Buying a call option gives the holder the right to buy the underlying asset, at the strike price, on the expiry date. The option buyer pays a premium for this right, so why not just buy the underlying directly in the first place?

The two main reasons are the fixed risk, and the considerably smaller initial outlay, that a long call option position provides.

Fixed risk

As we’ve mentioned a couple of times already in this section, buying a call option has a fixed risk. The maximum amount the trader can lose is the premium they pay for the option.

Let’s take a look at how the profit/loss of a call option compares to buying the underlying asset directly. By doing this we can deduce some of the pros and cons of each.

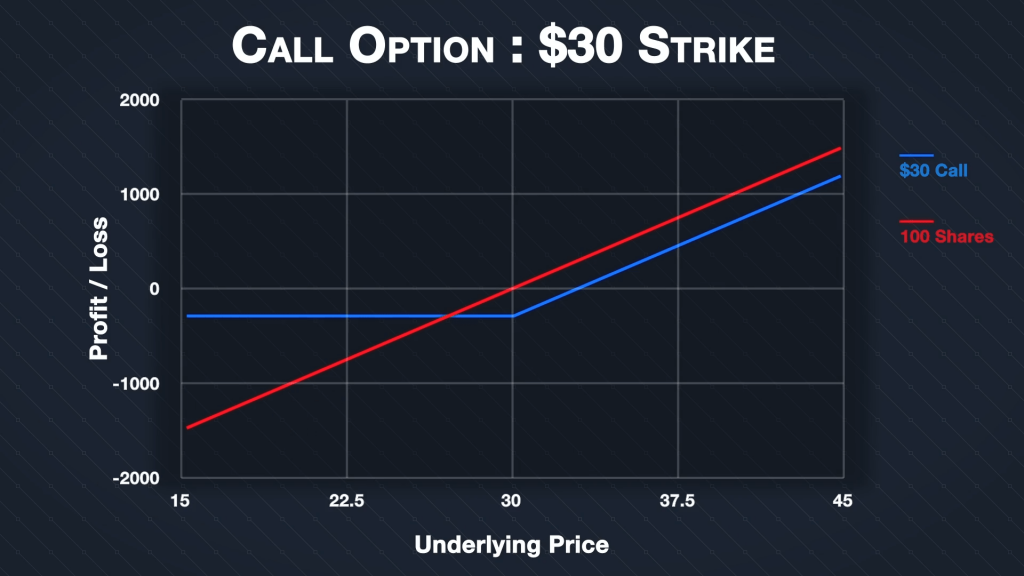

Suppose a stock is trading at $30, and there is a call option for this stock with a strike price also of $30. This call option has a price of $3 per share. This chart shows the profit and loss of the call option at expiration (in blue), and of purchasing 100 shares of the underlying directly (in red).

Purchasing the stock directly leads to this straight line (in red) which continues all the way back to zero to the downside, and off to infinity to the upside. If you own 100 shares, every dollar increase in the underlying price will give you a profit of $100. And there is no cap on this as the price increases. Similarly though, every dollar decrease in the underlying price will give you a $100 loss. The only cap on this is if the price falls to zero, which would result in you losing the full value of the shares you purchased. In this instance as you bought 100 shares at $30 each, if the shares become worthless, you could lose the full $3,000 you paid for them.

Let’s compare this to the call option in blue. As you can see, to the upside, the payoff is very similar to purchasing the 100 shares. The difference being that as $300 of premium was paid for the option, the profit is $300 less at every point above the $30 strike price. So far it’s not looking favourable for the call option, but now look at what happens when the underlying price decreases. The losses of the call option position are limited to the $300 premium paid, no matter what happens to the underlying price. Even if the price goes to zero, the loss is still only $300. Compare that to the $3,000 potential loss of buying the stock outright, and it’s a clear advantage for the call option.

The point at which these two lines intersect is $27. This can be calculated as the current stock price of $30, minus the premium per share of $3 paid for the option. It’s at this point that the call option would have exactly the same profit/loss as owning the shares. For any point to the left of this, it would be much more beneficial to have the call option rather than the shares. For any point to the right of this, it is a little more profitable to be holding the shares, but both gain from all further price increases.

In other words, by opting for the call option instead of buying the shares initially, you’re sacrificing a small fixed amount of your potential profit, for the guarantee that you can’t lose more than the amount you pay for the option.

Lower cost

The total cost of purchasing 100 shares at $30 a share is $3,000. Unless the platform you’re using offers some leverage, you will need the whole $3,000 to open the position. This is ten times more than is needed to buy the call option.

At a $3 premium per share, the total cost for the call option is only $300, so this is all you would need in your account. This allows you to gain very similar exposure to any price increases, but without tying up anywhere near as much capital.

The effect of time

As well as the premium that is paid for the call option, there is one major disadvantage worth mentioning, and that’s the inherent time limit that an option has. If the expiry date is reached and price has failed to increase, the option will expire worthless and result in a loss for the trader. To regain exposure to price increases they would need to buy another call option and pay a new premium for it. Whereas a trader who initially purchased the 100 shares instead could simply continue to hold them with no extra cost.

So when purchasing a call option, there is more pressure to be correct about the timing of the move as well, not just the direction.

The rate at which an option loses value over time is called the Theta, which is quite an expansive subject just in itself, so there is an entire section on it later in the course.

In summary

Buying an asset directly can require a lot of capital, and also has the potential for large losses if the price of the asset decreases significantly.

Buying a call option will usually require significantly less capital. The maximum loss of a long call option is also fixed to the premium paid.

These properties make call options ideal for traders who want to limit their risk, while still participating in almost all of any increases in the underlying price.

The costs of gaining these attractive properties are the premium paid for the option, and the inherent time limit the option trade has to work.