In the first few sections of this course, we covered the basics of how call and put options work. We covered how to calculate the profit/loss of each at expiry, the breakeven points, and how these calculations differ for cryptocurrency options. We also executed a few basic live trades, taking whatever prices were available at the time, however we haven’t yet given any thought to what actually influences the options prices (or premiums) themselves.

When an option expires, it’s value is easily calculated using just the strike price and the underlying price at expiry. However, while there is still some time left until expiration, there are other factors that affect an option’s price, primarily the amount of time left until the option expires, and volatility. In section 7 we will finally start adding some meat to the bones by studying volatility, option pricing, and the Black Scholes option pricing model.

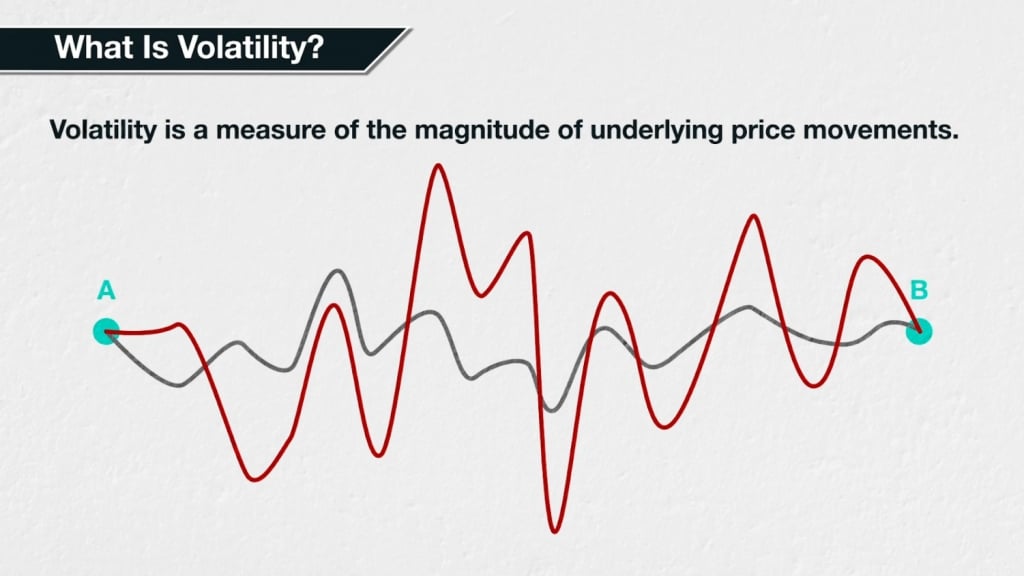

What is volatility?

There are different types of volatility which we will cover shortly, but each is a measure of the price movements of the underlying asset. More specifically, a measure of the magnitude of the price movements. The larger the swings in price, the higher the volatility.

Take these two lines, each representing the price of a different underlying asset. Both start at the same price, and end at the same price. So they have both moved from A to B over the same time period. It is clear to see though, that the grey line did so with far less volatility than the red line.

We could say that red has been a more volatile asset than grey over this time period, and indeed we can measure this. If the market believes this high volatility is likely to continue, this will translate into higher option prices. Before we discuss the relationship between option prices and volatility though, it’s important to define some different types of volatility, which we will do next.