In this week’s edition of Option Flows, Tony Stewart is commenting on turbulent spot markets.

April 27

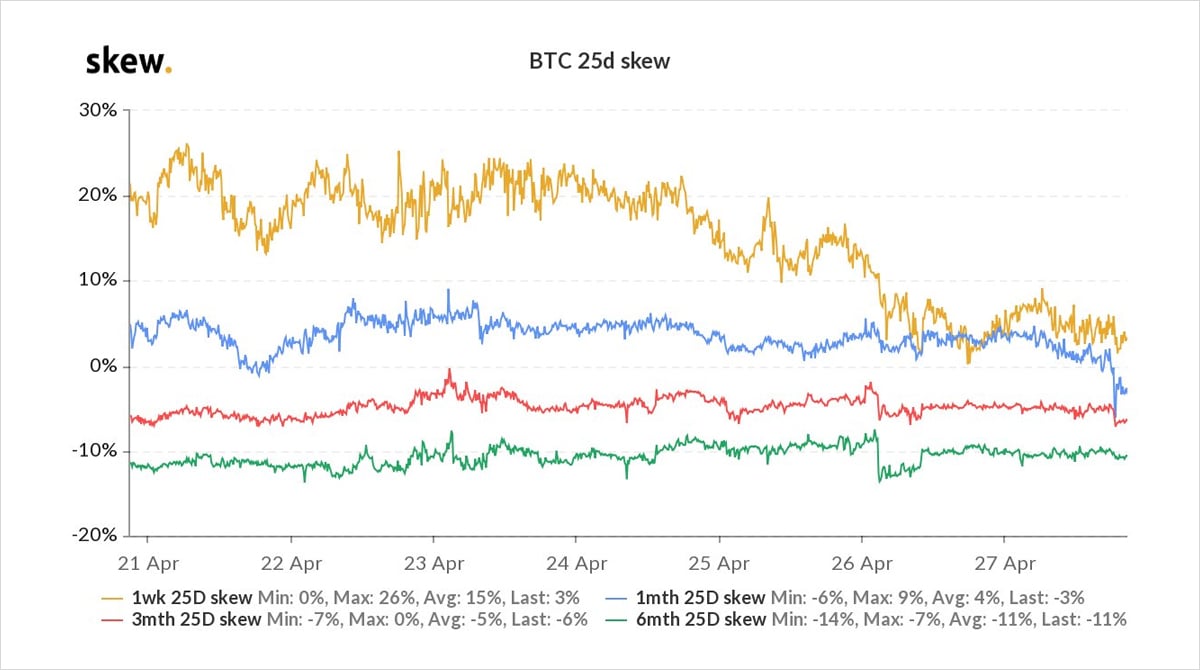

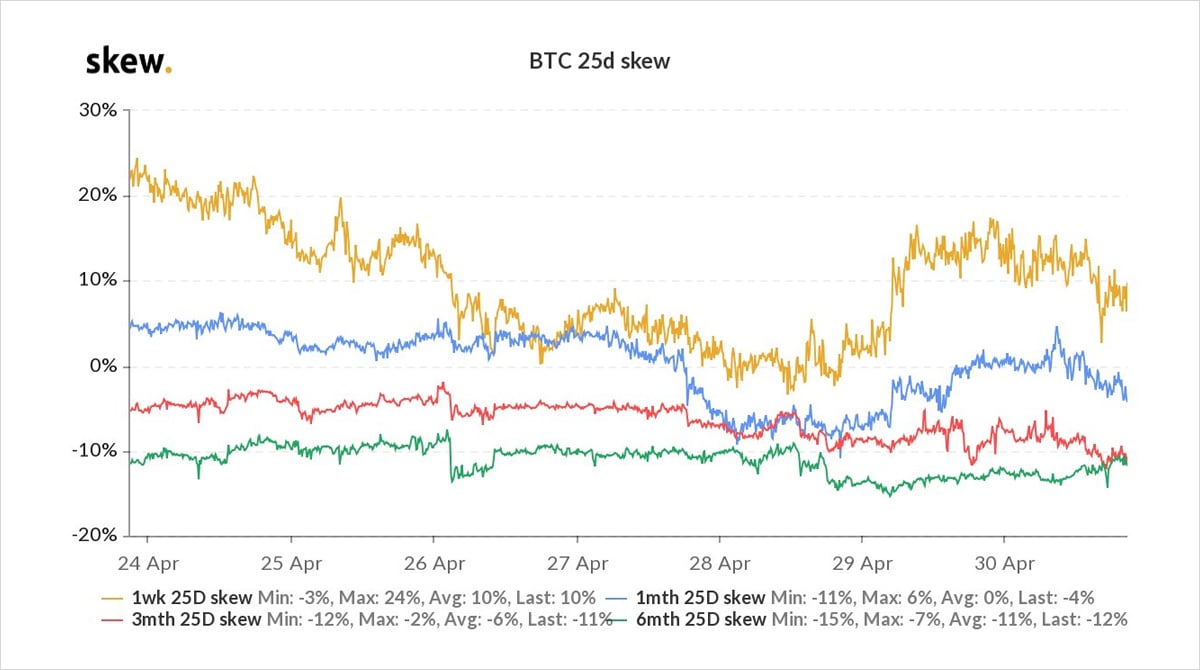

While spot markets have been turbulent, elevated Put skew protected longs over the weekend.

Resurrection returns us to 55k and 2.6k, as we were.

Option sentiment hasn’t changed.

BTC flows infer belief+caution; risk rolled, protection.

ETH flows infer vigour; narrative strong.

2) While BTC option volumes have been healthy, forensically they are dominated by Apr30th Expiry flows, fast money plays, risk management and rolling exposure.

More dominant trades outside Apr30th, have been protective; wide collars (initiator buying Puts), as Skew retraced flat.

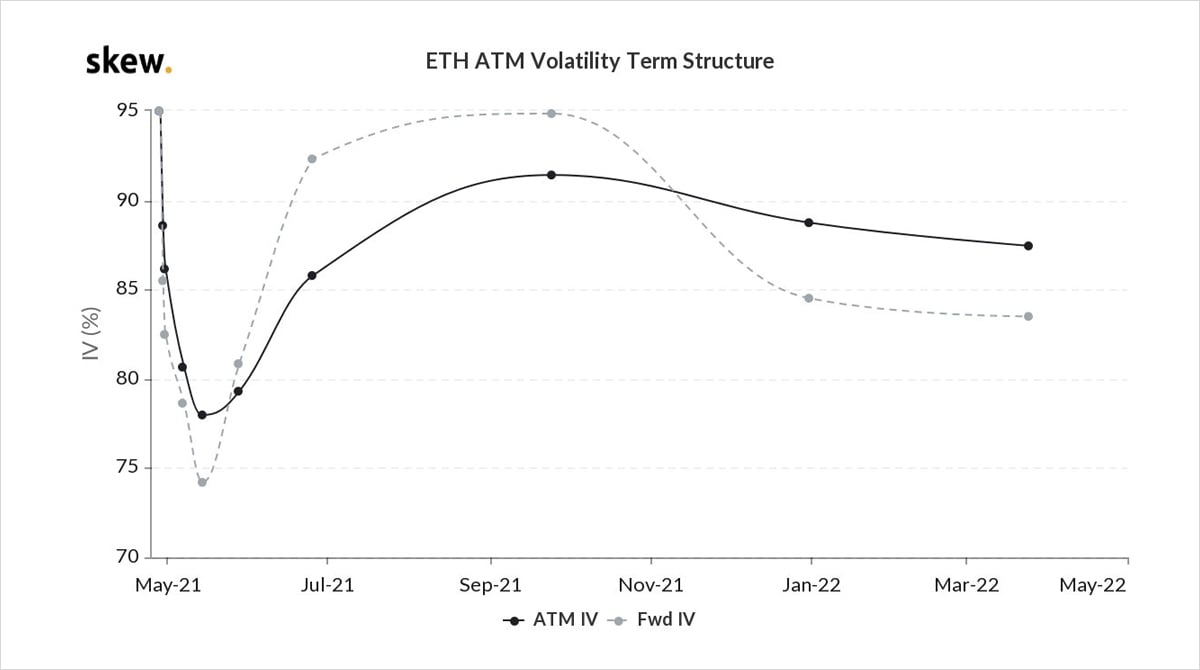

3) Interesting has been growth in ETH flows.

Fund structural-related action in May, today dominated by a buyer of May28 2400-3200 Strangles x10k, lifting IV 8% from low.

Books will define the motive as breaking the strike boundaries+premium, but other explanations feasible too:

4) May28th sits at the trough of the term structure, presenting the most efficient place to buy.

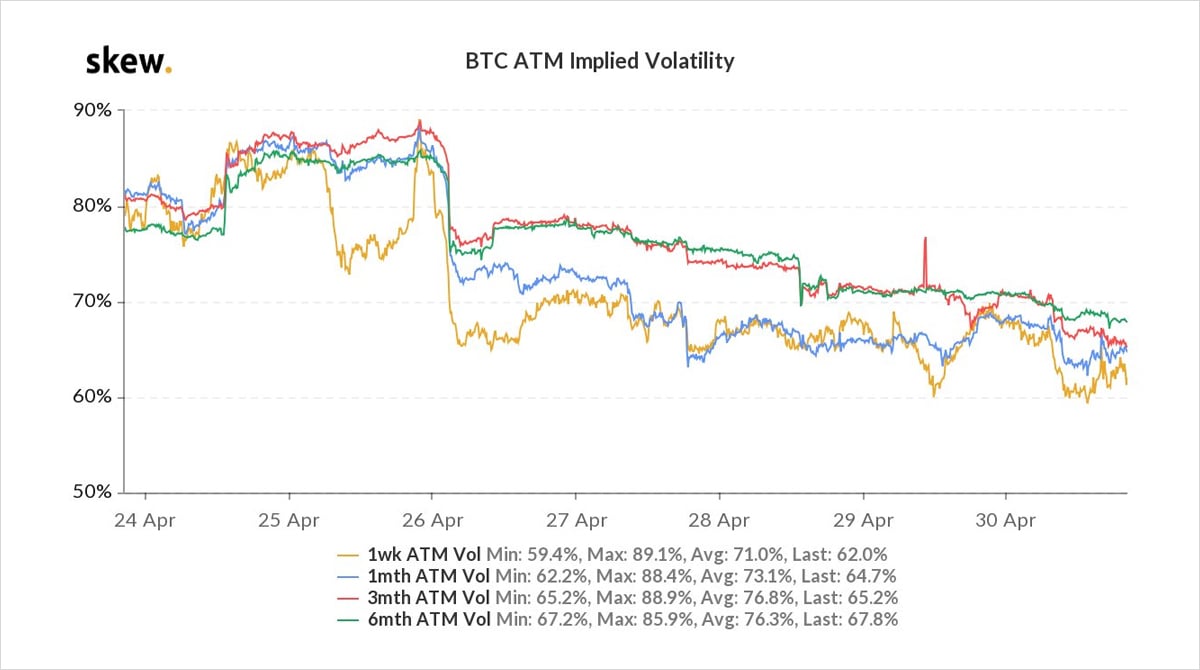

– 1wk-1m RV 90%, Strangle IV 79% upto 87%, good gamma optics.

– The 2400 Put could protect Spot longs, the 3200 Call could reflect a topside kicker, true bullish belief.

etc

View Twitter thread.

April 30

ETH took a rest as BTC structured Option flow returned for a day, one combination large trade dominating, temporarily creating ~1.5k BTC/$80mn notional d1 selling flow while BTC struggled at 54-54.5k post-expiry, then once the trade was filled, BTC ripped higher, breaching 57k.

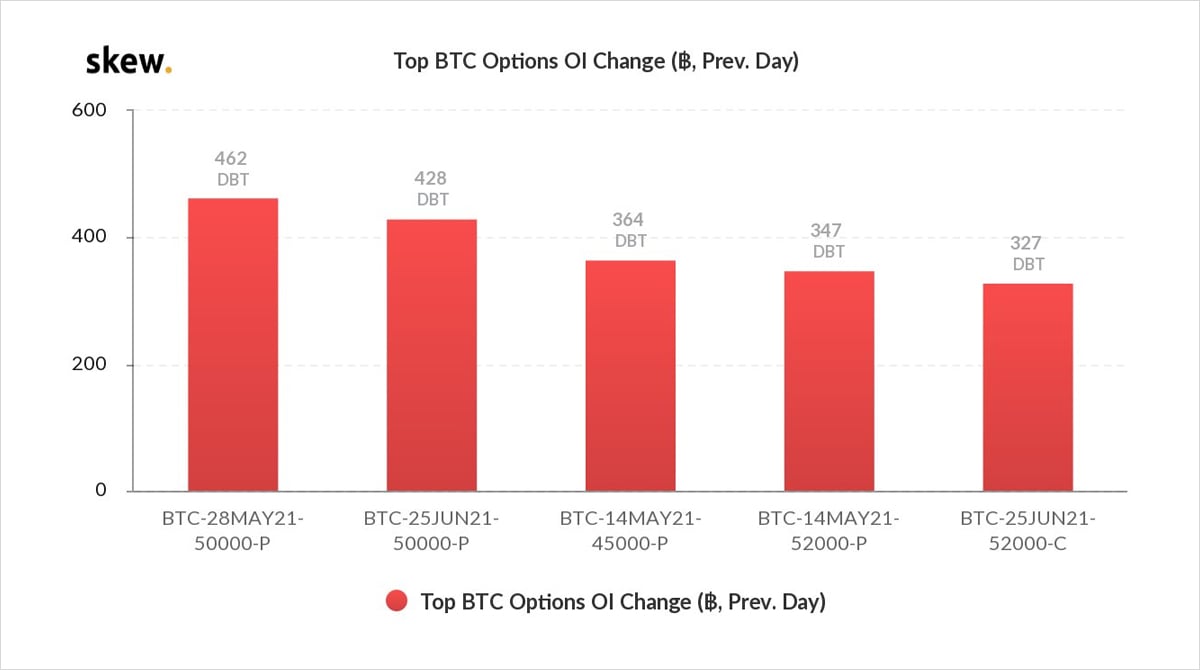

2) Initially, interest from a buyer of May 50k Puts, then Jun 50k Puts, but simultaneously offers in the Jun 50k + 52k Calls. Combined x1.5k+ May+Jun 50k Puts bought, x1.5k+ Calls sold.

Coincidental timing?..but also smaller size yesterday suggesting one player.

Package delta ~1.

3) The motivation is never clear without the full picture. This style of trade is rarely executed in a bubble; often attached to other risk exposure.

All appeared to be Opening interest, so not closing long Calls, then opening Long Puts, ie changing bias.

(Unless v off-exchange).

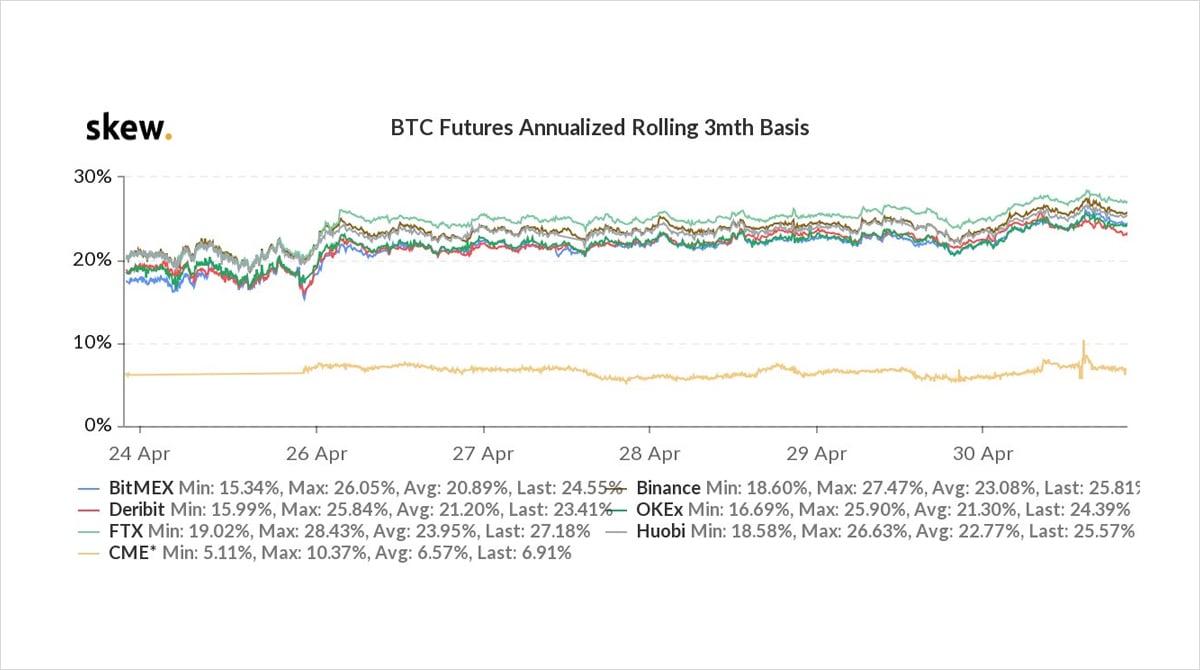

4) Annualized rates are becoming more of a discussion as ex-legacy individuals enter; – note cf Derbit v CME.

One theory is hedging an underlying Long spot BTC.

June trades at 25% APR.

52k Call sold at ~$7.5k, 50k Call sold at ~$9k, leave upside room.

50k Puts, May~$2k, Jun~$3k.

5) By selling June deltas (via Option execution) at 25% APR premium, the optics vs spot look attractive.

Market-makers/funds had to initially hedge with liquid perp/spot as Jun futures not tightly liquid, then spend time through the day locking in Jun Futures yield v Options.

6) June future remained under pressure all day.

Imagine if BTC Spot had fallen, rather than rallied.

The Calls (last to trade out) dominated impact on IV, but because the Calls were ITM, Skew was not affected (effectively the same strike being bought and sold, but OTM v ITM.).

View Twitter thread.

AUTHOR(S)

ex-MS Head of Trading desk /BTC Vol. Prop trading /Option Market forensics/ Alter Ego account Digital Asset arena. Tweets are my opinion, not financial advice.