Familiar Ranges Prevail

Bitcoin has held up above the $42,000 threshold, even in the wake of the initial ‘sell the news’ event tied to the launch of Bitcoin ETFs. The brief dip below $40,000 reflected the market’s recalibration in response to an increased supply following the transition of the GBTC product to a spot ETF.

Notably, the outflows from Grayscale are waning, overshadowed by substantial inflows into the other 9 new ETFs. In the previous week, Bitcoin ETFs experienced a net positive influx of $701m, a figure that comfortably eclipsed Grayscale’s $600 million outflow, thanks to $1.3b in fresh ETF capital.

That said, there may be some immediate price risks for Bitcoin, particularly with the potential liquidation of assets by Celsius and Genesis. An upcoming court hearing on February 8 may greenlight Genesis’s sale of $1.4 billion worth of GBTC, and Gemini’s potential sale of $1.2 billion worth of GBTC collateral, which constitutes a notable risk for the market this week. Furthermore, the initiation of $3 billion worth of crypto distributions by Celsius might also place downward pressure.

From a fundamental standpoint, the outperformance of the US dollar is expected to persist as the Fed is unlikely to implement rate cuts before May or June. This forecast was reinforced by the strong US jobs data released last Friday, and also by Fed Chair Powell’s comments at the recent FOMC press briefing and on ’60 Minutes’ indicating a delay in rate cuts.

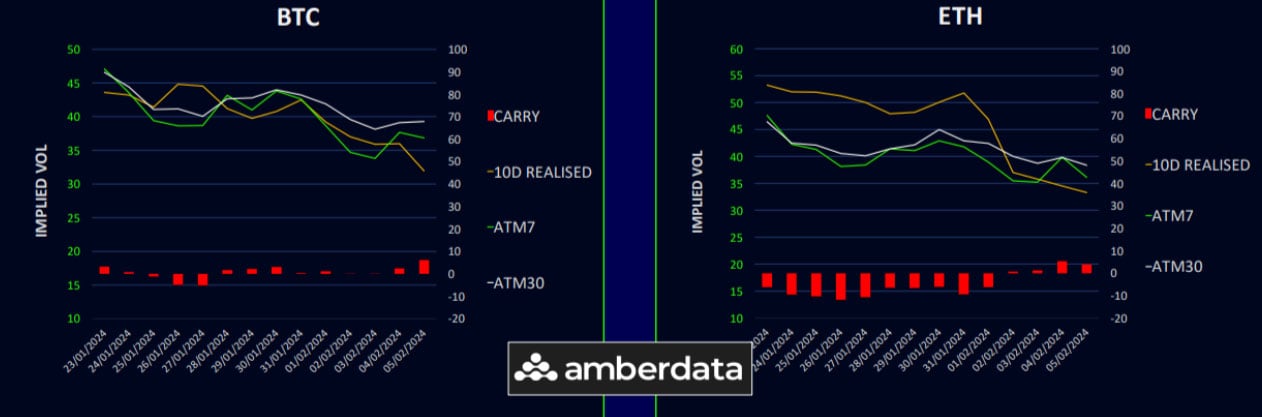

Realized Volatility Falling Fast

Cryptocurrency volatility has subsided this week, with market prices stabilizing and lacking major news to stimulate movement. Implied volatilities dipped but have now levelled off. With volatility carry at median levels, there’s still appeal for gamma selling.

Ethereum’s movement has remained rather restricted, likely due to call selling and dealer gamma exposure, suggesting a continued focus on theta harvesting until a market catalyst occurs. Bitcoin’s neutral position faces potential impact from Celsius liquidations, which could trigger some downside volatility.

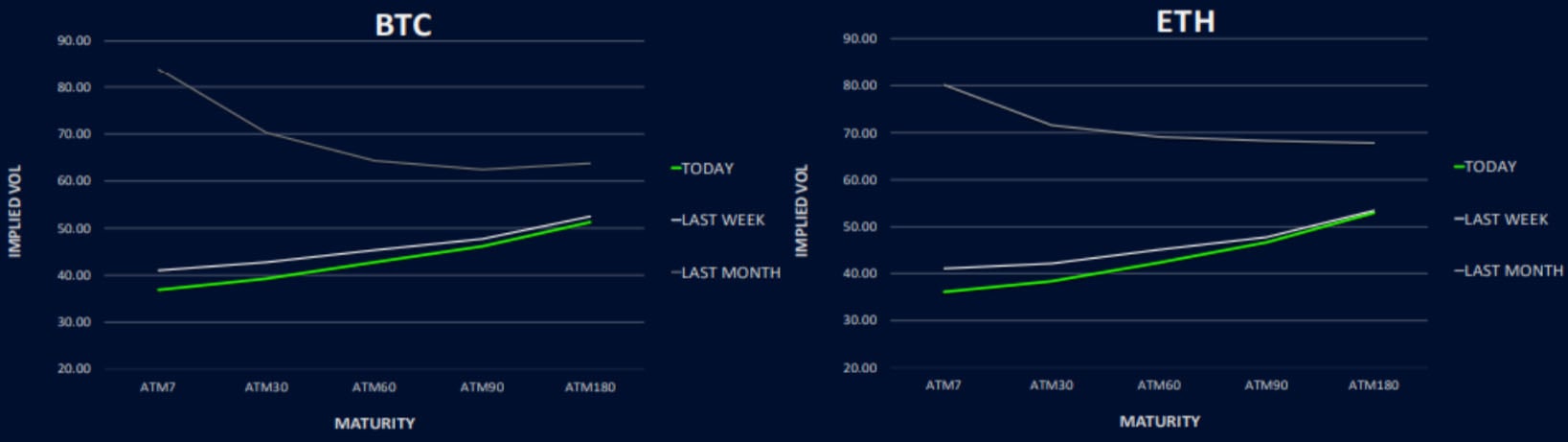

Front-End Vols Hit Hardest

Bitcoin’s term structure is falling deeper into contango, with a notable drop in front-end volatilities and minor declines at the curve’s long end. Concerns over Celsius and Genesis distributions have reintroduced front-end put skew due to anticipated near-term weakness.

Ethereum’s term structure is also steepening with lower front-end volatility. Implied volatilities are fast approaching their lows as excitement over ETFs wanes and the market finds equilibrium.

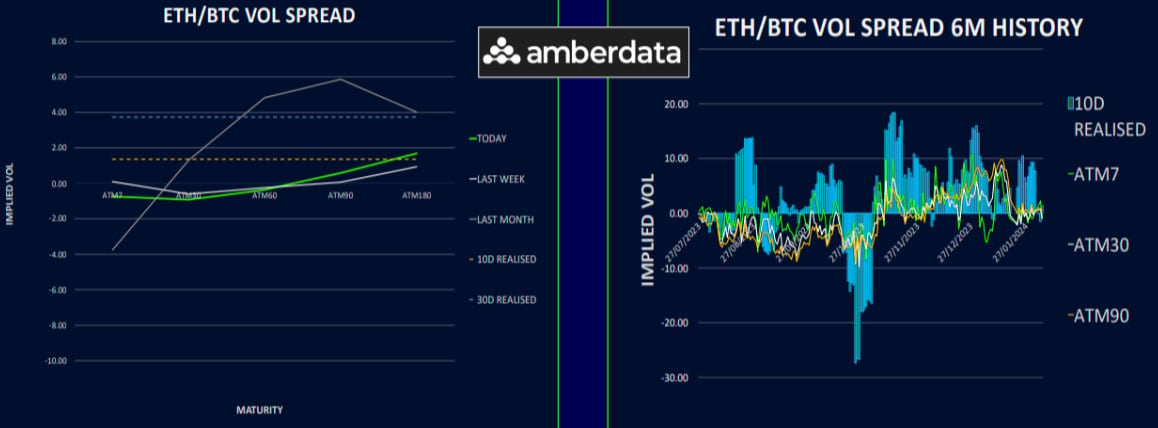

Owning ETH/BTC Vol Spread Long-Term Makes Sense

The volatility spread between Ethereum and Bitcoin is neutral short-term but slightly favours Ethereum in the long-term. The dampening effect of Ethereum’s long gamma positioning is visible, as both assets have been trading in tighter ranges.

Owning the long-term vol spread – favouring Ethereum over Bitcoin – remains the way to go in our opinion, though short-term conditions could lead to a Bitcoin vol premium due to ETH overwriting supply, higher BTC short-term realized vol due to bankruptcy liquidations and the halving effect on BTC.

Hence, trading calendar spread switches between the two could be a sensible move. Another way of thinking about this is saying you want to own the ‘forward’ vol spread ETH/BTC which is a VEGA trade, rather than spot starting, which has GAMMA (realized vol) exposure.

We explain the difference between the Greeks in detail in our options trading courses. See here for more details on our education products.

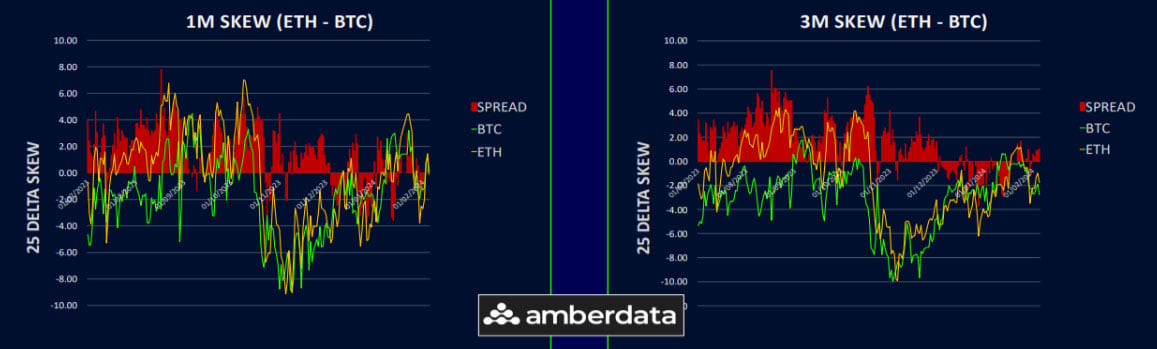

Short-Dated Put Skew Returns

Bitcoin’s spot retracement from recent highs has revived short-dated put skew interest, particularly for the Feb24 expiry, indicating hedging against potential GBTC supply from Celsius and Genesis distributions. In longer maturities beyond 1 month, a call skew persists, with both Bitcoin and Ethereum’s skew term structures showing almost identical call premium.

Ethereum’s ongoing call selling (moving out to March 24) is likely to cap front-end call skew, and since we still think the headlines are more likely to come from BTC in the near term, it suggests short- term hedging strategies may favour selling Ethereum calls to fund protection trades.

Option Flows And Dealer Gamma Positioning

Bitcoin option volumes rose by 10%, with calls prevailing, evidenced by a large Feb24/Apr24 strangle swap and the buying of March 50k calls. Ethereum’s volume was up by 12%, also call-dominated, including significant trades covering short positions in Feb24 as the premium got very low and rolling out shorts into Mar24 via call flys and credit put spreads.

Dealer gamma positions for Bitcoin remains balanced, while Ethereum’s is still heavily long due to significant on-screen call selling, potentially muting volatility until a fundamental market shift occurs.

Strategy Compass: Where Does The Opportunity Lie?

A seasonal pattern around Chinese New Year (thanks to 10x research) was flagged in BTC, and this has the potential to bring a 5-10% rally over the next couple of weeks. We think using 23Feb BTC call spreads or ladders is a nice way to play such a bullish short-term scenario. Details of the strikes we picked are reserved for our subscribers.

To get full access to Options Insight Research including our proprietary crypto volatility dashboards, options flows, gamma positioning analysis, crypto stocks screener and much more, Visit Options Insights here.

Disclaimer

This article reflects the personal views of its author, not Deribit or its affiliates. Deribit has neither reviewed nor endorsed its content.

Deribit does not offer investment advice or endorsements. The information herein is informational and shouldn’t be seen as financial advice. Always do your own research and consult professionals before investing.

Financial investments carry risks, including capital loss. Neither Deribit nor the article’s author assumes liability for decisions based on this content.

AUTHOR(S)

Imran Lakha is an expert at using institutional options strategies to capitalize on investment opportunities across global macro asset classes. Learn more here.