Now we’ve covered the basics of put options, it’s time to put some of this theory into practice with our first live put trade example. These next two live trades will largely follow the same format as the call examples in lectures 3.8 and 3.9, except this time of course we’ll be trading a put option each time.

In today’s example, we’re going to buy a put option live on Tastyworks. We will then look at what our potential profit will be at expiration, taking into account the premium we pay and the strike price, and we will then let the option expire. Once the option has expired we will analyse how the position performed and calculate how much profit/loss was made.

As with the call examples in section 3, we will use the SLV silver ETF for the next two examples. This is a deliberate choice to keep most parameters the same, except the fact we are using puts. This should give you a good understanding of what differences arise specifically because of the difference between puts and calls, rather than confusing the situation by also trading a different asset. In later sections though, we will of course place trades on different products as well.

First let’s take a look at the current price of SLV on a chart I’ve pulled from Trading View.

Today is Wednesday 9th December 2020, and SLV is currently trading at around $22.34. This is a one hour chart of the price of SLV, meaning each candle represents one hour.

You can see that the price gapped down at the start of today’s session. Let’s say we have a view that the price of SLV is going to continue to decrease for the rest of the week, so we want to buy a put option to take advantage of this. We’re going to buy the put option that expires on Friday (which is December 11th), with a strike price of $22. Let’s head over to the Tastyworks software to check out the prices and place the trade.

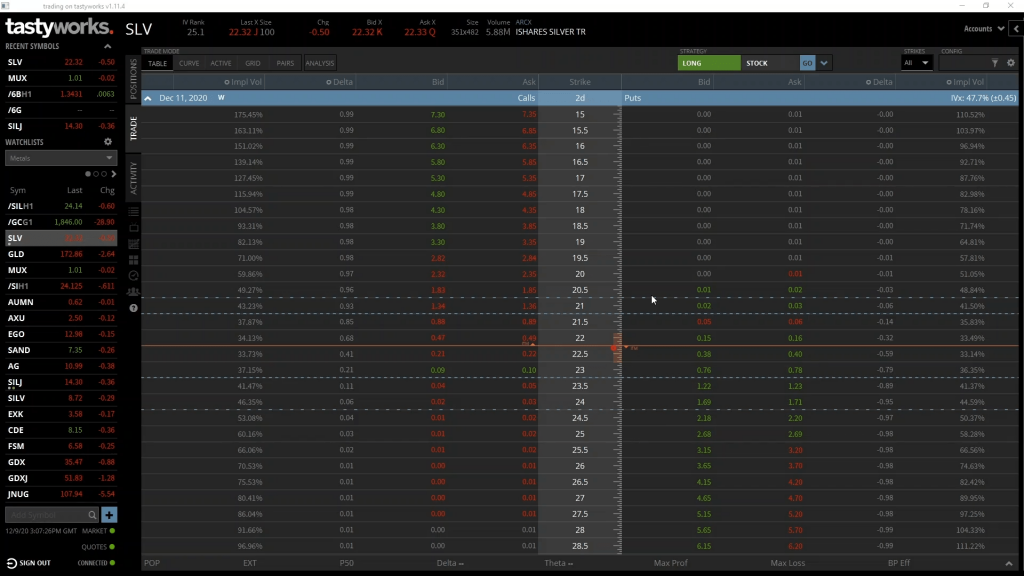

Here we have the option chain for SLV. As you can see in the top left, I’ve expanded the December 11th expiry date, so every option on the screen expires on Friday.

We’re interested in the $22 strike price, which we can find in the middle column. And we want the put, so we head right from here.

The bid is what we could currently sell this option for immediately, which is 15 cents in this case. The ask is what we could currently buy this option for immediately, which is 16 cents in this case. As we are buying this put today, it’s the ask price that we are interested in.

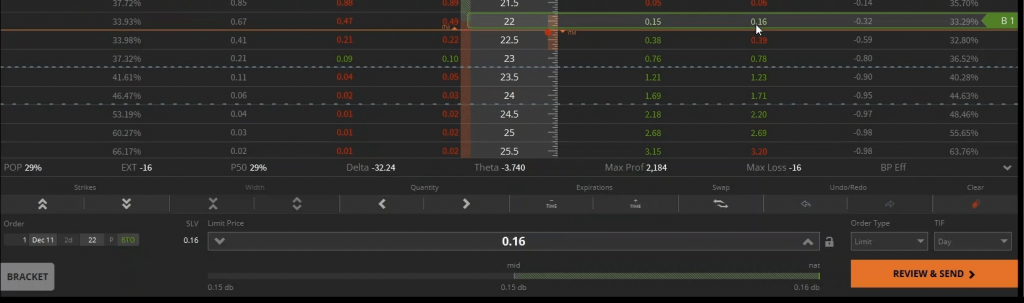

To populate the order form with an order to buy the put, we can click on the ask price of 16 cents. For this example, instead of just buying straight into the ask price of 16 cents, we’re going to set a limit price at 15 cents. This will mean we aren’t guaranteed to get filled, but if we do get filled, we will have purchased the option for a slightly cheaper price.

So here I’ve lowered the limit price of the order to 15 cents, and will send this into the market to wait for a fill. Once SEND ORDER is clicked, the pop up tells us the order has been sent correctly and is working in the market. Now we just wait and hope someone decides to sell into our buy order. Don’t worry I’ll cut out the waiting part if it takes very long.

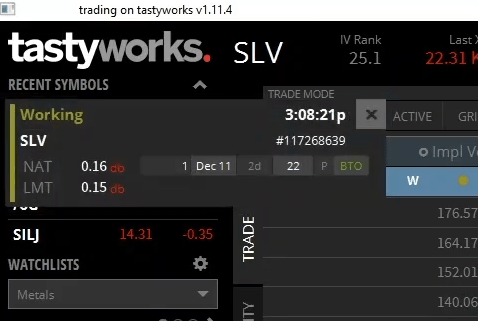

There is a pop up notification letting us know that the order has been filled. That only took a few seconds thankfully. It can take much longer, or even not be filled at all, but it’s worth knowing that you don’t have to take the ask price when buying, or the bid price when selling. You can set a limit order at whatever price you like. These SLV options we’re looking at have very tight spreads anyway, but this knowledge can be particularly useful if you’re trading an instrument with wider spreads. We’ll touch on this in other lectures as well.

We’ve now purchased the $22 put option that expires in 2 days. Before skipping ahead to see what happened, let’s look at what could happen with this position depending on what happens to the price of SLV in the next two days. We can use the knowledge gained in the other section 5 lectures to calculate our potential profit, potential loss, and where the breakeven point on this trade is.

What could happen

Let’s remind ourselves of the option parameters we have for this position.

-The underlying asset is shares of SLV

-The option type is put

-The expiry date is 11th December 2020

-The strike price is $22

-The option price (or premium) is $0.15 per share

As this is a real world example we will also include the fees in our calculations.

The total fees and commission for our order were $1.14. As the contract multiplier for SLV is 100, each option contract represents 100 shares of SLV. We bought 1 contract, representing 100 shares, so this total fee of $1.14 equates to a fee per share of $0.0114, or a little over 1 cent. This per share amount will help us in some of our calculations.

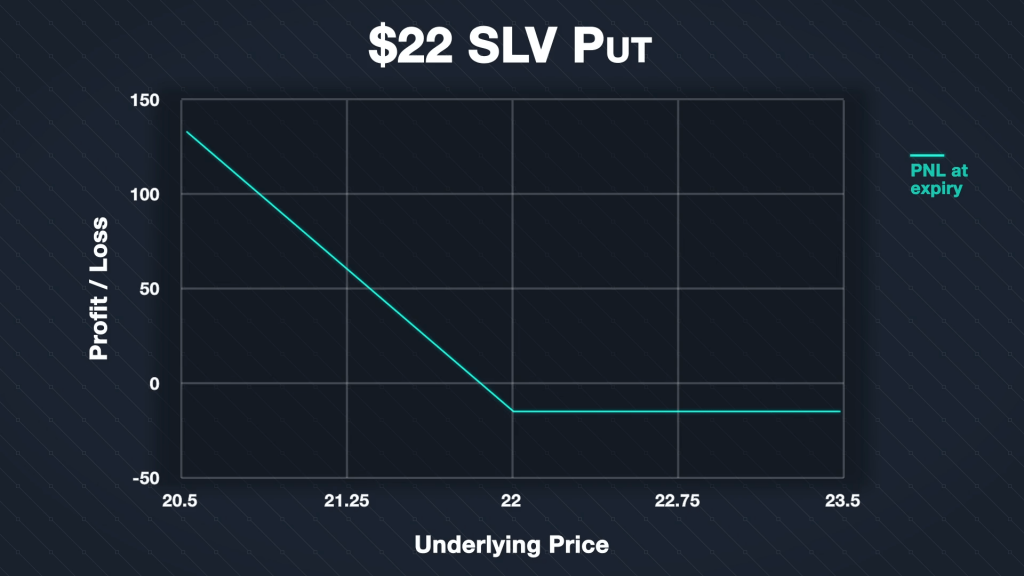

PNL chart

Given all the parameters we just covered, this is the PNL chart at expiry for this option position.

For any price of SLV above the strike price of $22, we will make the maximum possible loss. This maximum loss is limited to the premium we paid, plus the fees. We paid a premium of $0.15 per share, and the fees were $0.0114 per share. This gives us a total cost per share of $0.1614. As the contract multiplier is 100 and we purchased 1 contract, this equates to a total maximum loss of $16.14. And indeed this amount is what was shown as the total cost when we placed the order on tastyworks.

If SLV is any price below our strike price of $22 at expiry, we can calculate our profit or loss using the formula from lecture 5.3:

(Strike Price – Price At Expiration – Premium Paid) * Contract Multiplier * Number Of Contracts

Except instead of just using the premium paid per share, we can use the total cost per share, which includes the fees. So $0.1614 per share.

The profit/loss line increasing to the left of our strike price is this same formula plotted for each underlying price of SLV at expiry.

As an example, if the price of SLV at expiration is $20.50, we can calculate our profit as:

(22 – 20.5 – 0.1614) * 100 * 1 = $133.86

If the price of SLV at expiration has decreased to $20.50, our option to sell SLV at $22 is clearly worth $1.50 per share, for a total of $150. As this option cost us $16.14 in total, this gives us our profit of $133.86.

Breakeven

In lecture 5.4, we gave the formula for the breakeven point of a put option as:

Breakeven Point = Strike Price – Premium Paid

As with the profit calculations, instead of using just the premium paid, we will use the total cost including fees, which is $0.1614 per share. The breakeven point is then calculated as:

$22 – $0.1614 = $21.8386

This is the point at which the profit/loss line crosses the x axis.

What actually happened

Now we’ve studied what could happen, let’s jump forward and find out what actually did happen. Here we have the same 1 hour price chart of SLV we looked at just before placing the trade. Except now of course, it’s the end of Friday 11th December, so the option has expired.

We can see the point in time we bought the put option 2 days ago on the 9th. Later on the 9th, the price did continue to decrease, even past our strike price of $22. However, by today’s session the price had bounced back above $22, finishing the day at a price of $22.26. This is above the strike price of $22, so the put option has expired worthless, resulting in the maximum possible loss for this trade of $16.14.

The price of SLV did decrease over the life of the trade, but only by 8 cents in the end. As this was still above the strike price of the put option, this resulted in us making the maximum loss of the premium we paid plus fees.

Underlying position comparison

We began with a bearish bias, and bought the put option. This resulted in a loss, but how does this loss compare to a position in the underlying? In other words, what if we had just shorted 100 shares of SLV instead?

The price of SLV was $22.34 when we purchased the put, so we could have sold 100 shares for $2,234 instead. At the end of Friday the price had decreased slightly to $22.26, meaning we could buy back the 100 shares for $2,226. This means selling the shares instead would have resulted in a small gain of $8 (minus a little for fees).

Selling the shares would have required a lot more capital than purchasing the put option, but in this instance, selling the shares would have resulted in a better profit outcome.