In this week’s edition of Option Flows, Tony Stewart is commenting on drifted volume and China FUD.

May 29

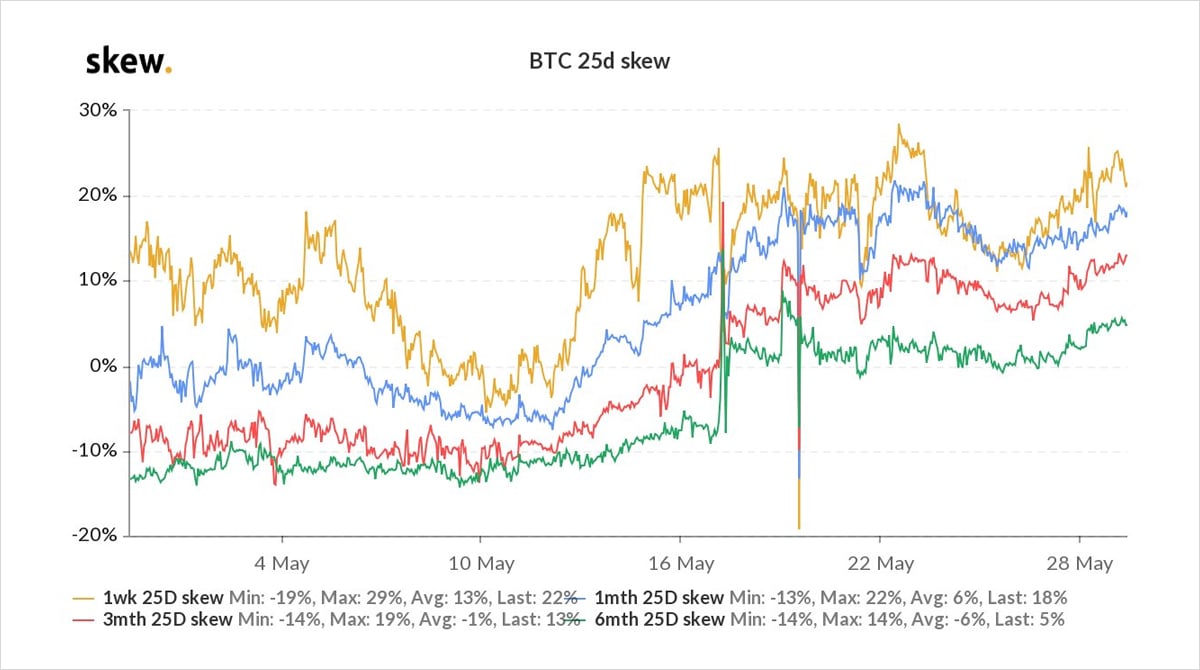

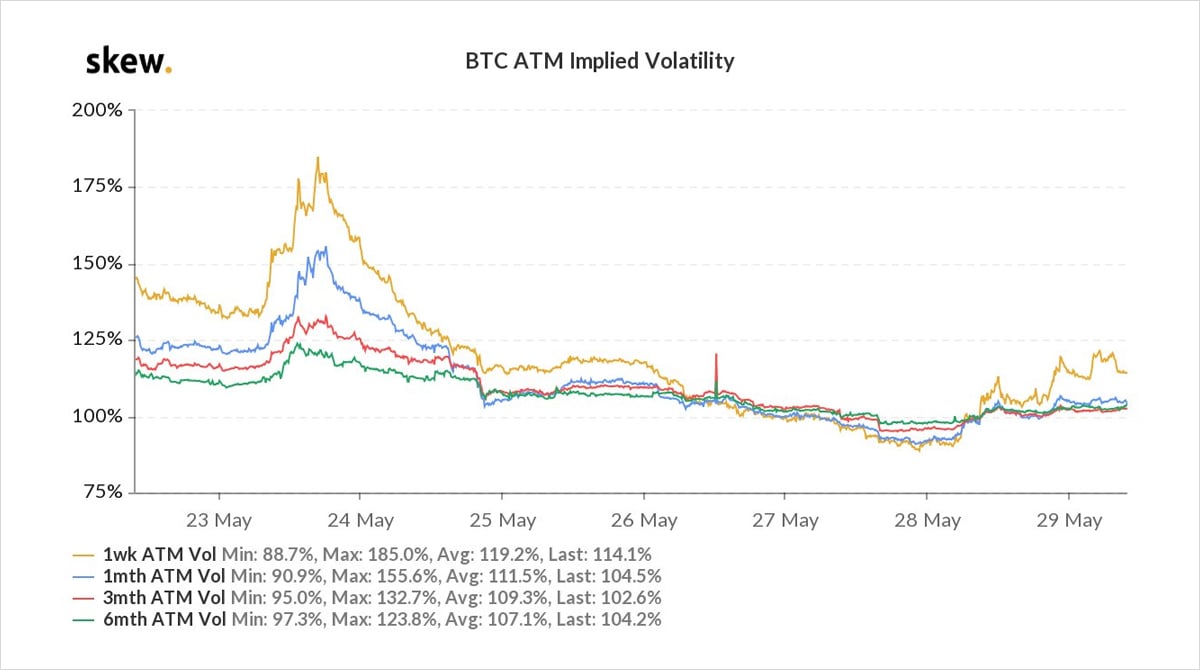

Volumes and Implied Vol have both drifted during the week, but Put Skew remains firm, as downside concerns persist following more China FUD, resulting in protective and speculative Put buying.

On rallies, particularly when BTC >40k, observed Call sales, yielding gains vs spot.

2) Most Put volumes have focussed on Jun4-11th expiry 25-30k Strikes, ie short-term ‘low’ premium cost.

Combined with sales of Jun 40-50k Calls, Skew metrics have firmed as illustrated.

Technically, Put spreads now more efficient to buy as protection, unless concerned about <25k.

3) General exhaustion and concerns over recent illiquid weekend moves on this ‘long weekend’ (in parts of the world) instigated a bounce in Implied vol in late US session: buying/covering gamma, paying theta to hedge vs bearish bias or a possible spot spike with funding flat/-ve.

4)

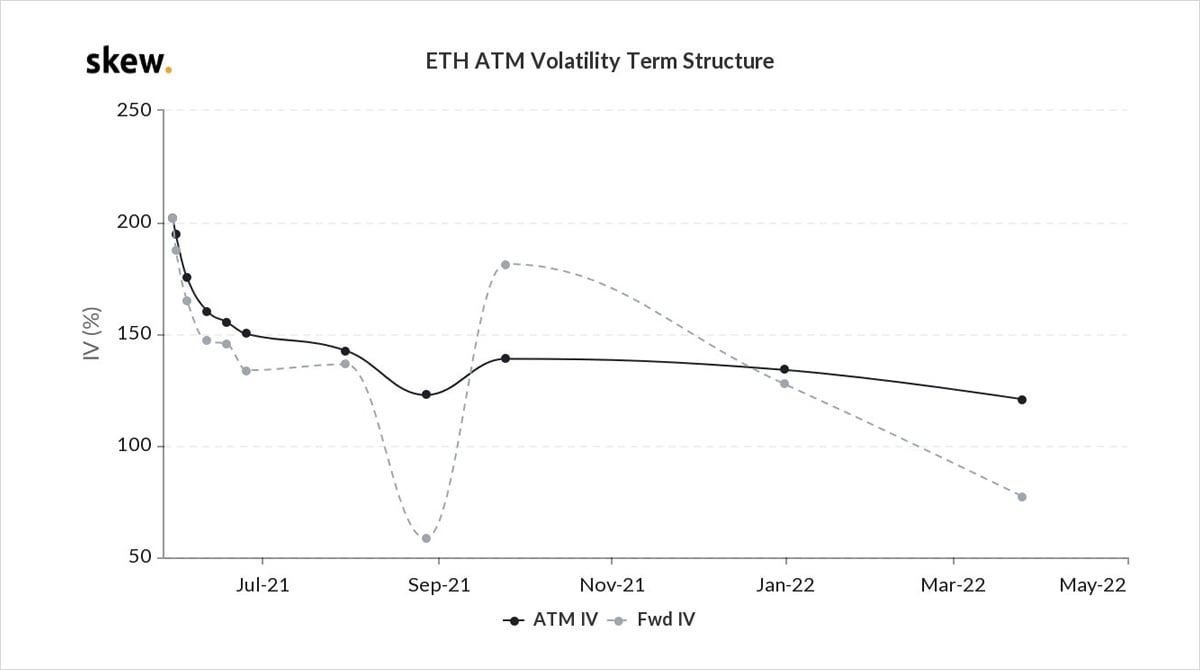

Behaviour on ETH Option flows has been very similar, but with arguably less speculative and more protective Put buying (20-23k Strikes, closer % spot relative to the ATM than BTC).

Skew + Implied Vol dynamics the same.

Term Structure backwardation with 10RV ~300, 1m ~200%

View Twitter thread.

AUTHOR(S)

ex-MS Head of Trading desk /BTC Vol. Prop trading /Option Market forensics/ Alter Ego account Digital Asset arena. Tweets are my opinion, not financial advice.