In this week’s edition of Option Flows, Tony Stewart is commenting on Politics, Trad Finance and Wall Street.

January 30

‘A week is a long time in Politics’ – Harold Wilson.

This week may be the tipping point of Trad finance into Crypto. Wall Street showed its ugly side. Defi + Alt interest surged while BTC remained volatile, testing weak hand resolve <30k, while Insto’s accumulated. Then Elon.

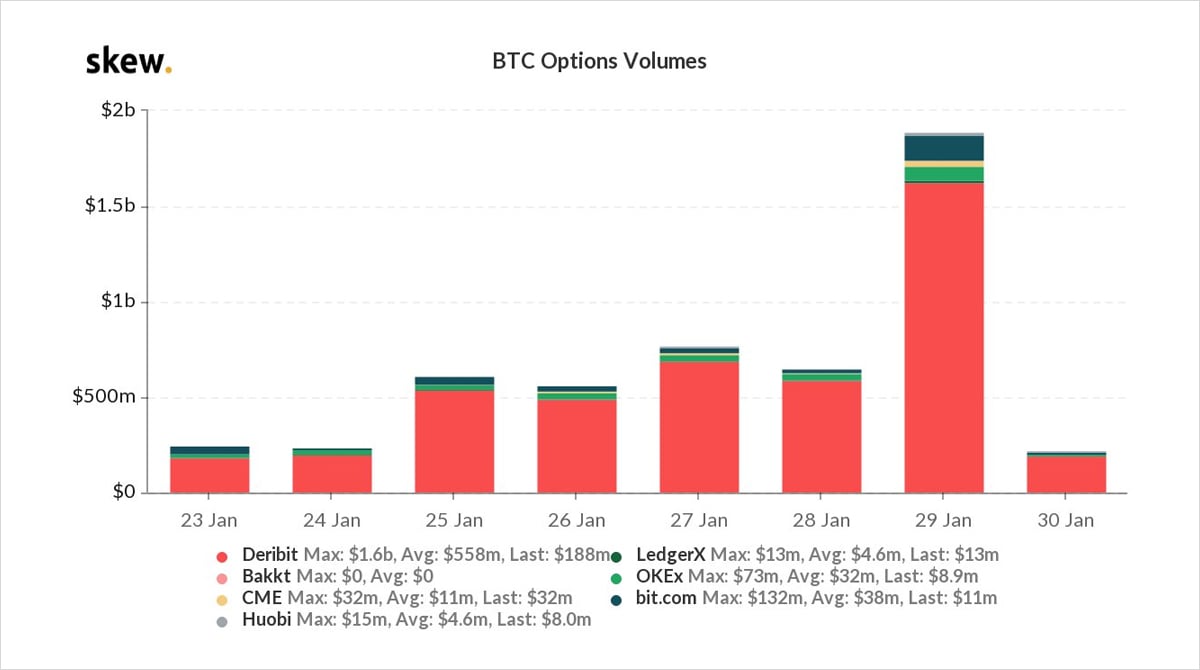

2) In the run-up to Deribit’s largest Open Interest expiry on the 29th Jan, the week started quiet.

The 22nd Jan BTC dump <29k had allowed weak hands to exit, institutional players to add; it was the shake-out that many had looked for.

Option volumes low; Alts+Defi attracted.

3) Near-term Puts were discarded as BTC rallied hard, Implied Vols were stable. Option activity focussed on Funds rolling Jan29th exposure into Feb 5th, mostly retaining Call exposure.

But the rally didn’t convince and protective Feb5 24-30k x1k + Mar 9-14k x2k Crash Puts bought.

4) Mid-week 27th Jan, saw another test for BTC.

Put buyers looked justified. But BTC selling was orderly down to 29k, and the ‘higher-low’ propelled BTC 20% to 34k.

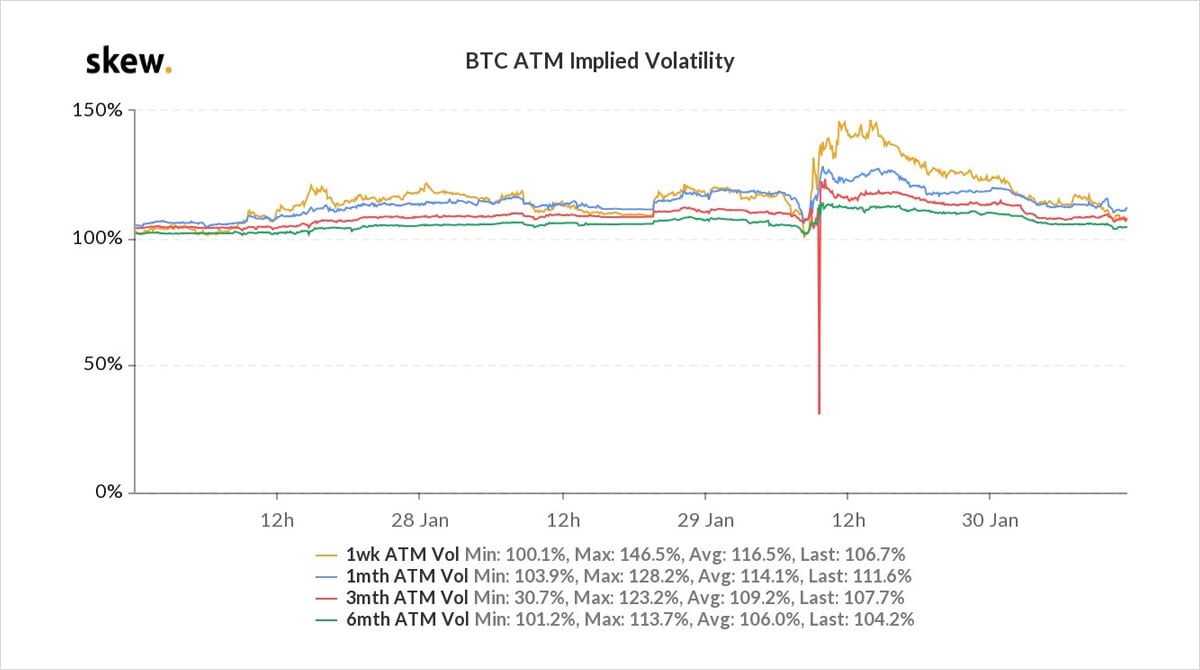

Option gamma was cheap even at >120%.

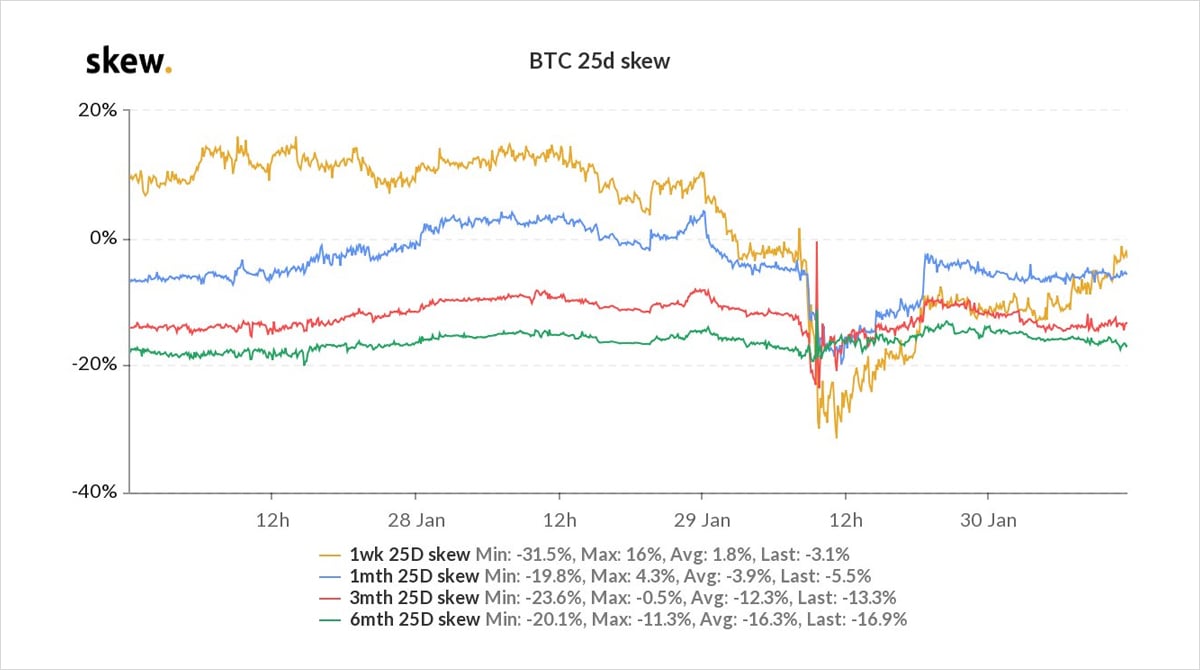

Again though, Puts bought, this time Feb26th 28+30k, 1month Put skew pumped.

5) Meme-reinforced Asian hours selling from 34k to 32k into Jan29th Options expiry. 32k held.

One ‘Fund’ logically decided the range was set for the next week, selling 5th Feb 28k Put 40+42k Call Strangles (Selling both) x800, crushing near-vol 15%.

Within 2hours the price had x2.

6) When Crypto-Twitter realized at 8:30am UTC, 30mins post-expiry that Elon Musk had changed his bio to one-word – Bitcoin, it took 30mins for the market to rally from 32k to 38k, liquidating $400m of shorts.

Feb 5th Calls went mental IV 200%+.

Buyers 1.5k+ 1week 50k-64k Calls.

7) Skew flipped. No-one cared about Puts anymore. That one word ‘Bitcoin’ pushed many to the conclusion that Elon was about to announce Tesla Treasury allocation.

With the MSTR conference next week, pre 5th Feb expiry, the upside was Calling.

Vols spiked in near-dates. Call led.

8) Expecting a surge from the US investor base, funding ballooned….but it didn’t come. If it did, it was over-run by deleveraging. Insufficient Spot.

Option market took advantage.

Large seller Feb12 40k Calls x1.5k at 130%.

OTC Feb/Mar 1×2 Call spread bought, hitting OTM Calls.

9) Now Implied Vol was getting hit from Feb12 Calls, absorbed by MMs hunting Gamma and upside.

Upside Calls hit from 1x2s (bullish payoff, but impact to hit upside Skew).

Short-term Puts bought again, limited quantities.

Overall impact – reverse Call Skew flip.

IV backwardation.

10) The weekend has seen its natural sell-off in Implied Vol at the near-end. IV has gone into contango, with selling of Feb1-12, rolled into Feb26/Mar, which has also drifted in with Spot maintaining 33-34.5k range.

Note Feb5th Strangle seller, never in doubt, back in profit!

View Twitter thread.

AUTHOR(S)

ex-MS Head of Trading desk /BTC Vol. Prop trading /Option Market forensics/ Alter Ego account Digital Asset arena. Tweets are my opinion, not financial advice.