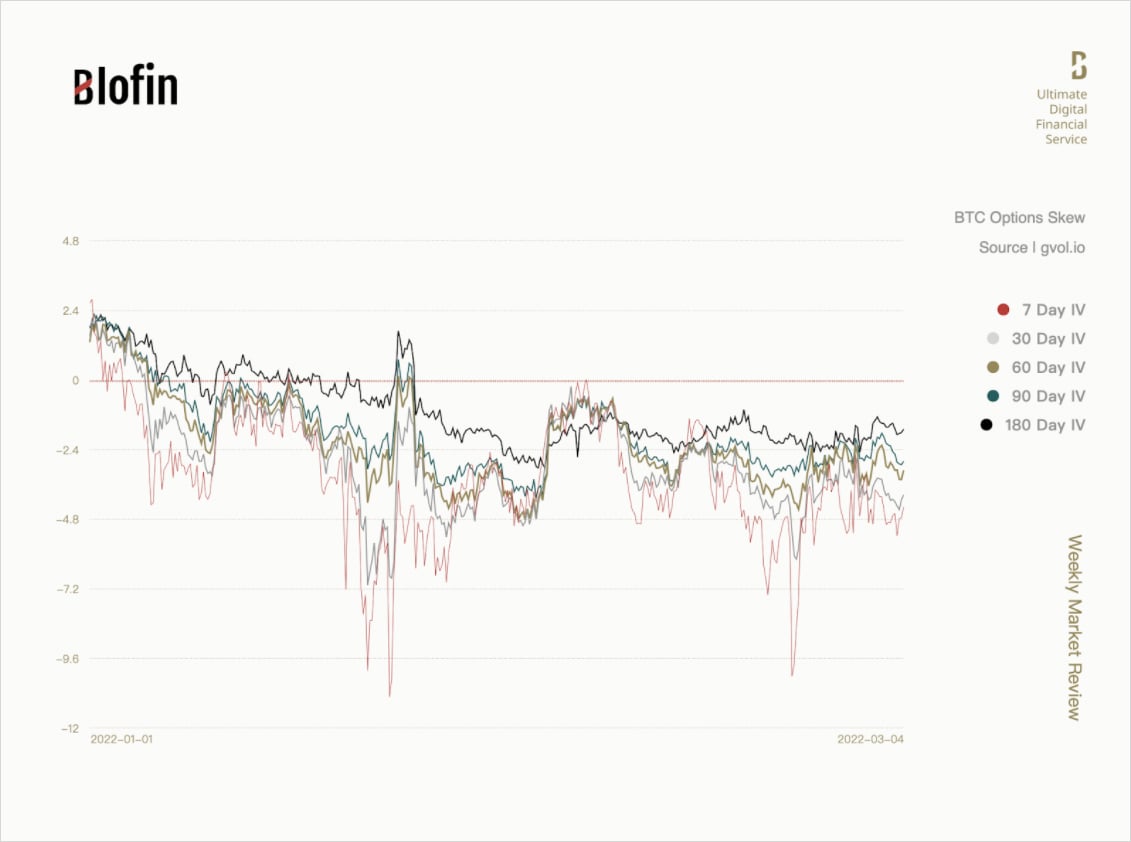

Since the beginning of the year, the skew of BTC and ETH options has shown an overall continuous decline. The negative skew trend has continued, whether it is a short-term option with less than a week to expire or a forward option with more than half a year to expire. Generally speaking, this means that bearish sentiment continues because option buyers are willing to pay higher and higher premiums to hedge their expected price decline risk.

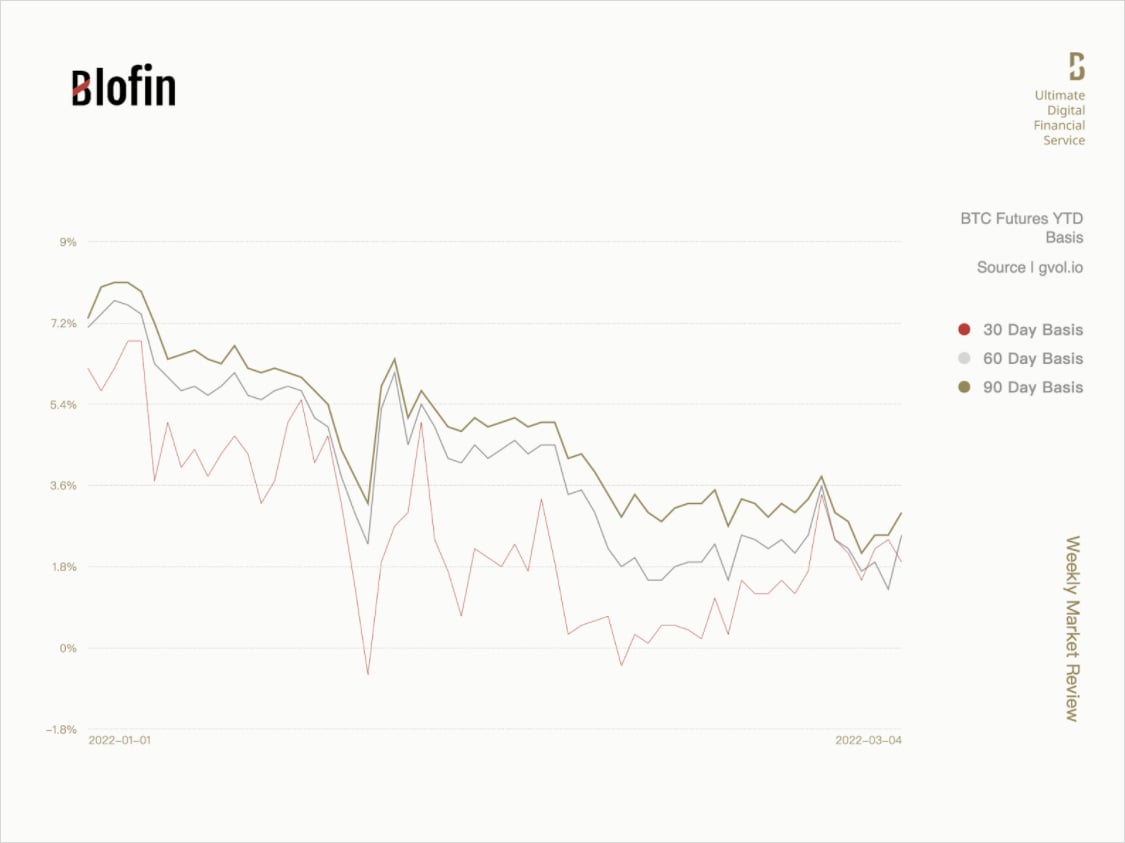

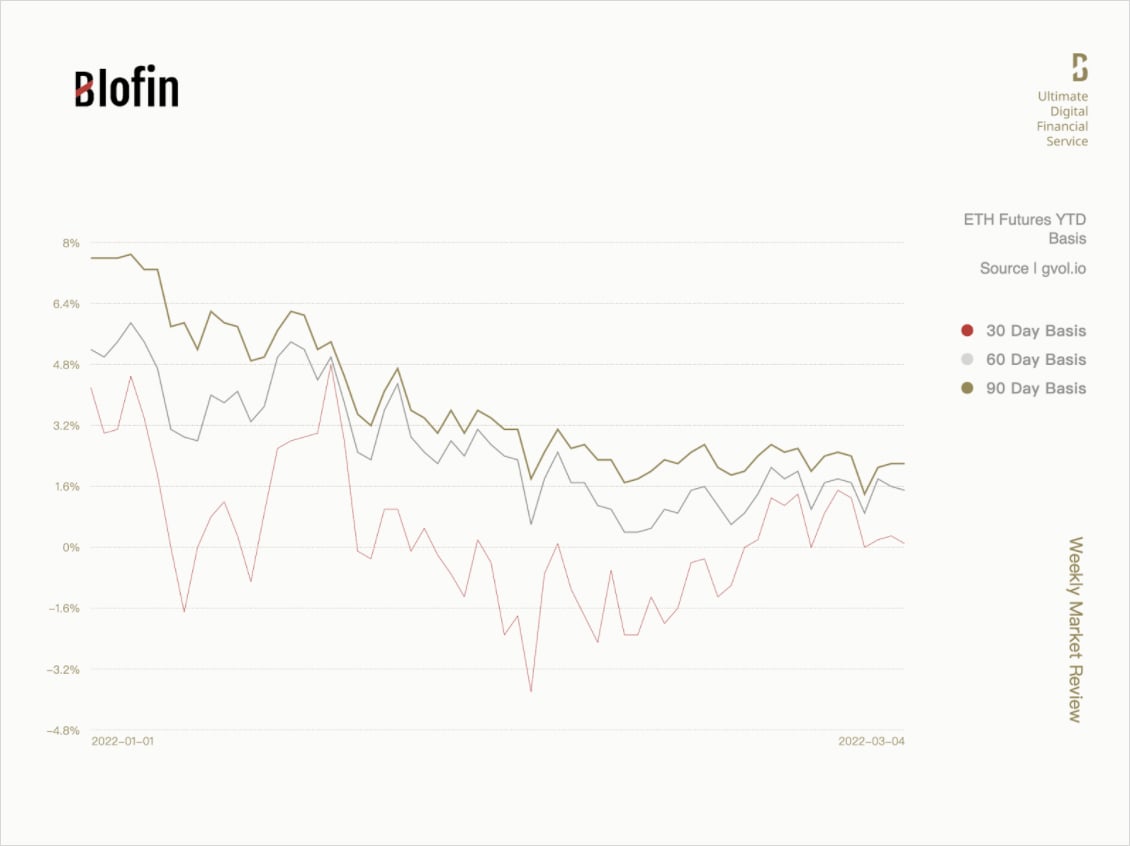

Investors in the futures market are also unwilling to pay more premiums to buy futures under the expectation of a decline. The premium between spot prices for BTC and ETH front-month futures has smoothed out, while the premium for far-month futures has converged to less than 5% by March. Suppose you observe the changes in the overall basis of the futures market. In that case, it is not difficult to find that the disturbance of the war to the basis is not apparent and has not interrupted the process of basis convergence.

It seems that derivatives investors do not believe that the “counter-cyclical effects” brought about by the war will last long. The Federal Reserve has confirmed an interest rate hike in March. The eurozone money market has already judged that the European Central Bank will raise interest rates by 30 basis points in December. At the same time, the central banks of major capital markets such as the Fed and ECB have agreed that solving the inflation problem is the primary goal and will actively use their monetary policy tools to achieve the inflation target.

After the leading capital markets isolated Russian market, the impact of uncertainty from eastern Europe on the financial market has significantly reduced, which means that the speed of withdrawal of market liquidity will not change due to unexpected events.

However, we cannot conclude that these countercyclical events are just fluctuations in the financial market. Every occurrence of countercyclical events will have an implicit impact on the market’s long-term performance, and the countercyclical events caused by war are especially serious.

Events such as the devaluation of the French currency and systemic financial sanctions during the war forced investors to reconsider the role of government bonds and gold as a haven. The government bonds may become worthless due to default. The depreciation of assets caused by financial weapons can erode a person’s life savings in a few hours. The “paper gold” and the actual gold may also be taken away in various ways. What happened to the Russians and Ukrainians is not guaranteed to happen to other investors one day. Investors realize that only a relatively secure, decentralized liquidity network can protect their assets. Before, people had no choice, but now, they have.The

change of concept is decisive for the shift in liquidity between markets. Although until now, crypto assets such as BTC and ETH are still recognized as secondary assets with high risks, due to their security, investors who have personally experienced the loss of assets under the “black swan” incident will eventually put some of the money in the blockchain network and store them in the form of cryptos, bringing additional backup liquidity to the crypto market.

In the future, with the increase of global uncertainty, the security of crypto assets will be more and more recognized by more people and eventually affect the distribution ratio of liquidity in the whole market. Although the decline caused by liquidity contraction is inevitable, more and more safe-haven liquidity remaining in the market will become the “ballast stone” of the crypto market, stabilizing asset fluctuations and becoming a new driving force to support the performance of crypto assets.

With the tone of interest rate hikes and scale-down already set, the impact of US non-farm payroll data and unemployment data on the crypto market may be relatively limited. Next week, the Fed will enter a period of silence. The impact from the Fed can be temporarily ignored when the market has fully priced its possible actions. However, the European Central Bank’s interest rate resolution may unexpectedly change due to its hawkish attitude in the March meeting notes, thus affecting the crypto market, which needs to be noted.