In this week’s edition of Option Flows, Tony Stewart is commenting on the FOMC meeting and some light trading.

December 17

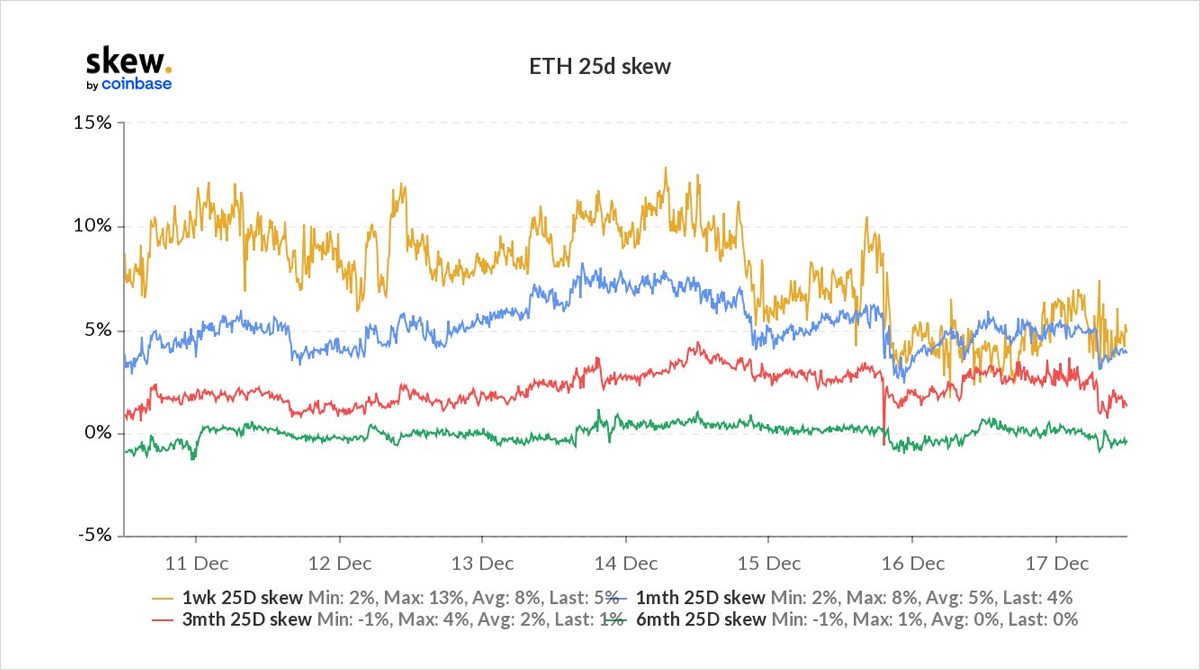

Given the unease leading up to FOMC, Option flows were surprisingly light, IV firmed only fractionally, Skew was benign.

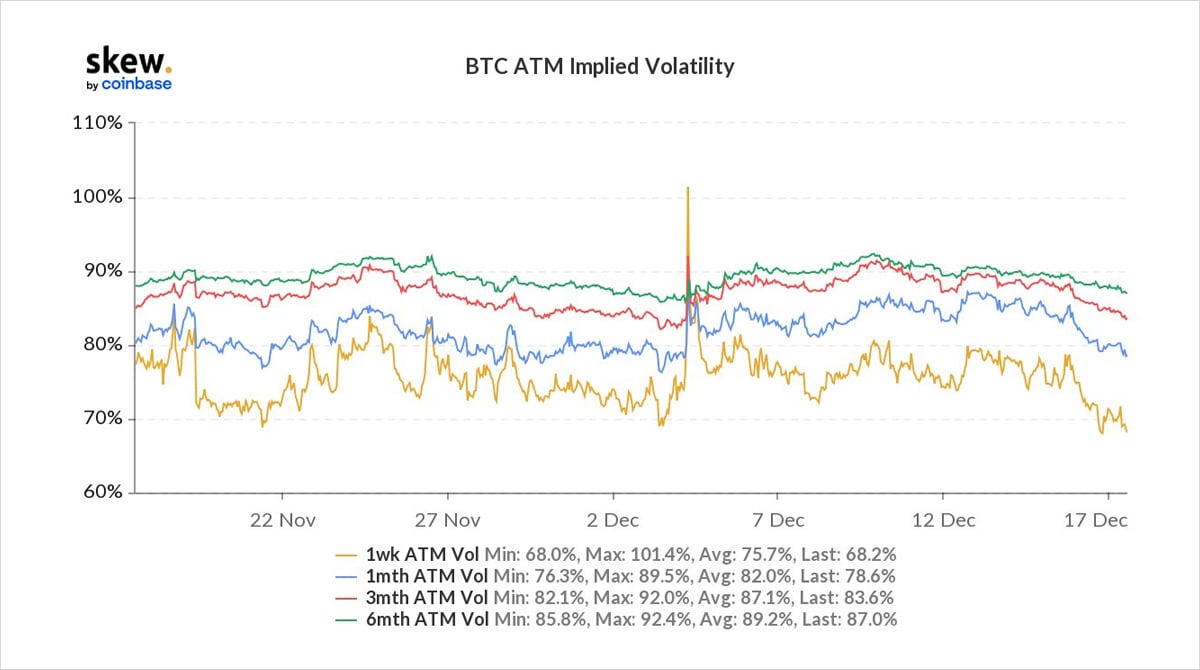

With no shocks, Spot+RV drifting, IV has consequentially been hit hard.

One Fund used flat Skew to add protection:

24th Dec BTC 45-52k, ETH 3.7-4.4 RRs.

2) 24th Dec BTC 45-52k x750 (50delta 18m notional delta), ETH 3.7-4.4k x5k, (50delta 10m notional delta) Risk-Reversals bought for the Put when BTC Spot 48k, ETH >4k, hedged by MMs selling the delta.

Calls fund the Put resulting in low net cost.

Often employed to protect vs AUM.

3) RRs privately negotiated, not aggressive, negligible impact on Skew.

Skew is one form of Fear/FOMO measurement, the other being IV (the cost of premium); near-date hit to 1m lows.

The whole term-structure has fallen, but Dec hit actively & Jan7-Dec31 50k Call Cal bought x1k.

4) All this evidence, coinciding with slightly positive funding, would conclude a deleveraged market in a quiet holiday season. Sometimes we dream of a break, but previous end-of-year activity has been far from passive. Flat Skew and further IV drift could present opportunities.

View Twitter thread.

AUTHOR(S)

ex-MS Head of Trading desk /BTC Vol. Prop trading /Option Market forensics/ Alter Ego account Digital Asset arena. Tweets are my opinion, not financial advice.