Cold storage… should temper crypto vol decline.

With the maturation of the asset class, the strategy of selling crypto volatility has come of age in 2022 and afforded stellar returns in what otherwise has been a tumultuous market. With plentiful supply from DOV’s to distressed miners and despite sizeable spot market shocks from UST, 3AC and FTX the crypto vol market has behaved relatively well.

As 2021 ATH’s and the heady days of parabolic price predictions fade into distant memory, saner and more orderly price action have afforded greater conviction to vol rent seekers attempts to wrestle control of crypto’s call wing. The communities awakening to the mean reverting nature of volatility has emboldened those abandoning reliance purely upon spot price appreciation for returns, to diversify and focus on extracting what yield they can from BTC and ETH options markets. The growth in this movement makes sense and as mentioned is a sign of the evolution and progress of the community as they embrace various TradFi methods on CeFi exchanges with some utilising innovative DeFi protocols. One of the major challenges faced by DeFi practitioners in particular has always been the well documented liquidity issues suffered by the very nature of the predictability of such systematic protocols up against savvy and sophisticated market makers. Those challenges have not changed. What has changed recently is we now add into the mix a sudden flight to safety post FTX, resulting in a surge in extraction of crypto off exchanges and into self-custody and cold storage. So called “shrimps” and retail hodlers may well be taking advantage of the sell-off to accumulate but whales and market makers are deleveraging and/or reducing risk, the latter being far more impactful in our opinion. Users of systematic strategies best be wary as the underlying liquidity assumptions they predicate their strategies on now must be called further into question. Even with waning participation, the weekly impact of DOV’s remains clear to see.

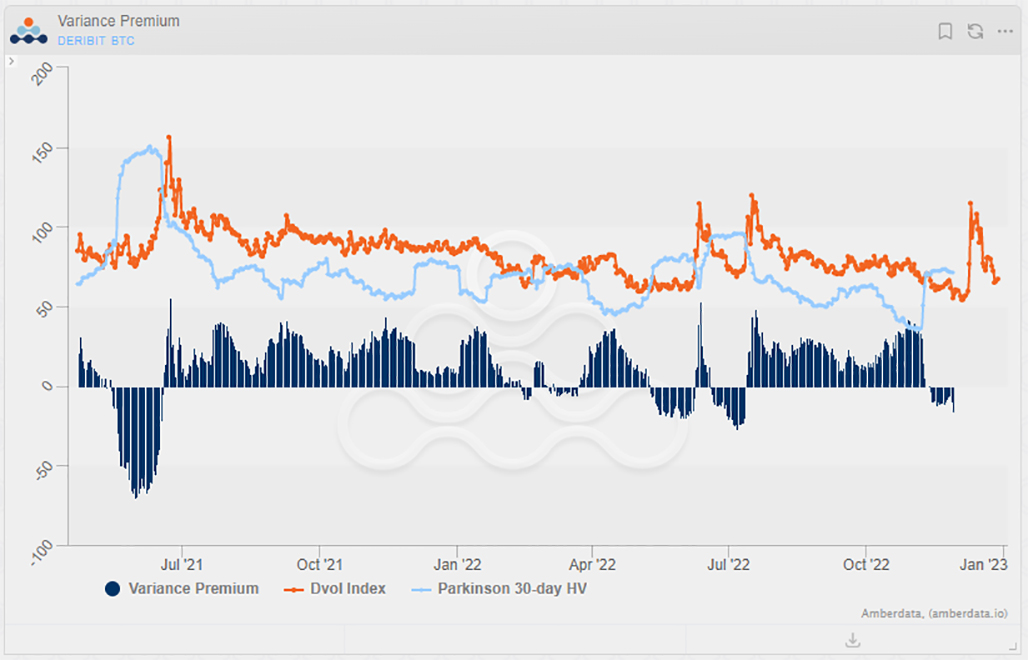

Liquidity is everything, without it even mature and supposedly mundane bond markets experience dysfunction, just look at the gyrations of the MOVE index through 2022 and the recent Gilt crisis. In light of recent crypto native events, understandably everyone’s guard is now firmly up. Still reeling and somewhat numb from one shocking revelation after another, the bar for event inspired or headline induced vol spikes inches ever higher to the benefit of vol sellers. However, going forward and absent any change in DOV or miner’s behaviour, we firmly believe we could witness much more prolonged and frequent instances of negative variance premium (see chart below) due to a trend higher in underlying realised at least until community trust is repaired and liquidity flows back onto exchanges. With the slow-motion car crash that is the FTX saga, it is hard to see that until well into 2023. Thus, in the short to medium term, opportunistic as opposed to systematic will be the key approach to sustaining the profitability of any vol selling.