Most Altcoins do not meet Howey Test’s Criteria.

The SEC’s lawsuit against Binance and Coinbase undoubtedly increases the regulatory risk of the crypto market. Still, the regulatory risk is mainly concentrated on altcoins investors, which has a limited impact on holders who only hold BTC and ETH.

However, Once the SEC lawsuit is successful, all altcoins may be recognized as securities and need to be regulated by securities standards, which means that the trading of altcoins will be more offshore and decentralized. Moreover, liquidity will be more concentrated in BTC, ETH, and other mainstream cryptos.

Author: Matt Hu

“This Glass of Water Is Like Security”

As an emerging global market, regulatory authorities and their actions have never been lacking in the crypto market. Whether to control a series of risks contained in it or for other purposes, the regulatory authorities of various countries hope to gain some voice over the crypto market through supervision.

The frequent actions of the regulatory authorities have also become one of the critical sources of additional uncertainty in the crypto market. The regulatory in May 2021 interrupted the last bull market for nearly two months, and in 2023, the regulatory storm seems to be coming back – this time by the SEC.

Before the SEC took action, the CFTC had already sued some exchanges for “violations.” In the indictment, the CFTC accused the exchange of providing derivatives trading services without registration and assisting customers in evading regulation. This does not appear to have impacted investors; they can trade on compliance or offshore platforms. Money in the crypto market is global and comes and goes as it pleases.

The SEC’s indictment adds perhaps the most significant element to the previous list: the illegal offering and sale of unregistered securities and financial products by certain exchanges. At worst, the charges against the exchanges will push investors to withdraw their funds or move to other exchanges. However, the charge of “unregistered securities and financial products” means that the SEC treats token assets held by users, especially altcoins, as “unregistered securities” and cannot list or sell them on exchanges and trading platforms. A total of 68 tokens have been recognized as securities by the SEC , including all categories from public chain tokens, exchange tokens, and project tokens – except for BTC and ETH.

Wow, that is not a small case. Let’s think about the possible consequences of a successful SEC prosecution:

- The SEC has gained regulatory authority over tokens other than BTC and ETH. “The 68 tokens being recognized as securities” is just the beginning. Any other tokens intended to be listed on CEXes or already traded on the DEXes may be compared by the SEC to these 68 tokens and considered “securities” based on their similar properties to these tokens, requiring them to be regulated.

- Any trading platform with US operations may be sued and fined for listing certain “non-compliant” tokens. Even if these trading platforms are offshore, the SEC may invoke previous successful litigation cases to enforce financial sanctions against them.

- Due to “compliance requirements,” centralized exchanges may choose to strictly review the publishing of tokens or abandon altcoins to obey the requirements, making financing through ICO/IEO more difficult.

In fact, the SEC’s battle for the crypto market regulation power may not stop there. In 2018, MIT professor Gensler said ETH is “not a security.” Still, in April 2023, SEC chair Gensler stated that “most crypto assets are securities” and refused to answer “whether ETH is a security.” Considering that the CME has been listed ETH futures and options for a long time, Gensler and the SEC may not make a statement in the short term, but once more support is received, the SEC will not rule out the possibility of identifying ETH and even BTC as securities. After all, even the business of selling oranges needs to register with the SEC.

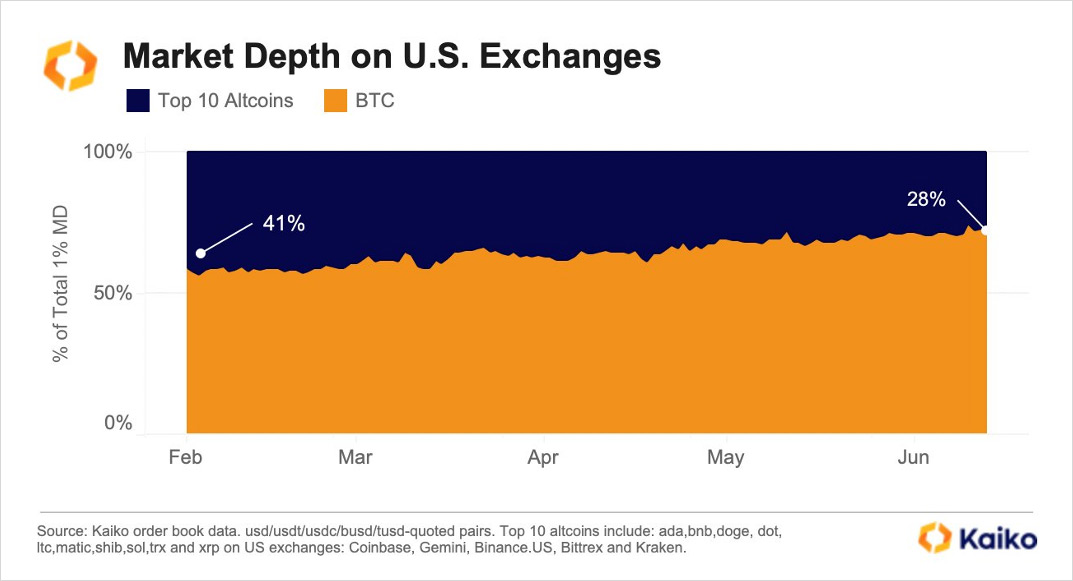

But regardless of whether altcoins are securities, the SEC’s lawsuit has significantly impacted the crypto market. Online trading platforms such as Robinhood have announced the delisting of altcoins identified as “securities” in the SEC indictment, triggering panic selling by investors. Market makers have chosen to withdraw liquidity from the altcoins and US crypto markets under the threat of compliance risks. As a result, the market depth available to US retail investors has dropped by a quarter in just one week.

Market depth changes of altcoins and BTC of US crypto exchanges from Feb to Jun 2023. Source: Kaiko

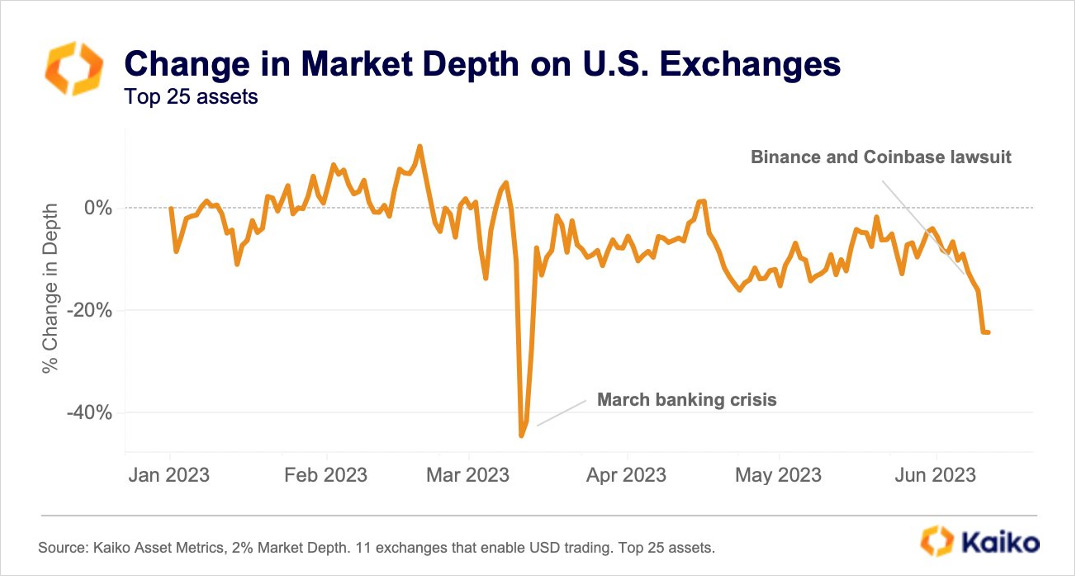

Changes in market depth of US crypto exchanges since the beginning of 2023. Source: Kaiko

Although BTC and ETH have not been recognized as “securities” for now, and have become “safe havens” for liquidity from altcoins, are altcoins securities? Let’s use the SEC’s criteria for determining securities to make a quick judgment.

Is This Glass of Water a Security?

The SEC’s standard for determining “whether a product is a security” dates back 77 years to 1946. Let’s leave aside the rationality of the standard established before all modern financial products; the law is the law.

The criterion is named the “Howey Test” — the name comes from the SEC’s lawsuit against a company that makes a living buying and selling oranges. In the lawsuit, the SEC determined that the company’s “citrus planting agency contract” was an “investment contract” that met securities standards and should be regulated. To illustrate, then-Justice Frank Murphy established the following criteria to define “security”:

- Investment of Money: The buyer should provide funds to the project initiator through cash as a form of consideration.

- Common Enterprise: The wealth of each investor is tied to the fate of other investors, usually combined with the proportional distribution of profits. Whether investors can obtain benefits depends on the efforts of the project initiator. The benefits of investors and the efforts of others are combined with the final operating results.

- Expectation of Profit: The “profit” here can be the capital appreciation generated by the initial investment or business operation or the income generated using the funds provided by the buyer. The appreciation caused by external factors such as the general inflation trend or economic development affecting the supply and demand of underlying assets does not belong to “profit.”

- Derived From The Efforts of Others: The project initiator, organizer, or other related third party has made necessary management efforts, and this effort will critically affect the success of the business. Investors only need to pay the specified fees and costs and do not actually participate in the operation and management of the project.

Let’s use this framework to judge crypto.

The trading and settlement of cryptocurrencies are usually conducted in BTC, ETH, and stablecoins and are sometimes anchored to other tokens. BTC and ETH are not cash; stablecoins are not sovereign currencies issued based on national credit but synthetic targets based on underlying assets such as bonds, more like the existence of “banknotes.” Therefore, this does not meet the definition of “investment of money”.

So, will investors who purchase cryptocurrencies receive dividends? Unlike securities in the usual sense, cryptocurrencies do not provide dividends. Crypto holders may have voting rights or some discounts. In addition, due to decentralization, the benefits obtained by investors are not necessarily related to the efforts of the project initiator or the final operating results. “Emotion” and “speculation” may have a relatively greater impact on investment returns. Perhaps some attributes of cryptocurrencies are linked to “common enterprise,” but most cryptos do not have such features.

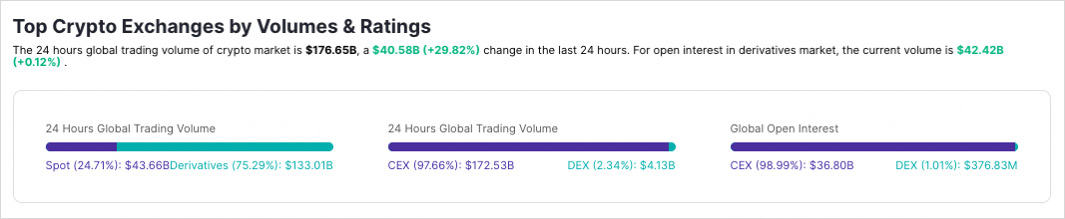

From the perspective of expected returns, most altcoin investors get their returns from external factors, such as tokens being listed on major exchanges, market recognition of new concepts or narratives, and even the discovery of speculative opportunities rather than initial investments and business operations. The impact of market makers on investor returns cannot be ignored. As of June 2023, the proportion of derivatives trading volume in the crypto market has exceeded 75% of the total trading volume, and the market-making and hedging behavior of derivative market makers has a continuous and significant impact on prices. Compared with this, “the efforts of project operators” are not even the main influencing factor.

Comparison of the total in-house spot trading volume and derivatives trading volume. Source: TokenInsight

Similarly, because most of the factors that affect altcoin returns come from external factors (macro liquidity, emotion, speculation, etc.), the management of project initiators, organizers, and affiliates may not play a critical role. In addition, since the operation of the crypto community usually adopts the DAO model, investors holding altcoins have the right to participate in the operation and management of the project.

In fact, investors play a key role in the operation and management of the project: community voting by token holders will directly determine the future of the project, and anonymous developers and contributors from the community have made indelible contributions to the operation and maintenance of various projects, and these people are investors and participants in the project. The success or failure of the project depends on the community’s joint efforts, and of course, the impact of the macro environment cannot be ignored. Still, it can be sure that the crypto market will not develop to its current level only through the efforts of project initiators.

Therefore, altcoins seem like “securities”; however, most altcoins do not meet Howey Test’s criteria. Perhaps some altcoins can be judged as “partially meeting Howey Test,” but this cannot define them as securities. The genetic similarity between humans and corn is close to 50%; however, it is evident that humans are not corn.

If Water Is Eventually Recognized as a Security…

Although we have proven through many facts that “altcoin is probably not a security,” we must prepare for the worst.

If the SEC ultimately prevails (which may take several years or even a decade), altcoin issuers and liquidity providers will face unprecedented difficulties. Before passing a Howey test, the US financial and banking systems will not provide services to high-compliance-risk clients represented by web3 project teams; they must choose other systems. In addition, even if the project’s tokens are temporarily not considered securities, compliance issues will still accompany a series of links such as token issuance and trading.

Places like Hong Kong, Dubai, and South Korea may be viable choices; the regulatory authorities in these places are more friendly to the crypto market. However, compared with the U.S. market, the service level and financing scale that can be provided by regions such as Hong Kong still have a lot of room for development. However, the replacement of financing channels is undoubtedly a good thing for the landing place. For the crypto market, this means “internal rebalancing”; the dominant position of North America in the crypto market may be weakened.

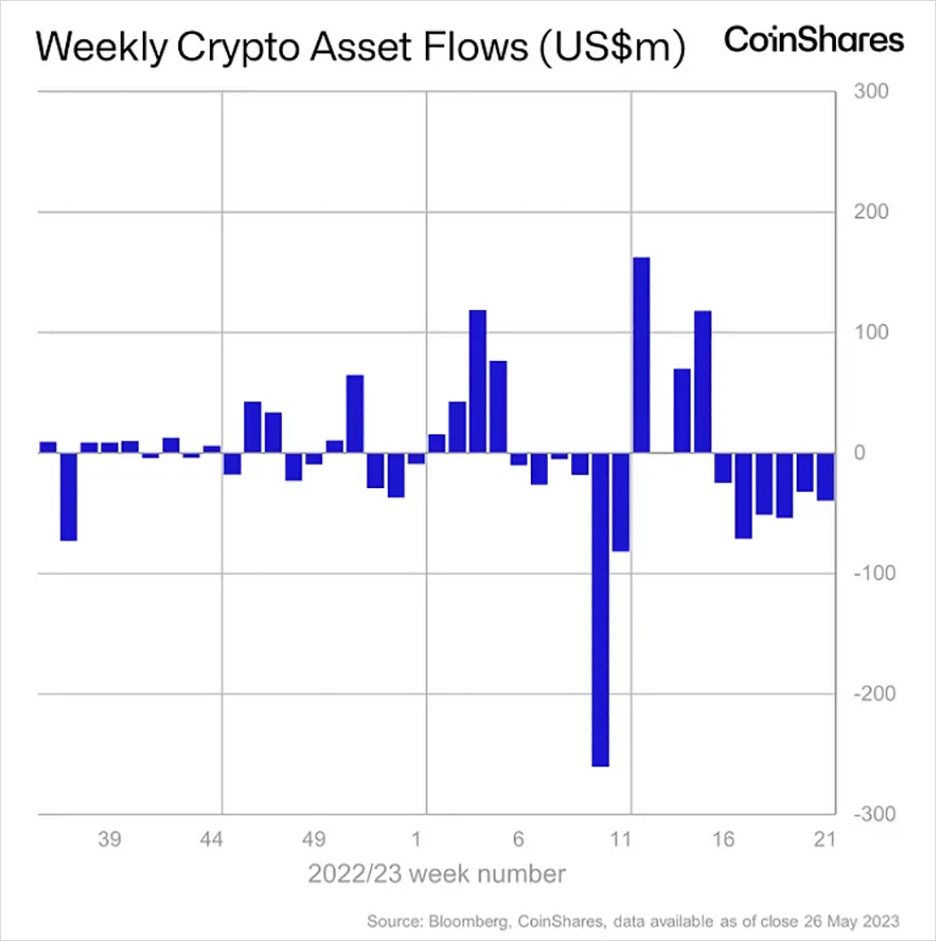

For another important participant in the crypto market – asset management institutions, the altcoin investment portfolio that once brought them considerable returns has become a “hot potato.” Leaving aside the losses caused by high volatility, compliance risks alone can make them decisively choose to close all altcoin positions. In fact, after the SEC’s lawsuit, investors have withdrawn from fund managers who manage altcoins; some altcoins portfolios lost 65% of assets under management (AUM) within a week, and the weekly outflow scale of funds from major crypto asset management institutions has reached $39m.

Fund netflow of crypto asset management products. Source: CoinShares

Of course, institutions will not necessarily give up altcoins. Holding OTC return swaps on altcoins does not violate compliance requirements (as long as the counterparty agrees); likewise, having index futures and options on altcoins is a viable option. It can be expected that for some crypto-regulatory friendly areas, altcoin-related indices and derivatives seem profitable. However, before this happens, altcoins may temporarily “retreat behind the scenes” in institutional portfolios – this is difficult to avoid.

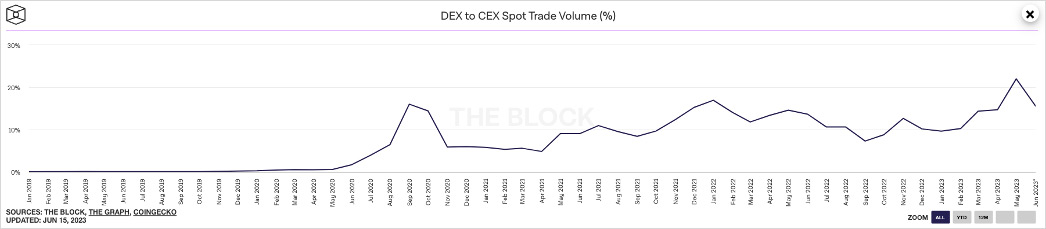

Comparison of decentralized and centralized exchanges’ spot trading volume, as of June 2023. Source: The Block

For retail investors, compliance does not seem to be a problem; they are more willing to hold crypto assets rather than bank accounts. Therefore, for retail investors, offshore and on-chain markets are acceptable; they can trade anywhere. Retail investors have actually been voting with their feet; additional regulatory risks for centralized exchanges are pushing investors towards decentralized exchanges. With more regulation events, we may witness further development of on-chain markets.

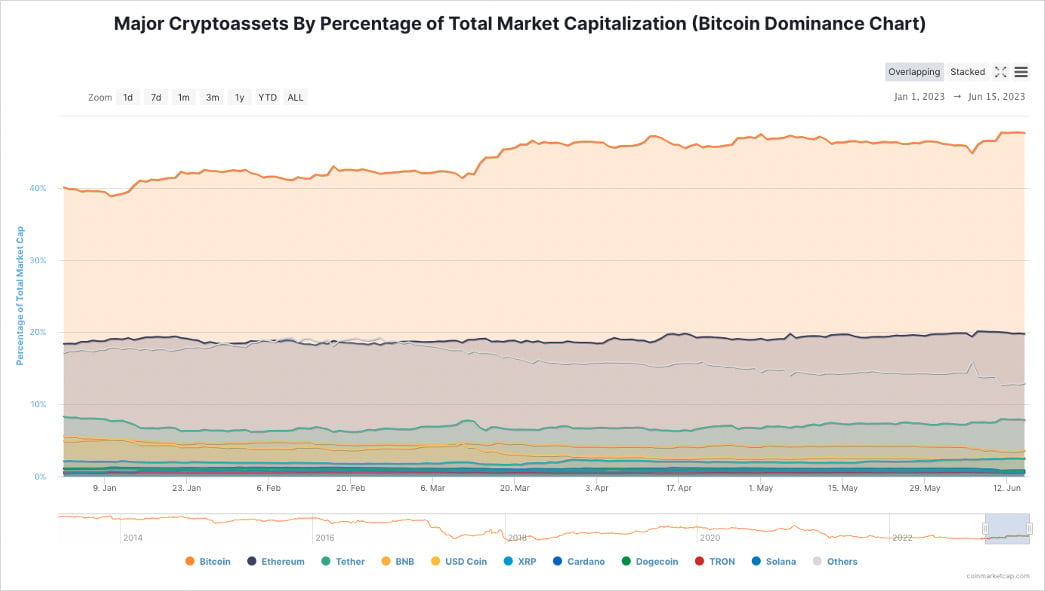

Changes in market share of major crypto assets, as of June 2023. Source: Coinmarketcap

But overall, regardless of whether altcoins are securities or not, the impact of risk aversion is long-term. Although institutions and retail investors have a variety of channels to avoid compliance risks, compliance itself is a risk—it protects investors while increasing the trading costs of all investors, and the consequences are already beginning to show. Retail investors and institutions are regaining their preference for BTC and ETH, while altcoins are being neglected, and their share continues to shrink.

In addition, the crypto market’s liquidity pressure is increasing in the current macro environment. BTC, ETH, and stablecoins are currently the safest liquidity destinations for crypto investors. The altcoin bear market may last long, and we must be prepared for it.