“___ has closed another fund at $___ billion dollars as it seeks to continue investing in the world of cryptocurrency and Web3”

If you’ve followed any sort of financial news in the past two years, chances are you’ve seen headlines like this week after week and month after month. At face value, it’s obvious that this type of investing and capital allocation is a signal of value in a new industry and reaffirms a strong bid for crypto. Yet there is a large story that is essentially ignored whenever an investment firm has raised and deployed capital into projects within the space. Through an examination of the early days of traditional venture capital, comparisons to that era in time, and an understanding of crypto markets, we’ll be able to explain the implicit bet that venture capital firms are making in the future of crypto asset prices.

The Early Days

To explore this topic further, one must first look back in time to the earliest days of modern venture investing and the then nascent landscape of technology and the internet. The “Dot Com” era was known for the frenzy of retail buying and crazy stock surges in early technology companies, particularly in public markets but few people credit the craze to the earliest backers of these new technologies, venture capitalists.

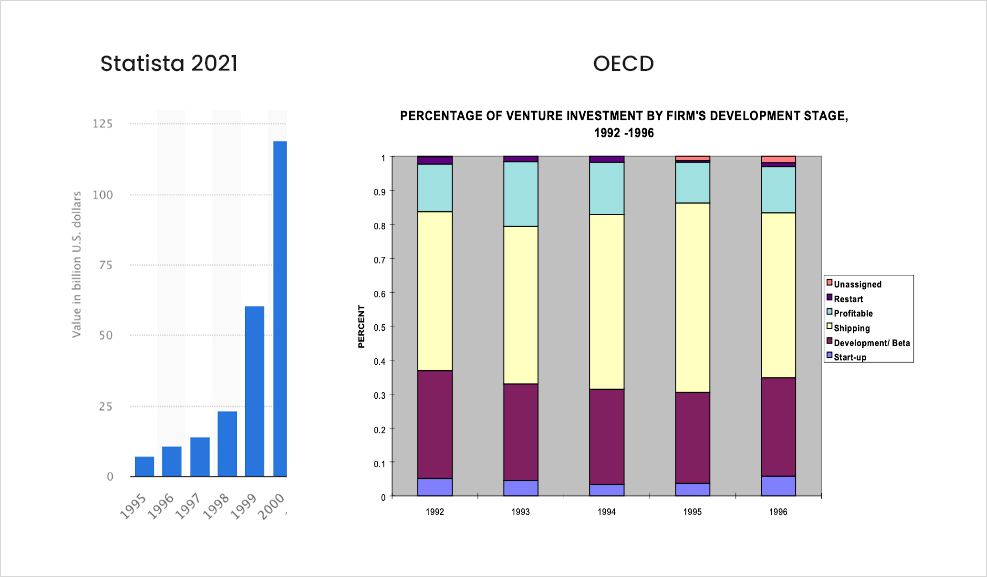

In the mid 1990s, venture capital was a tiny and relatively new form of investing, totalling to only $7.6 billion1 in deployed capital (less than 5% of the 2021 market size2). Even still, that tiny pool of capital ended up becoming the lifeblood of the technology revolution as nearly 70% of venture investing went towards technology / internet companies, most often in the late stage. The trend didn’t stop as subsequent years only saw more and more activity picking up for the venture capital space as investments in firms grew 10x from 1995 to 1999.

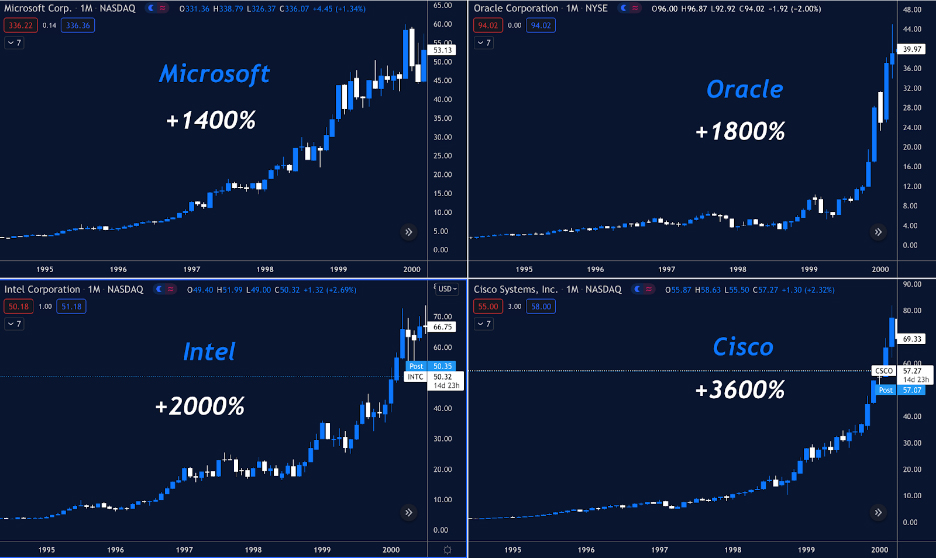

What happened next was no surprise. The next 5 years from 1995, saw a dramatic price increase in publicly traded technology companies, as the 4 largest of the era each netted more than 10x return, most of which lined up exactly at the same time as the largest venture raises.

Source: Tradingview

It’s no coincidence that the most significant growth in technology occurred in the era where private capital flooded the industry, rather it was this flurry of capital that pushed public market equities to their highs and allowed for the largest portion of the US economy to be built.

This time is different

In order to relate internet venture capital to crypto venture capital we must find the similarities and more importantly the differences between the two markets in order to understand the direct effect on crypto asset prices.

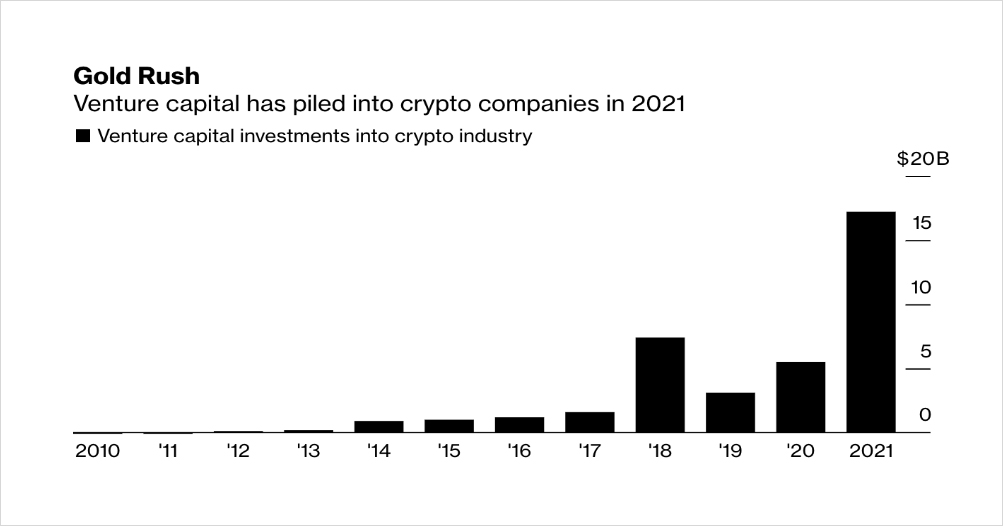

Source: Bloomberg

1) Similarities:

- Emerging markets: The most obvious similarity is the closeness of both industries and their relative bases. In many ways crypto is an extension of the same core technologies built 2 decades ago. In a similar manner the industries also share a very common group of early adopters as both had strong zealots leading early expansion and received a lot of skepticism in terms of their long term value.

- Speculation: As previously outlined, the early days of the internet received a lot of attention from venture capitalists. Both industries share this similarity as the crypto industry has recently become the leader in venture capital dealflow. Relative to their valuations, they also seem to be two sectors in history that (at their respective times) have been high risk, high reward bets.

2) Differences:

- Regulatory difficulties: The funding mechanisms for crypto assets and respective projects makes the investing profile very different as investors not only aim for equity deals but in most cases for token deals as is evident. In addition to this there is a huge disparity in being able to invest in the asset class as only venture capitalists can invest as opposed to traditional investors like asset managers, mutual funds, and general public equities. Because of the lack of clarity on crypto investments, there is now a smaller broad base of investors that can actively participate in token and equity deals.

- Shorter Liquidity Horizon: The quicker route to liquidity for founders, projects, and investors also changes the dynamics of funding cycles and the base expectation of the bets made in crypto projects. Capital moves a lot more freely and it is this capital movement that spurs the development of new ventures in the ecosystem.

- New valuation paradigm: The introduction of a new monetary system also changes the fundraising mechanism as projects, founders, and investors are paid in tokens / in-kind contributions as opposed to cash in traditional ventures. In addition to this, protocol / project performance is often generated by token prices as opposed to growth metrics as markets are much more liquid and comparables are available.

- Cult dedication: The average founder and investor ends up benchmarking their own performance in Bitcoin or Ethereum as their own base currency. Protocols that have raised millions and worked to become unicorns in a short period of time end up having employees retain their base currency and continually reinvest in projects and protocols within the ecosystem. Concentration is extremely high.

Levered long

It comes as no surprise that these very differences are in fact what causes a strange correlation to appear when venture capital firms look to purchase equity in crypto companies. When looking at any large venture-backed crypto firm’s prior growth rate, you’re able to quickly find that past projections are in fact a direct reflection of asset price appreciation in crypto. Consider this example:

The traditional venture firm / investor, “A+ Partners”, is looking for an investment in crypto. Unfortunately, A+ Partners cannot buy Bitcoin or Ethereum as their mandate doesn’t allow them to but they can buy equity stakes in organizations that focus on crypto. They choose to make an investment in a crypto exchange so they have to look at the revenue of the organization and what the future growth looks like. For exchanges, the entire revenue base comes almost entirely from trading activity. High trading activity is almost exclusively derived from high volumes and high volumes are almost exclusively derived from high asset prices.

Applying this line of thinking to a forward looking investment and we’re able to understand what top-tier venture capital groups imagine crypto asset prices to be in the future, even if they don’t intend to make a direct bet on cryptocurrencies. Even accounting for traditional firms that aren’t looking to invest in tokens, we’re still able to understand their logic behind what Bitcoin and Ethereum prices will likely look like in the near future. In today’s world of crypto venture investing we can continue to take stock of funds raised through venture capital and continually price their forward expectations of crypto asset prices.

In the end

Looking back at our past 25 years in investing and our current state of a red-hot venture market, we’re able to extrapolate a very interesting outcome for the future of crypto. When we look at venture capital raises in the future and new fund deployments, we must instead think about the implicit bet that these private investors are making on the state of crypto asset prices and where they think the liquid market is headed. Safe to say that in the future, things look optimistic for our industry.