Markets are mechanisms where people can exchange goods and services with each other. Even though all participants have only their own self-interest in mind, price discovery allows markets to efficiently allocate resources to their highest value use in society.

The speed and accuracy with which markets can process information can be observed from the following example. In 1986, the Space Shuttle Challenger exploded right after takeoff, killing all seven crew members. Two economists, Maloney and Mulherin, studied the stock market reaction to this event and found that it took the market minutes to pinpoint Morton Thiokol — the vendor responsible for the booster rockets — as the guilty party. (A feat that took the official government commission five months to complete.)

In an efficient market, prices reflect all available information. As a result, market prices have an immense predictive power. We can confirm this by looking at the inverse: If someone possessed information that a particular event will deviate significantly from the market’s current view, he could trade on it until the opportunity went away. Because of that predictive power, more and more people consult market prices for a “no-bullshit” view on the likelihood of future events.

Prediction markets

The appreciation for market mechanisms in combination with wisdom of the crowds has birthed the idea of prediction markets (PM). In a prediction market, users can buy and sell contracts that resolve on the outcome of real world events. All contracts are binary in nature, meaning they resolve either to 100% (e.g. a particular event happens) or 0% (it doesn’t). They often use a contract size of $1, so the market price of a particular share can easily be read as the likelihood that this particular share will pay out.

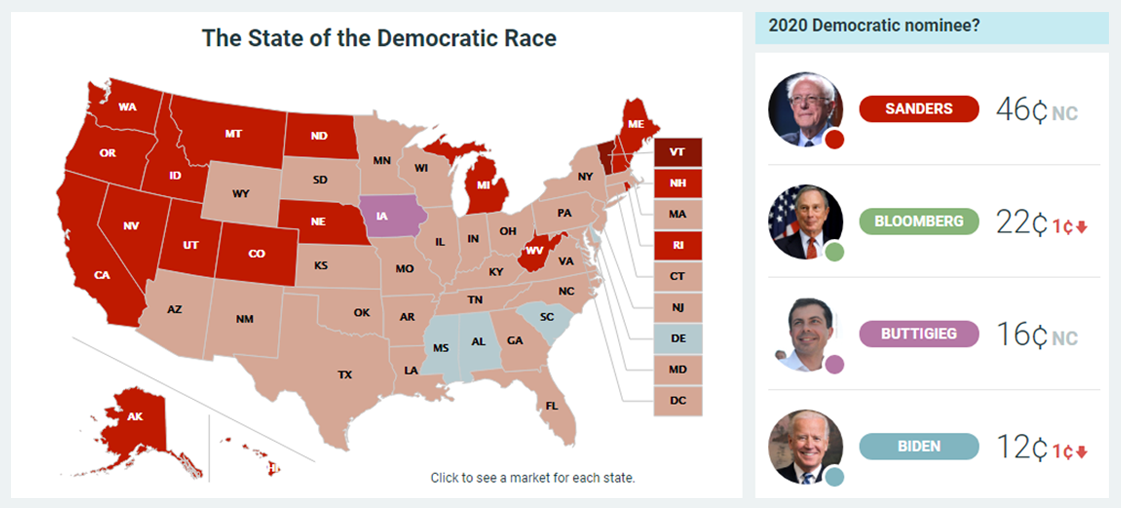

In this example from PredictIt, the market puts Bernie Sanders’ chance to become the Democratic nominee at 46 cents on the dollar, or 46%. Traders who think the real likelihood is higher or lower could buy “yes” or “no” shares to pocket the difference between the market price and the real value of the contract.

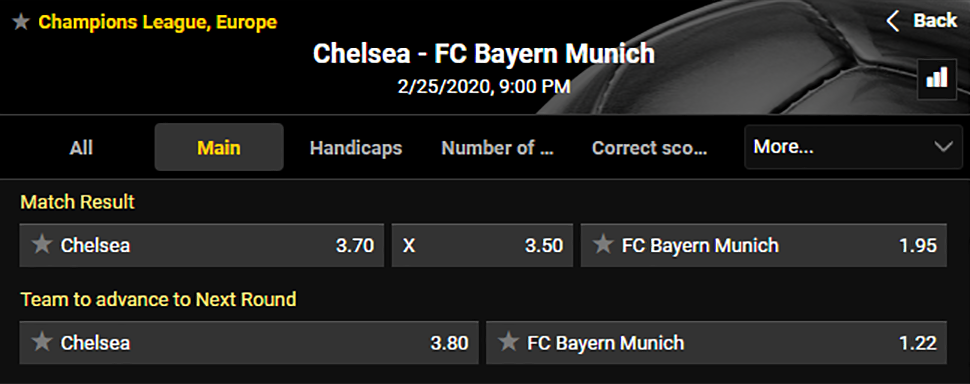

Source: bwin.com

A more popular, but less commonly cited form of PM is the sports betting market where participants place binary bets on the outcomes of sporting events. In this case, bwin displays the odds in the decimal format, which shows the payout from a successful bet. According to the above odds, a successful bet on Chelsea pays out $3.70 on the dollar, a draw pays out $3.50, and a win for Munich pays out $1.95. These payouts convert to a probability distribution of 27%, 29%, and 51% respectively.

It’s no coincidence these outcomes map to more than 100% because of bwin’s profit margin. PredictIt, on the other hand, shaves their 10% fee off any resolved bet and charges users another 5% for withdrawals.

The mechanism by which these markets can accurately predict the outcomes of real-world events is always the same: the uncoordinated behavior of market participants, each acting on their own private information to make a profit, can lead to the emergence of information that none of them possesses individually.

PMs for world peace?

This information leads some economists and futurists to dream how much more “efficient” societal decision-making could be, if only we had prediction market information for more real-world events. The pinnacle of that ideal is futarchy, a form of governance where decisions are made based on the outcomes of such prediction markets. But if their outputs are so useful, why are they not popular in the real world?

Fans of PMs are quick to bring up problems with government regulation, but the more simple explanation is that bettors have simply no interest in betting on most outcomes. Markets don’t exist to create accurate price predictions. Instead, the predictions are a positive externality of market activity, not the goal for participants themselves. If market participants were motivated by the predictions, they should simply wait and observe the trading of others, instead of engaging in costly trading themselves.

My impression is that most people who vocally support the idea of generalized prediction markets do so from the perspective of a market watcher, not a bettor. They want to benefit from the positive externalities — market prices — without giving up anything in return. But by doing that they forget that markets produce accurate predictions as a result of participants following their own self-interest, not to please economists and market watchers.

How prices are formed

To understand why most markets will never see any meaningful liquidity, it helps to understand how efficient markets work. For prices to reflect available information, two things need to happen. First, someone needs to unearth a piece of private information about a particular real world event. And second, that person needs to place a bet to act on his private information.

Both the act of getting the information and the act of taking the position (paying a fee and locking up capital for an extended period of time) have a significant real-world cost. Unless bettors are compensated for that cost, no betting will take place and the price will not move. That means no information is being priced in either.

The incentive for profit-driven market participants to discover and act on new information has to come from somewhere. Usually, it comes from market participants who are willing to bet at a price that is worse than the fair market price. In other words, they pay for someone to take the other side.

There are many valid reasons to pay for liquidity. In the example of sports betting, users might feel that betting on their favorite team enhances their viewing experience and are willing to take a small loss for that. The equivalent in financial markets are so-called noise traders, who buy and sell without any fundamental reason to trade. The poker equivalent of both of them is the fish, without whom no game can take place.

A commercially valid use case is the transfer of risk. For example, wheat producers are natural sellers of wheat futures to hedge the risk of falling prices. These wheat futures might be bought by industrial consumers of wheat, who want to hedge against rising prices. In many cases, betting markets allow the transfer of risk from market participants who don’t want it to those who do.

In either case, there exist parties who create an overlay that attracts professional bettors to provide liquidity.

Can the general PM be saved?

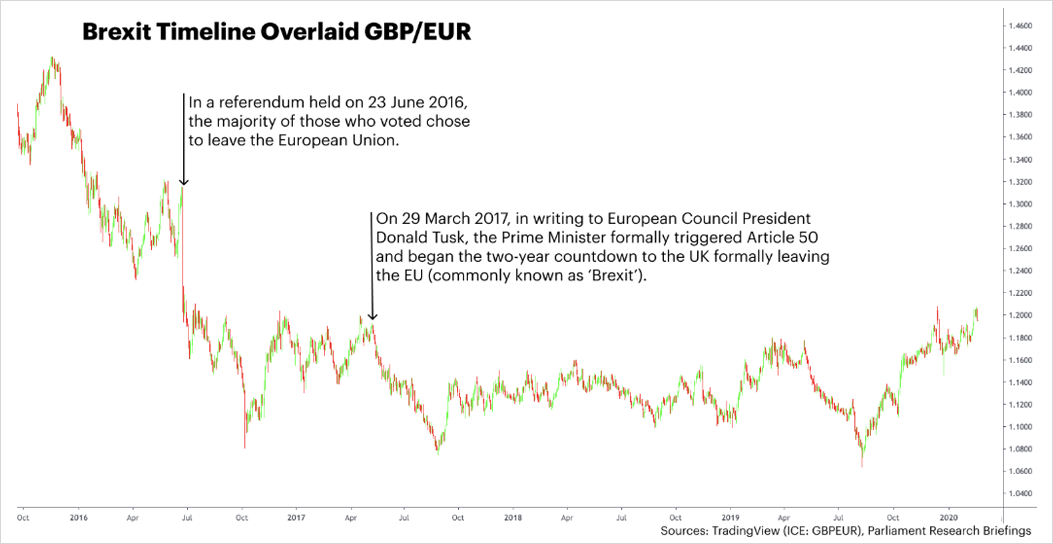

It is futile to expect overlays to form naturally in markets where there’s little natural liquidity, either because participants have no commercial reason to buy or sell risk, or because they are unwilling to gamble at a loss. That pretty much restricts PMs to markets that are already highly liquid today: sports, finance, and politics. Even for events that should lend themselves well to prediction markets, bettors are often better off using other options. For example, a bettor who might think Brexit will happen could have shorted GBP vs EUR in the forex markets.

GBP fell against EUR months before the referendum as market participants took a bet on Brexit.

Source: Mike Co

But all may not be lost, as we can borrow mechanisms from other systems like poker. In poker, each person has some private information (their hole cards) and they can make bets on their belief about the strength of their hand relative to the hands of other people. But if you changed the game by removing the forced bets that all players make before the game begins (called blinds and antes), then the correct strategy for each individual player would be not to play — the exact outcome we see with prediction markets today.

The reason that poker hands take place in practice is that there is already an overlay in the pot that makes future bets profitable. So some player will open the action and say “I’ll bet you $10 that I win this pot of $10”, and then another player might say “Hold on. I also have a good hand. I’ll bet you $20 that I win this pot of $20” and so on.

Overlays are also used to bootstrap poker tournaments, as people generally don’t want to play in illiquid tournaments. Initially, the tournament organizer steps up and guarantees a minimum prize pool of, say, $100k. Suddenly, it is no longer bad to sign up early. In fact, the fewer players are signed up, the more profitable it is to join. So more and more players join until the guarantee is filled and the overlay is not even in play any longer.

The mechanism of deliberate overlays is missing from the current iteration of prediction markets. In order to bootstrap liquidity, they must reward participants for betting.

Conclusion

If prediction markets want to survive, they need to realize that all markets need an overlay in the form of a) commercially viable use cases, or b) for a lack of a better word, fish. Most markets will never have either, as most people have not shown an inclination to bet on events other than sports, finance, and politics, and that is unlikely to change.

So they can either optimize for the markets that are proven to work, in which case they will discover that competition in these markets is strong and entrenched, and optimized to offer the best experience for particular types of markets (e.g. sports betting.)

Or, they insist on creating more general markets (and thereby primarily serve market watchers and economists instead of the actual bettors). In that case, they may need to start paying bettors with manual overlays, similar to how poker tournaments reward their early liquidity providers. Pricing in information is costly, and someone has to foot the bill.

AUTHOR(S)

Crypto researcher writing w/@zhusu for @DeribitInsights and uncommoncore.co, podcast: uncommoncore.co/podcast/